| | | | | | | Presented By ProEdge, a PwC Product | | | | Axios Markets | | By Aja Whitaker-Moore ·May 14, 2021 | | Good morning and happy Friday! Sending you warm and sunny weekend vibes. Situational awareness: April retail sales data will be released at 8:30am ET. Analysts expect strong growth after sales grew 10% in March, the biggest uptick in 10 months. (Today's TGIF Smart Brevity count: 1,287 words, 4.8 minutes.) | | | | | | 1 big thing: The distress cycle that wasn't |  Reproduced from Preqin Pro; Chart: Axios Visuals Distressed hedge funds that raised record amounts of cash last year to invest in COVID-hit businesses are sitting on a mountain of cash and competing for crumbs to invest it in, writes Axios business editor Kate Marino. Why it matters: Pandemic-era government stimulus programs, and the Federal Reserve's intervention in markets, caught many on Wall Street by surprise last year with their magnitude. - They effectively cut short the wave of distress that these hedge funds have been waiting on for over a decade — leaving many scrambling for what to do next.

How it works: Distressed funds, which mostly buy loans and bonds backing struggling companies at pennies on the dollar, hope to profit when the issuers default and can't pay their debt bills. Outside of industry-specific pockets like oil & gas or retail, this hasn't happened en mass since the financial crisis. What they're saying: "In the short term, I worry about not having great things to buy," Oaktree Capital Management's Howard Marks said at an event this week, Bloomberg reports. By the numbers: Distressed funds prepped for a pandemic doomsday scenario by raising $46 billion in 2020, almost double the annual average of $24 billion over the prior nine years, according to Preqin. - The typical places to put all that cash did not offer the opportunity investors thought they would, leaving funds sitting on $81 billion in dry powder as of September 2020

- With nowhere to go, distressed funds returned negative 8% on average during 2020 through September, compared with an average annual return of 12% from 2001-2019, Preqin says.

There are few signs of this dynamic changing. The portion of high yield bonds and loans that trade at distressed levels has fallen dramatically. And default rates tell a similar story. What's next? A hunt for new opportunity. Some have turned to more esoteric assets like vendor claims or insurance claims, or even returned cash to investors, Bloomberg reports. - Many have stretched to non-distressed high yield bonds — where strong demand has pushed up prices, says Gershon Distenfeld, co-head of fixed income at AllianceBernstein.

What to watch: The Fed and a rate hike. - "The Fed is a cycle killer," says William Housey, senior fixed income portfolio manager at First Trust Advisors.

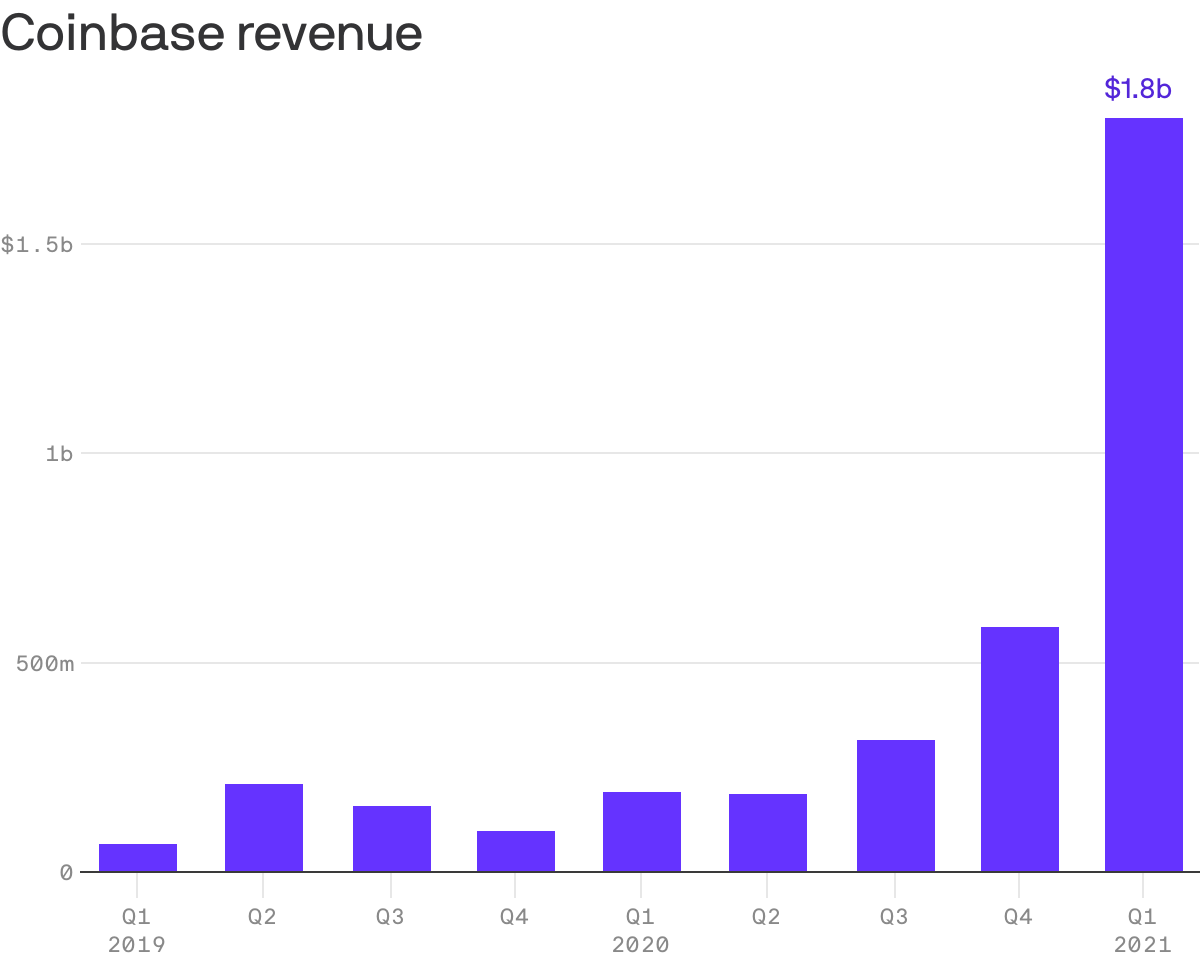

The bottom line: What is generally a good sign for the economy, is a distressed investor's worst nightmare. Go deeper. |     | | | | | | 2. Catch up quick | | Binance, the world's largest cryptocurrency exchange, is under investigation by the Justice Department and the Internal Revenue Service. The probe is part of a government effort to track illicit activity that's supported by the cryptocurrency market. (Bloomberg) A group of large U.S. banks plans to begin extending credit to people who previously lacked the ability to borrow money. The banks will share data on customer deposit accounts, as part of a government-backed initiative to open up credit to people who lack credit scores but are financially responsible. (WSJ) Institutional investors, starved for returns, are buying up single-family homes to rent out or flip, driving up prices for individuals. (WSJ) | | | | | | | | 3. The rehabilitation of Wells Fargo |  Data: Harris Poll; Chart: Danielle Alberti/Axios Wells Fargo is no longer viewed as the least ethical big company in America. That's the big lesson from the most recent Axios Harris reputation poll, writes Axios Capital author Felix Salmon. Why it matters: After hitting extreme Axios Harris lows in 2017, Wells Fargo embarked upon a massive public rehabilitation campaign in 2018. It seems to have worked. Flashback: The bad news started with the revelation in 2016 that the bank had created millions of fake accounts and opened them without the account holders' permission or even knowledge. It didn't end there — a series of scandals followed, tarnishing Wells Fargo's reputation — and that of its former CEO. By the numbers: Wells Fargo's "ethics" score of 38.9 in 2017 was by far the lowest in the history of the poll. (Wells Fargo and the Trump Organization are the only companies to ever score under 50.) This year, it has recovered to 62 — a big jump, even if it's still in the bottom five. - Overall, Wells Fargo's reputation score of 63 in 2021 puts it well ahead of Facebook, tied with TikTok, and slightly behind Comcast.

- Other banks have also been improving. The reputation score for Bank of America, for instance, increased from 59.7 to 70.5 between 2017 and 2021.

The bottom line: Banks are generally unloved, with the notable exception of USAA, which has outperformed in every year of the survey. And Wells Fargo remains at the bottom of the banking pack. That said, the sector as a whole is improving. | | | | | | | | A message from ProEdge, a PwC Product | | Align skills and culture with the changing nature of work | | |  | | | | Readying the enterprise for the future typically includes investment in new technologies. But it also requires ensuring your organization has the right skills to make the most of these technologies. Read the guide from ProEdge, a PwC Product. | | | | | | Bonus chart: Coinbase revenue surges |  Data: FactSet; Chart: Will Chase/Axios Coinbase reported record revenue on Thursday. But its biggest news was the announcement that it plans to list Dogecoin on its exchange in the next six to eight weeks. Go deeper. | | | | | | | | 4. Bulls keep shrugging off bad news |  Data: Boston Consulting Group; Chart: Sara Wise/Axios Just over half of investors (53%) are bullish on the S&P 500 over the next three years — even as the index sits at or near record levels, according to a bi-weekly sentiment survey released Thursday by Boston Consulting Group, Kate writes. Why it matters: Strength in long-term market views was on full display over the past week, as stocks largely shrugged off seemingly negative data. - Major indexes had muted reactions to last Friday's disappointing jobs numbers, the Colonial Pipeline cyberattack and higher-than-expected inflation data.

Yes, but: In the shorter term, many say they're slightly less optimistic than they had been. About 47% have a bullish view of the S&P 500 in 2022, down from 57% who held that view in July of last year. - The shrinking bullish contingent reflects the fact that valuations have expanded rapidly and the economic rebound is more priced in, Hady Farag, BCG partner and associate director, tells Axios.

Meanwhile, the economic recovery has shifted expectations for corporate behavior. - Just 54% think it's important for healthy companies to focus on preserving liquidity, the lowest reading in the survey's history. The high was 79% in April 2020.

- And 56% believe companies should quickly access all available sources of debt financing, also a record low. It was at 73% last April.

On the flip side: More investors are now comfortable with companies maintaining dividends and doing share repurchases. - They also have lower tolerance for companies not meeting (or even providing) earnings guidance.

| | | | | | | | 5. A replacement rate rollercoaster |  | | | Illustration: Eniola Odetunde/Axios | | | | The Libor benchmark interest rate is going away soon and the transition to a replacement has been a bit bumpy, Kate writes. The intrigue: Why anyone cares about this particular saga is related to the fact that trillions of dollars in corporate and consumer debt are pegged to it. - Libor fell out of favor after regulators in 2008 revealed widespread manipulation of the rate by traders at numerous banks.

Why it matters: So far investors largely aren't raising alarm bells over the uncertainty. But the process of moving to a new benchmark, called SOFR, has dragged on — and talk of using different alternative rates is increasingly cropping up. What's new: Bank of America and JPMorgan used a new Bloomberg index in a sizable trade earlier this month, the WSJ writes. That index will compete with SOFR. - The BofA/JPM transaction could signify a fork in the road of investor opinion on the matter, as more people think multiple benchmarks will replace Libor, instead of just one, WSJ says.

What's at stake: "The swath of those impacted by Libor is vast — like $220 trillion vast," Meredith Coffey, executive VP at the Loan Syndications and Trading Association, tells Axios. - "It is the benchmark rate used in setting many adjustable-rate loans worldwide — from corporate loans to mortgages to credit cards to auto loans to student loans in various countries. And it is going away."

Watch this space: Numerous alternative rates mean investors have to do more to prepare operations, technologies — and, importantly, investment strategies — for a multirate environment. The bottom line: Large investment banks and asset managers will undoubtedly find their way through the process. But regional banks and smaller funds may not have the same depth to adapt as quickly. | | | | | | | | A message from ProEdge, a PwC Product | | Align skills and culture with the changing nature of work | | | | | | | | Readying the enterprise for the future typically includes investment in new technologies. But it also requires ensuring your organization has the right skills to make the most of these technologies. Read the guide from ProEdge, a PwC Product. | | | | | | Axios thanks our partners for supporting our newsletters.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Suite 1300, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment