| | | | | | | Presented By Crexi | | | | Axios Markets | | By Matt Phillips and Emily Peck · May 10, 2022 | | 😐 Folks. It's brutal out there. We've opted to use zero exclamation points this morning to convey the solemnity of the situation. 🗓 Join Axios' Russell Contreras and Erica Pandey today at 12:30pm ET for a virtual event exploring initiatives to resolve financial barriers in higher education. Register. Today's newsletter, edited by Kate Marino, is 1,180 words, 4.5 minutes. | | | | | | 1 big thing: Farewell to the "Fed put" |  | | | Photo illustration: Sarah Grillo/Axios. Photo: Win McNamee/Getty Images | | | | The Federal Reserve held its last policy meeting six days ago. But it feels like it's been 60 days, given the unnerving shift in markets in the three trading sessions since then — a 7.2% drop in the S&P 500 that left the index 17% below its early January high, Axios' Neil Irwin writes. - It's the kind of moment when you might expect heightened chatter about the Fed relenting on its interest rate hike plans. But right now, all signs point to the Fed being less reactive to markets than it was in the not-too-distant past.

Why it matters: Investors can't count on the "Fed put" in the potential bear market of 2022. - The Fed put is a term used to describe the central bank's recent tendency to pivot toward looser money whenever markets drop, acting like an options contract that protects against losses.

Flashback: In late 2015 and again in late 2018, the Fed sent signals that sustained monetary tightening was on the way, then backed off in the ensuing weeks when financial markets started to go haywire, contributing to the idea that the central bank stood ready to bail out investors. Yes, but: Things look awfully different in 2022. The biggest difference is that those previous tightening actions were pre-emptive — aimed at preventing inflation from taking off. This time, inflation is a major problem in the here-and-now, not a distant potential threat. - And for all the discussion of recession risk, Fed officials emphasize signs of economic robustness, like a very strong labor market and strong household and corporate balance sheets, that may cushion the blow of higher rates.

What they're saying: "The stock market is volatile," Raphael Bostic, president of the Atlanta Fed, tells Axios. "It goes up and it goes down. I think part of what we've seen there is a byproduct of a wide range of narratives about the prospects for the economy." - "When you have a wide range of views, you're going to get more volatility in those markets. That's what we have. To be frank, I don't think that's super surprising. There's a ton of uncertainty in the world today."

What might change things and cause Bostic to reevaluate his support for rate hikes in the near term? "It would have to be some significant negative shock that would have to occur," he says. The bottom line: Never say never. But the conditions that made the Fed quick to reverse course in previous episodes of market volatility don't really apply now, which means relief from volatile markets may be hard to come by. Go deeper. |     | | | | | | 2. Catch up quick | | 🛑 Goldman Sachs plans to stop working with most SPACs it took public. (Bloomberg) 🇺🇸 Amazon helping refugee employees obtain citizenship. (Axios) 🚦Tesla reportedly stopped production at Shanghai plant. (Reuters) | | | | | | | | 3. Warhol sale disappoints |  | | | Photo by Angela Weiss/AFP via Getty Images | | | | Andy Warhol's iconic 1965 pop art portrait of actress Marilyn Monroe — considered by some the Mona Lisa of the 20th century — sold at Christie's on Monday for $195 million, Axios' Felix Salmon writes. Why it matters: "Shot Sage Blue Marilyn" set an auction record for any modern painting. But the price was substantially less than many had anticipated. - In the context of financial markets in free-fall, the appetite for high-end art is seemingly not bottomless.

The big picture: "Shot Sage Blue Marilyn" is not the most important Warhol in existence or even the most important Marilyn. Earlier portraits of Monroe, like the "Gold Marilyn" at MoMA or the "Marilyn Diptych" at the Tate, have more art-historical importance. - The series of five, 40-inch square portraits that Warhol made of the actress in 1965, however, have long been an art-market benchmark. That's partly because they're all still in private hands and partly because of the power of the silkscreened image.

Context: The previous auction record for an American painting was held by a Jean-Michel Basquiat skull that sold for $110.5 million in 2017. The record for a modern painting was held by a Picasso that sold for $179 million in 2015. - The record for a Warhol was almost certainly the $240 million that hedge fund billionaire Ken Griffin paid for the orange version of this Marilyn portrait in 2017.

- Although that sale was private and didn't take place in an auction saleroom, Monday's result implies that the market for high-end Warhols has actually declined over the past five years.

- The overall record price paid for any painting ever remains the $450 million that a controversial Leonardo sold for in 2017.

The bottom line: Market worries can infect everything — even the desire of billionaires for trophy assets. Go deeper. | | | | | | | | A message from Crexi | | Get the CRE data you need | | |  | | | | Crexi is transforming CRE by improving access to key data for real estate professionals. Here's how: With Intelligence, property buyers and sellers can quickly access 13M+ nationwide sales comps and market data to make decisions with confidence. Learn more about Intelligence. | | | | | | 4. Crypto drag |  | | | Illustration: Allie Carl/Axios | | | | Crypto prices continue to tumble, humbling companies that made a big show of building up exposure to digital assets in recent years, Matt writes. Driving the news: In yesterday's market bloodbath — as in the broader selloff over the last few months — the losses in cryptocurrencies and the companies that own and trade them have eclipsed those of the major stock indexes. Why it matters: Whether you think crypto is a potential life-altering technology or an elaborate tech-centered Ponzi scheme, the recent tumble shows what a market downdraft will do to a speculative investment that produces no cash flows. - Such investments — those that generate no dividends or corporate profits — tend to fare the worst when interest rates rise. And this year rates have risen at one of their fastest clips in history, as the Fed focuses on knee-capping inflation.

- Similarly, shares of tech firms that have shown little sign of being able to produce steady profits any time soon — like Peloton and cloud technology provider Fastly — have gotten shellacked.

By the numbers: Bitcoin shed 8% yesterday, and is worth less than half of its market value from six months ago. - A Goldman Sachs basket of 11 stocks that are especially sensitive to crypto pricing was clobbered by more than 14% yesterday alone. The basket's down about 68% over the last six months, compared to the S&P 500's 15% decline and the Nasdaq's 27% fall over the same period.

- Coinbase, the largest U.S. crypto exchange, dropped 19.5% yesterday. And MicroStrategy, a software company that issued half a billion dollars of junk bonds to buy bitcoin when it was near its peak in price, shed an eye-popping 25.6% yesterday.

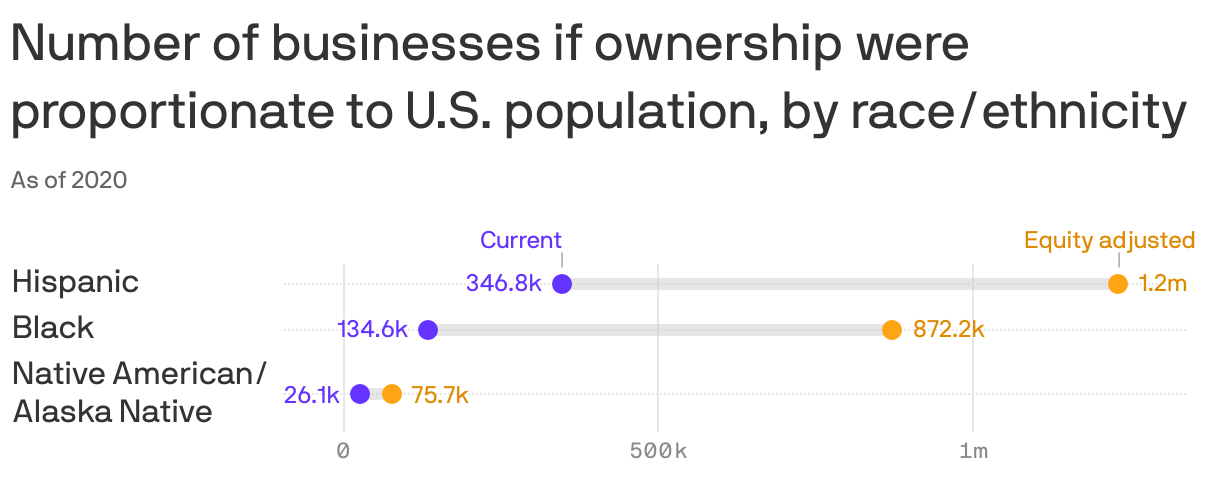

What they're saying: "My instinct is there's some more damage to be done," Michael Novogratz, a former Wall Street trader who founded crypto asset management and trading firm Galaxy Digital, said on a conference call with analysts. The bottom line: Assume the crash position. Go deeper. | | | | |  | | | | If you like this newsletter, your friends may, too! Refer your friends and get free Axios swag when they sign up. | | | | | | | | 5. An overlooked driver of the racial wealth gap |  Data: The Alliance for Entrepreneurial Equity; Chart: Erin Davis/Axios Visuals Only 2% of businesses in the U.S., or 134,600, are Black-owned, even though 13% of the country's population is Black. If business ownership was proportionate to population, there would be 872,200 Black-owned businesses, according to a new report released today, Emily writes. Why it matters: This entrepreneurial inequality is an under-appreciated driver of the racial wealth gap. - Only 6% of businesses are Hispanic-owned, or 346,800, the report notes. But if the numbers were proportionate, the number would climb to 1.2 million. (Read more on the barriers these businesses face.)

Go deeper. | | | | | | | | A message from Crexi | | This data hub helps you make better CRE decisions | | |  | | | | Intelligence, a robust data hub developed by CRE leader Crexi, is a comprehensive database subscription with unlimited access to over 13 million nationwide sales comps, map overlays and a data center. Learn more. | | |  | It's called Smart Brevity®. Over 200 orgs use it — in a tool called Axios HQ — to drive productivity with clearer workplace communications. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Suite 1300, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment