3 Trade Adjustments You Need to Make Right Now Nate Bear, Lead Technical Tactician, Monument Traders Alliance This past week hasn't been easy for many traders, including myself. I saw traders who plowed money into semiconductors face margin calls and steep losses. Now, those same folks are doubling down on those bets, praying for a rebound, or chasing money as it rotates from one sector to the next. However, there's a better way to approach this market. I introduced three specific adjustments to Profit Surge Traders over the past month, designed to keep money in my pocket while riding the rebounds. Here's how they work. 1. Reduce Position Size Volatility and position size have an inverse relationship. When volatility goes up, my position size decreases. This level sets all my setups so the losses and potential profits are roughly the same. Think about it this way. I have the same setup on two stocks, A & B. Stock A will go up or down by 50%. Stock B will go up or down by 25%. If I want to keep my losses and profits the same for both stocks, I need to use half the shares to trade Stock A as I would Stock B. When the market is extremely volatile like it is now, I may cut my position size even more. I can use the VIX as a gauge to determine my position size. Right now, the VIX is trading in the high 20s. Yesterday, it was over 60. Just a few weeks ago, it was around 13. To keep things simple, if the VIX was 13 and now it's 26, I need to reduce all my position sizes by 50%. If the VIX was 13 and now it's 39, I need to reduce my position sizes by 2/3rds. This is a simple way to think through the problem. However, let me point out something quite obvious. You need a position size small enough for the setup to work. Otherwise, you'll stop out early because you're afraid of taking a massive loss. Let's stick with the idea of the VIX for a moment as we talk about the next adjustment. 2. Pick Shorter Duration Options The VIX is a measure of demand for options on the S&P 500 index, also known as implied volatility or IV. Option prices are comprised of four components: - Distance between the strike price and the stock's current price

- The intrinsic value of the option (how far it is in-the-money)

- The time until expiration

- Implied volatility

For the moment, we're going to ignore the first two and focus instead on time and IV. Here's the basics: - More Time = Higher Option Prices

- Higher IV = Higher Option Prices

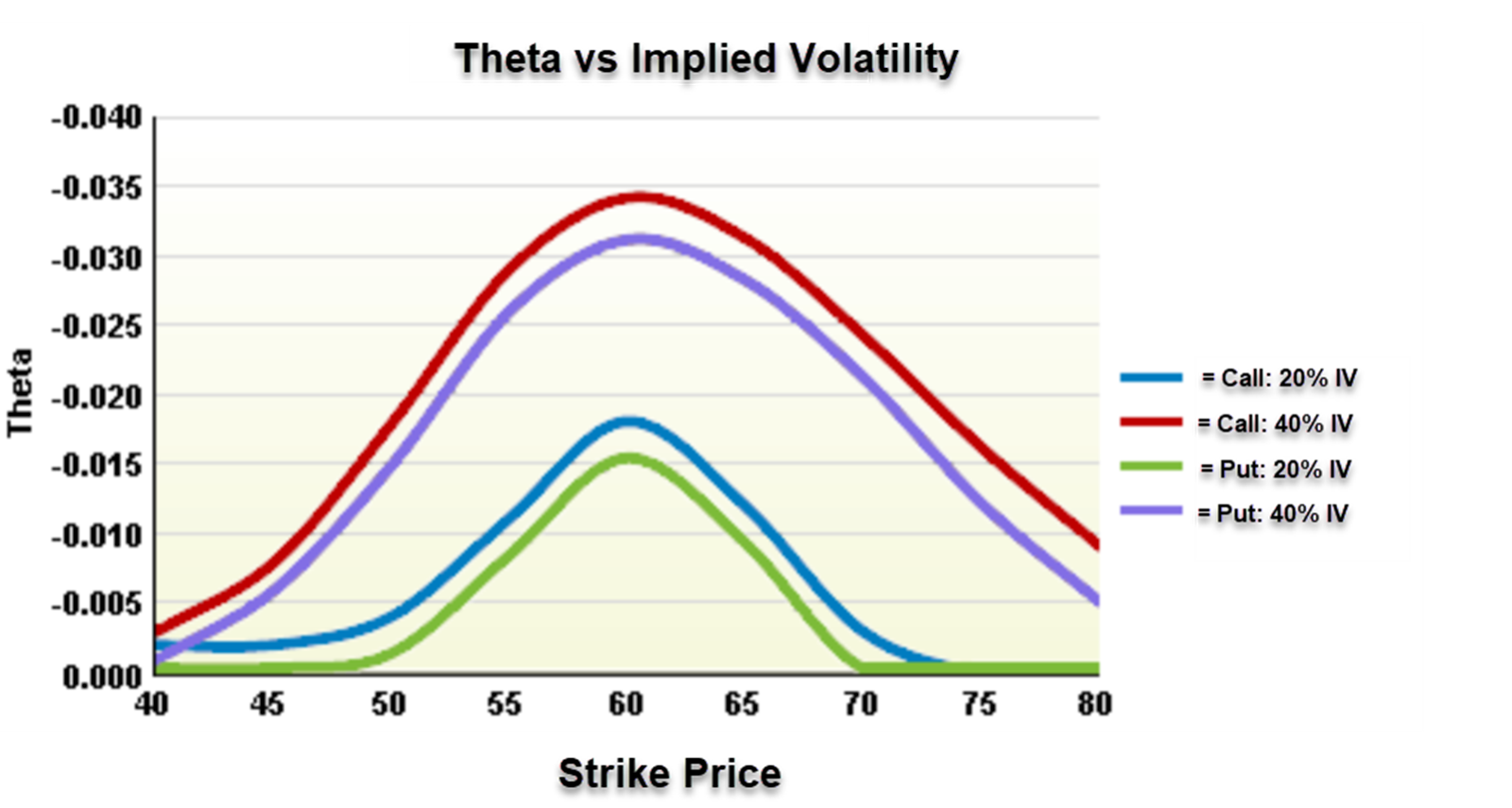

Every day that goes by bleeds off more of the option's premium at an exponential rate. However, that rate of decay is directly impacted by IV. So, if IV is higher, the amount that decays each day is higher. When you graph it, It looks something like this: The blue and green curves show lower rates of time decay because IV is lower, while the red and purple curves show higher rates of time decay because of higher IV. By selecting options with shorter durations, we limit the impact of time decay and implied volatility. At the moment, that's a good thing because IV is higher on most stocks than it has been in years. Naturally, that means I need my setups to match. So, instead of looking for potential trades on the 195-minute or daily chart, I'm going to focus on the 60, 30, 15, or even 5-minute chart setups. With the moves happening so sharp and fast, I don't need many wins because the ones I hit will deliver bigger payoffs. |

No comments:

Post a Comment