| | | | | | | | | | | Axios Markets | | By Felix Salmon · Oct 01, 2022 | | It's been a pretty calamitous week, especially in the U.K. and Florida, so I'm going to try some counterprogramming today and look on the bright side of the strong dollar. That said, even NASA is worried about calamity; I'll talk about that, too. - The whole thing, including an examination of financial inclusion in credit scoring, is 1,435 words, a 5.5-minute read.

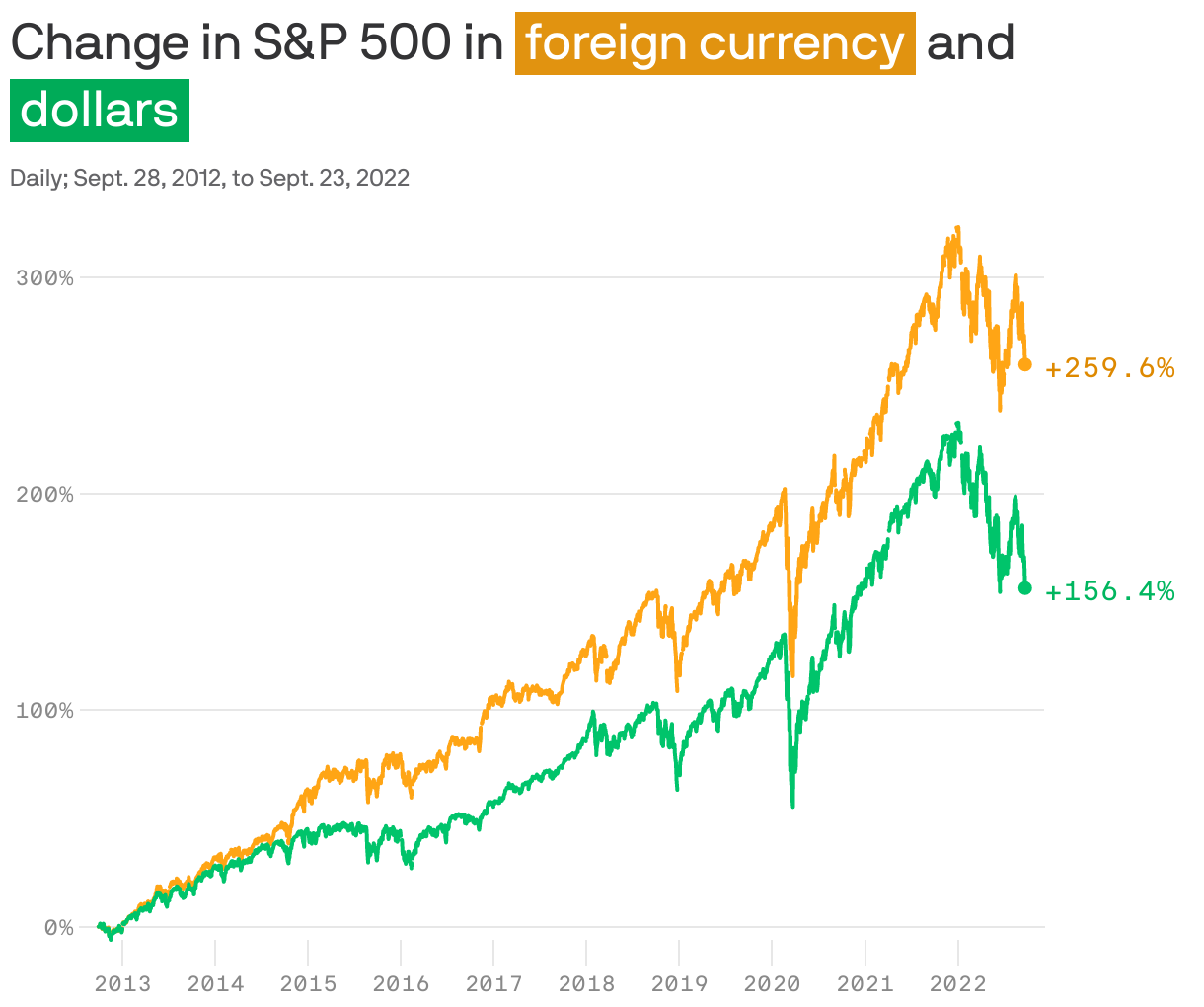

| | | | | | 1 big thing: Don't hate the strong dollar |  | | | Illustration: Natalie Peeples/Axios | | | | The strong dollar might not actually be "wreaking havoc" around the world, as some headline writers would have you believe. Why it matters: Large swings in the dollar — in either direction — tend to destabilize corporate and central bank strategies. Stability and predictability are good things. Still, the strengthening greenback is welcome news to many constituencies. Foreign investors all have substantial exposure to stocks and bonds that are denominated in dollars — and the strong dollar has helped boost their local currency returns. - Over the past 10 years, the S&P 500 is up more than 250% in foreign currency terms, if you look at how the the dollar has performed against a trade-weighted basked of currencies. By comparison, it's up only about 150% in dollar terms.

Foreign governments, frustrated by sluggish domestic economies, like the idea that their exporters will see higher revenues when their currencies weaken, thereby boosting growth. - China, for instance, has pushed its currency down to a low of 7.2 yuan to the dollar, in an attempt to turbocharge exports.

- Europe has seen its currency weaken by roughly the same amount, much to the delight of its exporters. One euro is worth about 22% less than it was at the beginning of 2021; one yuan is worth about 13% less than it was as recently as March 2022.

- "The weakening of the euro, yen, pound, or renminbi improves the competitiveness of other major economies, offering support for their economic activity," writes Stephen Dover of the Franklin Templeton Institute.

The Federal Reserve, tasked with lowering inflation, is happy to let the strong dollar do some of the heavy lifting. - Imported goods cost less in dollar terms, causing disinflation.

- The profits of multinational corporations also decline in dollar terms, both because foreign revenues are worth less and because U.S. companies find it harder to compete with companies whose prices are denominated in euros or yuan. That might not be great news for the companies in question, but it does help the Fed slow demand in the economy.

What they're saying: "At this juncture, where inflation seems much too high and much more out of whack relative to target, U.S. policymakers are probably looking at the stronger dollar and are quite pleased with the help they are getting on the inflation front," writes Kamakshya Trivedi of Goldman Sachs. The bottom line: The last time the dollar was this strong, in 1985, the world's governments made a concerted effort to weaken it. This time around, that's highly unlikely to happen. |     | | | | | | Bonus: The stock-market boost |  Data: FRED; Chart: Simran Parwani/Axios Visuals. Note: Foreign-currency returns calculated using the Federal Reserve's Broad Dollar Index. | | | | | | | | 2. The race to hand out credit scores |  | | | Illustration: Victoria Ellis/Axios | | | | Credit bureaus want to score more Americans, by incorporating non-credit sources — timely rent payments, for instance — into their calculations. Why it matters: A lot of for-profit companies have joined the bureaus in this space, invariably proclaiming high-minded ideals of financial inclusion. But as Stanford sociologist Barbara Kiviat tells Axios, "access to credit is the same thing as enabling people to become indebted." How it works: Lenders like to lend to people they can trust to repay them in full and on time. One way of predicting such behavior is to look at how assiduously previous loans have been repaid. Another way is to look at a history of on-time payments for anything from rent to utilities to Netflix. - One such program, Experian Boost, has signed up 8.6 million Americans. In the same vein, Esusu, which works with landlords, claims a 100% success rate in getting a credit score for people who previously didn't have one.

- Other credit-building companies, like TomoCredit and X1, make short-term loans underwritten against wealth or income rather than repayment history. Those loans then build a credit history, which becomes a credit score.

By the numbers: Compared to someone with "very good" credit of between 740 and 799, someone with "fair" credit — between 630 and 689 — has to pay substantially more interest on their loans. The credit risk means higher rates of about half a point on mortgages, three points on auto loans, and seven points on credit cards. The catch: If a "credit invisible" person then ends up with a credit score that's very low, that can be worse than having no credit score at all, says Chi Chi Wu of the National Consumer Law Center. - Having bad credit can double your car insurance rate — but in most states that allow insurers to use credit scores, the law specifically says that people without a credit score can't be penalized.

- Similarly, having bad credit is worse than having no credit when you're applying for a job.

- Having a subprime credit score also exposes people to some of the most predatory lenders in the industry.

The other side: "I have yet to see anyone go from credit invisible to a bad score," says Maitri Johnson, who oversees programs at TransUnion that incorporate rent payments into credit scores. The big picture: All of these programs, so far, are opt-in. People who pay their rent on time are the people who try to improve their credit scores, or get a brand-new score that's reasonably healthy. People who don't, generally don't. - The risk is that as these programs become embedded into credit bureaus' methodology, data on things like rent and utility payments will be automatically reported, much like data on loan repayments are today.

- At that point, the programs "may replicate and entrench the social and economic disadvantages that lead some people to have fair and poor credit scores," write law professors Pamela Foohey and Sara Sternberg Greene in a recent article.

| | | | | | | | A message from Axios | | Join the Axios Pro: Policy waitlist | | |  | | | | Axios Pro: Policy is your behind-the-scenes look into the halls of congress. How it works: Sign up to be the first to know when Axios Pro: Policy launches, and receive special pricing. Join the waitlist | | | | | | 3. Who's really spending longtermist billions |  | | | Illustration: Sarah Grillo/Axios | | | | A 1,260-pound spacecraft, traveling at 13,680 miles per hour, obliterated itself on Monday by smashing — deliberately — into an asteroid moonlet called Dimorphos. Why it matters: The $324.5 million program, known as DART, is just part of the broader NASA project known as "planetary defense" — which, even now that DART is largely over, will continue to be funded to the tune of $142.7 million per year. - In fact, the $142.7 million is $55 million more than NASA asked for; Congress is telling NASA to hurry up and spend more money, more quickly, to reach its mandate of identifying 90% of near-Earth objects greater than 140 meters in diameter.

The big picture: This is the sort of spending that governments are supposed to be bad at. - A 2010 report by the National Research Council (NRC), with the wonderful title "Defending Planet Earth," admits that the roughly 100 lives per year lost on average to asteroid impacts is probably "trivial in the general scheme of things."

- The catch, of course, is that the average conceals massive variation — and that a large impact could pose existential risk. (Just ask the dinosaurs.)

The problem of asteroid impacts, concludes the NRC, is simultaneously "extremely important" and "extremely rare." - Asteroid 2005 ED224, for instance, is only 50 meters in diameter — about the same size as the Tunguska event of 1908, and much smaller than anything NASA is looking for. It's the closest thing to a present risk that Earth faces, but when it passes our planet on March 11, there's only going to be a 0.0002% chance of collision.

What they're saying: Charitable foundations are necessary, wrote Stanford professor Rob Reich in a highly influential 2013 essay, insofar as they "take on the long-run, high-risk policy experiments that no one else will." - "Public officials in a democracy do not have an incentive structure that rewards high-risk, long time horizon experimentation; they need to show results quickly from the expenditure of public dollars in order to get re-elected."

Between the lines: The best-case outcome of the planetary defense budget — essentially a billion-dollar insurance policy of unknowable utility — is that it's wasted and never needs to be put to the test. - If it does get put to use, the politicians who funded it will almost certainly all be long dead. And yet, those same politicians, over the past decade, have joined forces across the aisle to provide the planetary defense project with a nine-figure annual budget.

The bottom line: The longtermist project in philanthropy is dedicated to the proposition that wealthy individuals can and must step in to protect the planet from risks that governments are too myopic to address. - The DART program stands as an implicit rebuke to that thesis — especially since there is no chance that it would have ever been funded via private philanthropy.

| | | | |  | | | | If you like this newsletter, your friends may, too! Refer your friends and get free Axios swag when they sign up. | | | | | | | | Building of the week: The Gasworks, Dublin |  | | | Photo: David Dear/Construction Photography/Avalon/Getty Images | | | | The Gasworks, in Dublin, designed in 2006 by O'Mahoney Pike architects, is one of the most striking examples of the kind of residential adaptive reuse that Kate wrote about this week. - An old gas holder now houses 240 apartments on nine levels.

| | | | | | | | A message from Axios | | Join the Axios Pro: Policy waitlist | | | | | | | | Axios Pro: Policy is your behind-the-scenes look into the halls of congress. How it works: Sign up to be the first to know when Axios Pro: Policy launches, and receive special pricing. Join the waitlist | | | | Thanks to Kate Marino for editing this week, and Elizabeth Black for copy-editing. |  | | Why stop here? Let's go Pro. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment