| | | | | | | Presented By Hands Off My Rewards | | | | Axios Markets | | By Matt Phillips and Emily Peck · Sep 30, 2022 | | Hang in there everybody, at least it's Friday. Today's newsletter is 1,036 words, 4 minutes. | | | | | | 1 big thing: Ugly, ugly, ugly |  | | | Illustration: Sarah Grillo/Axios | | | | Another bad day, in a rotten month, in a horrible year in the markets, Matt writes. Driving the news: The penultimate trading day of Q3 was another rough one, with stock and bond markets continuing to take rising interest rates on the chin. Why it matters: The performance of financial markets has a profound effect on the thinking of business executives who decide whether to borrow, invest, expand and hire — or cut staff and production and hunker down in a defensive crouch. - With markets like this, a fair amount of crouching is to be expected.

- If the hunkering hits a critical mass, a recession can result, as uncertainty becomes something of a self-fulfilling prophecy.

- The Q3 numbers on borrowing in the bond markets, initial public offerings, and mergers and acquisition activity all point tp a stark decline in risk-taking among our titans of industry. (More on that below.)

By the numbers: After the S&P 500's strong start to the summer revealed itself to be a bear market rally, the index is on pace to end the third quarter down roughly 4%. - Inflation, and the Fed's efforts to fight it with higher rates, slammed bond prices — which are on track to be down roughly 5% over the quarter, as measured by the Bloomberg U.S. Aggregate index.

State of play: Barring a miracle today, the S&P is headed for a third straight quarter of losses — the first such string since an awful stretch that ended in the first quarter of 2009 — leaving the index lower by roughly 24% this year as of Thursday. That would be the benchmark's worst performance since the full-year loss of 38.5% in 2008. - The nearly 16% year-to-date tumble in the Bloomberg bond index is the worst on record stretching back to the late 1970s.

But, but, but: Keep in mind that since the COVID crisis hit — arguably the largest shock to the world economy since World War II — the S&P 500 is actually up. - We're up about 13% since the end of 2019.

- The S&P averages a 7% increase per year, so we're basically on track for a few years of slightly subpar stock market performance.

The bottom line: It still hurts to look at that 401(k) statement, though. |     | | | | | | 2. Catch up quick | | 📉 Nike warns of inventory glut, price cuts (CNBC) 🌫 Hurricane Ian turns toward Carolinas (AP) 💶 Euro zone inflation hits 10% (AP) 🤴🏻 King Charles to be on British coins before Christmas (Fortune) | | | | | | | | 3. Charted: IPOs down |  Data: Dealogic; Chart: Axios Visuals One word: Wow. When stocks are down 24%, it may not be the best time to go public — and IPOs have all but disappeared this year, Axios' Kate Marino writes. Worth noting: Not included in the above chart are companies that went public by merging with SPACs. - Those are down a ton this year, too: Q3 deal value of $13 billion is but a fraction of the $118 billion in SPAC mergers, on average, over the first three quarters of 2021, according to Dealogic.

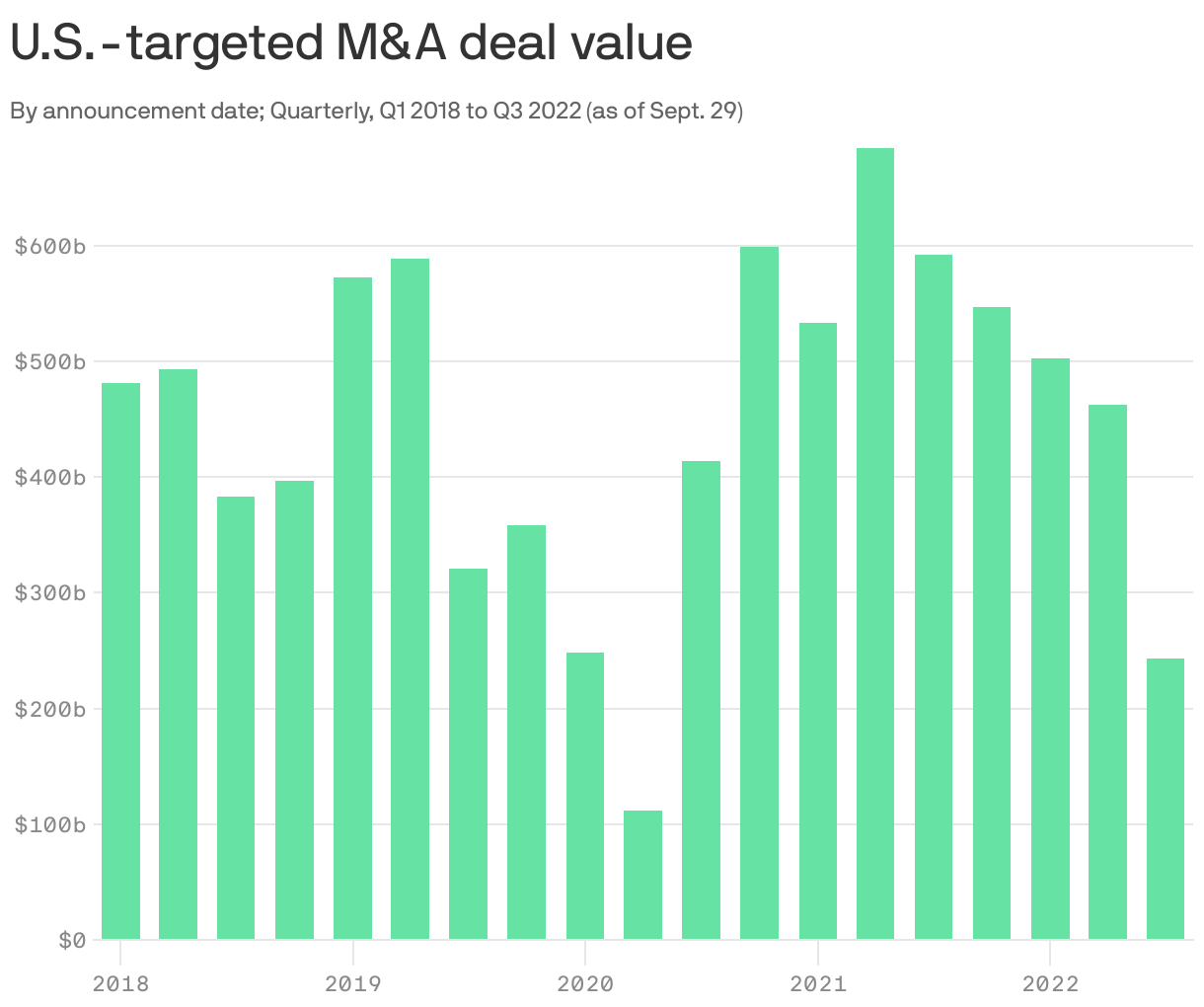

| | | | | | | | A message from Hands Off My Rewards | | Congress, take your hands off my rewards | | |  | | | | Despite record profits, mega-retailers and merchant groups are trying to trick Congress into passing harmful credit card routing mandates that will end popular rewards programs. What you need to know: Lawmakers must oppose the Credit Card Competition Act. Learn more. | | | | | | 4. Charted: M&A down |  Note: M&A data excludes SPAC mergers; Data: Dealogic; Chart: Axios Visuals As of the second quarter of this year, M&A was down but not out. That changed in Q3, Kate writes. The big picture: First-half deal volumes were lower than the record-breaking 2021 levels — but still higher than the average in the years before the pandemic. - But in the last three months, deal-making volumes were basically halved from Q2 levels, sinking below the 2018-2019 quarterly average.

State of play: The higher cost of capital, of course, is one of the big factors. Debt's been getting more expensive since the beginning of the year, chipping away at the affordability of financing a huge purchase. - Recession risk is lurking, too. "When companies are anticipating that there's a recession on the horizon, they say to themselves, perhaps it's time to pull our horns in a little bit. And I think that's what we're seeing," Ken Monaghan, co-head of high yield at Amundi U.S., tells Axios.

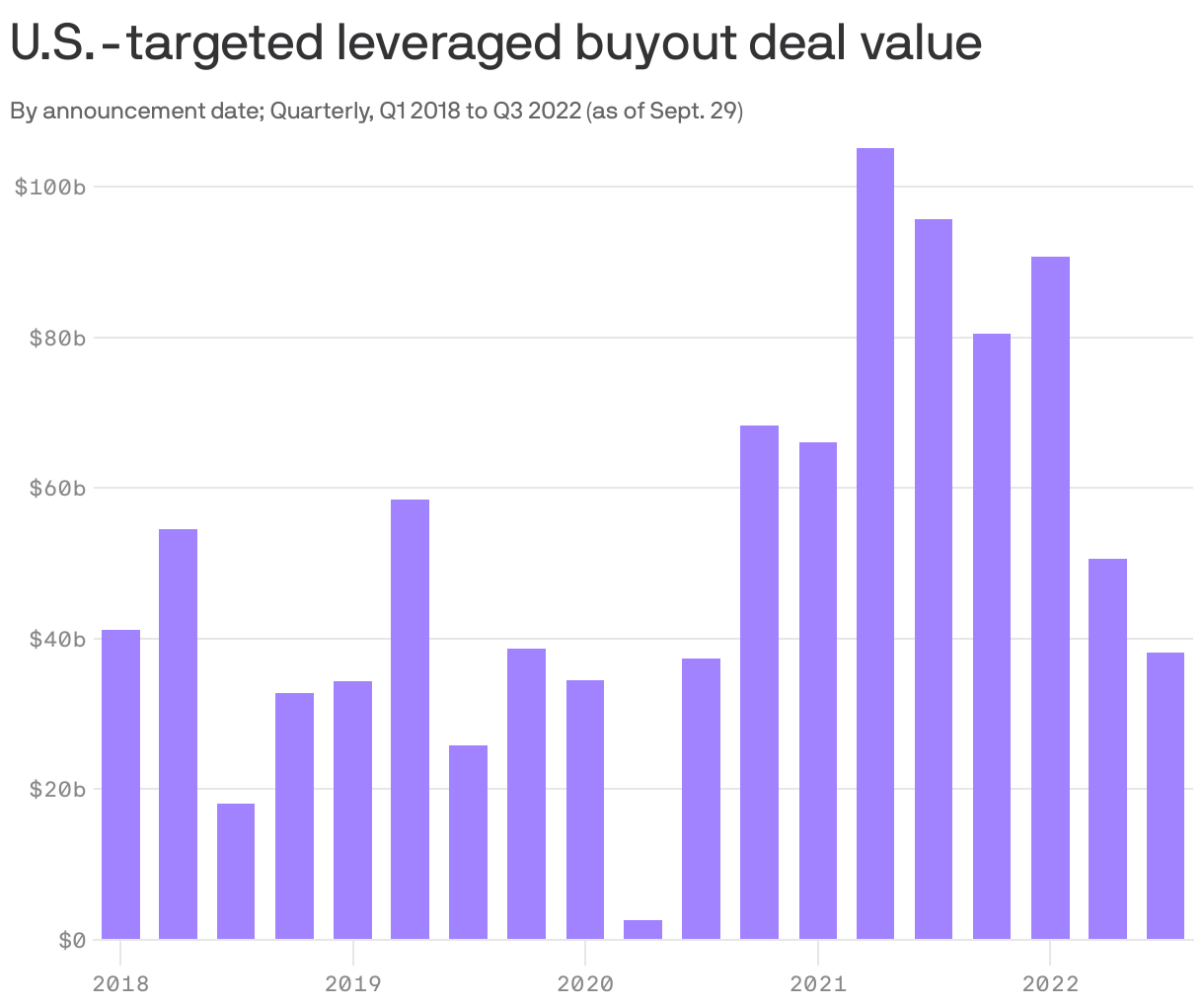

| | | | |  | | | | If you like this newsletter, your friends may, too! Refer your friends and get free Axios swag when they sign up. | | | | | | | | 5. Charted: Leveraged buyouts down |  Data: Dealogic; Chart: Axios Visuals The story with leveraged buyouts (LBOs) is a little different. Though deal volumes plummeted this quarter, historically speaking they've held up better than corporate M&A — Q3 was neck-and-neck with the pre-pandemic average, Kate writes. How it works: LBOs are the heavily debt-financed acquisitions by private equity firms. - Those firms raise money from investors, and in turn, use those funds to buy companies.

The big picture: Right now, PE firms are sitting on record amounts of "dry powder," or investor money that needs to be deployed. - That adds up to a little more pressure to do deals than what, say, a corporate CFO might face in an uncertain market.

The bottom line: Still, Q3 LBO activity is a whopping 64% lower than the peak in the second quarter of last year — a signal of the sea change in the markets that Matt described above. | | | | | | | | 6. Charted: High yield bonds down |  Data: Pitchbook LCD; Chart: Axios Visuals Corporate borrowing in the high yield bond market slowed to a trickle as money got more expensive, Kate writes. - Not surprising, right? That's basically what the Fed wanted to happen when it started raising rates.

But, but, but: The Fed's actions before this year's rate hikes are just as important a factor here. - Call it the pull-forward effect: Thanks to the ultra-low rates of 2020-2021, just about every company with debt has recently refinanced — and pushed maturities to later in the decade.

- "The need to just do the normal refinancing that companies typically do, is just not there right now," says Lindsay Rosner, principal on the multi-sector portfolio management team for PGIM Fixed Income.

Meanwhile: The investment grade (IG) bond market slowed, too, though not as much as high yield. - IG bond deals in Q3 totaled $270 billion, down from a Q1 2021 peak of $422 billion — but right on top of the 2018-2019 average of $267 billion per quarter, according to Pitchbook LCD.

What to watch: Even the higher-credit quality IG space may slow further in the months ahead. - Rosner notes that September issuance of around $80 billion was nowhere near the $125 billion-$150 billion expected in the pipeline at the beginning of the month.

- Translation: Some of the expected deals just didn't come to market.

The bottom line: "The volatility in the market and the uncertainty around economic projections is really filtering into the credit market," Rosner says. | | | | | | | | A message from Hands Off My Rewards | | Congress, take your hands off my rewards | | | | | | | | Despite record profits, mega-retailers and merchant groups are trying to trick Congress into passing harmful credit card routing mandates that will end popular rewards programs. What you need to know: Lawmakers must oppose the Credit Card Competition Act. Learn more. | | | | 🌷1 Thing Matt Loves: Hey, given the ugly developments in bonds and stocks, I've got a solid place for you to put your money that will yield an incredible return in just a few months. Flower bulbs. That's right, we're well into fall and now is the time to get crocuses, daffodils, alliums and, of course, tulips tucked into the soil — a diversified portfolio is best — setting yourself up for a burst of color next spring. Oh, but don't go crazy. There's a reason tulip bulbs were the focus of one of the first speculative manias on record. Today's newsletter was edited by Kate Marino and copy edited by Lisa Hornung. |  | | Why stop here? Let's go Pro. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment