| | | | | | | Presented By SiriusXM | | | | Axios Markets | | By Felix Salmon · Feb 04, 2023 | | I'm back from spending five days longer than expected in New Zealand, thanks to global warming. The flight delay was annoying, but the country is as spectacularly beautiful as ever. In this week's newsletter: Why I like discontinuous stock trading, why TikTok ain't what it used to be, the IRS's biased auditing algorithm, and more. All in 1,459 words, a 5.5-minute read. | | | | | | 1 big thing: The stock market is broken |  | | | Illustration: Shoshana Gordon/Axios | | | | At 9:30am on January 24, the world saw, briefly, just how fragile the stock market is. When it's left to its own devices — which is, essentially, exactly what happened — prices in more than 25o stocks oscillated wildly, causing unacceptable and chaotic trades, many of which had to be torn up after the fact. Why it matters: Stock auctions, like the ones held at 9:30am and 4:00pm every day, are a transparent and reliable form of price transparency. The continuous trading that happens between those hours, by contrast, is rife with illiquidity, flash crashes, and market manipulation. - Without an opening auction to anchor prices, the market proves utterly rudderless.

The big picture: As Walter Mattli explains in his excellent book, "Darkness by Design," the stock market has, since roughly 2005, become dominated by ruthless and highly profitable financial intermediaries — banks and high-frequency traders — who trade against large investors. How it works: During the trading day, the stock market operates on a "continuous" basis, with the time between trades measured in microseconds. In such a system, it's generally impossible to instantaneously match a natural buyer or seller with someone wanting to do the opposite trade. Instead, middlemen intermediate almost all of the trading. - The exceptions to the rule are the opening and closing auctions, when trading can be done in size, and the high-frequency traders don't have an edge.

Between the lines: There is no particularly good reason why stock markets need to trade continuously. Until March 2020, for instance, stocks listed on the Taiwan Stock Exchange traded in mini-auctions every five seconds. - When Taiwan switched to continuous trading, the move increased both trading costs and adverse selection, according to a paper studying the changeover. It was unambiguously bad for investors.

- The exchange itself, however, saw higher volume, higher fees, and higher profits — which explains why it switched.

Reality check: It's hard to see the U.S. moving to a system of "frequent batch auctions," or discontinuous trading — no matter how much better that would be for investors — because such a move would be bad, financially, for the exchanges themselves. - The events of last month, however, underscore that auctions are much more robust than continuous trading, and are much more efficient for the large investors — pension funds, insurers, and the like — who invest on behalf of everyday Americans.

The bottom line: America has too many stock exchanges — well over a dozen — and, as Mattli compellingly demonstrates, a set of toothless regulators who seem incapable of enforcing rules about what happens on them. (It's been almost a decade since the most recent SEC action against the NYSE, and that was a hand-slap.) - In an ideal world, there would be no continuous trading. A series of auctions would be much more effective at providing investors with the liquidity they need, without any bid-offer spread at all. They don't even need to happen every five seconds; a handful of auctions per day would probably suffice.

Go deeper: My review-essay of Mattli's book appeared in Foreign Affairs in 2019. |     | | | | | | 2. Locked in |  | | | Illustration: Lazaro Gamio/Axios | | | | Consumer-facing companies grow by delighting consumers and providing them with what they want. That's not how they make money, though. They make money by getting a critical mass of customers, locking them in, and then exploiting them. The delight goes away, but the profits roll in. Why it matters: This cycle — as explicated by Cory Doctorow in Wired — has been seen at every social network, including TikTok, and at a huge number of other companies, too. They start out great, grow to a point at which their sheer size alone becomes self-fulfilling, and then pivot to extracting dividends from their corporate customers. Where it stands: Doctorow makes the case that TikTok has now reached that point. The days when it was referred to as "the only good social network" are long gone — the novelty has worn thin, to be replaced by formulaic thirst traps and professional influencers. - What they're saying: "TikTok is only going to funnel free attention to the people it wants to entrap until they are entrapped," writes Doctorow.

Between the lines: The model here is Amazon, a company that used to put customers front and center but has now become, as John Herrman writes, simultaneously junkier and vastly more profitable. Driving the news: Amazon's decision last month to abolish its hugely popular Amazon Smile program is instructive. - Smile was a way that Amazon's customers could give money to charity instead of giving it to Amazon's network of affiliate marketers. If you went directly to the site rather than following a link from a site like Wirecutter, you could effectively pay some of that commission to a good cause of your choice.

- The official announcement says that "as a company, we will continue supporting a wide range of other programs." Which is to say, it's a pivot from customers directing a part of their own purchases, to Amazon directing a part of its own corporate profits.

- The message: We're stuck in Amazon's world, and Jeff Bezos is very thankful.

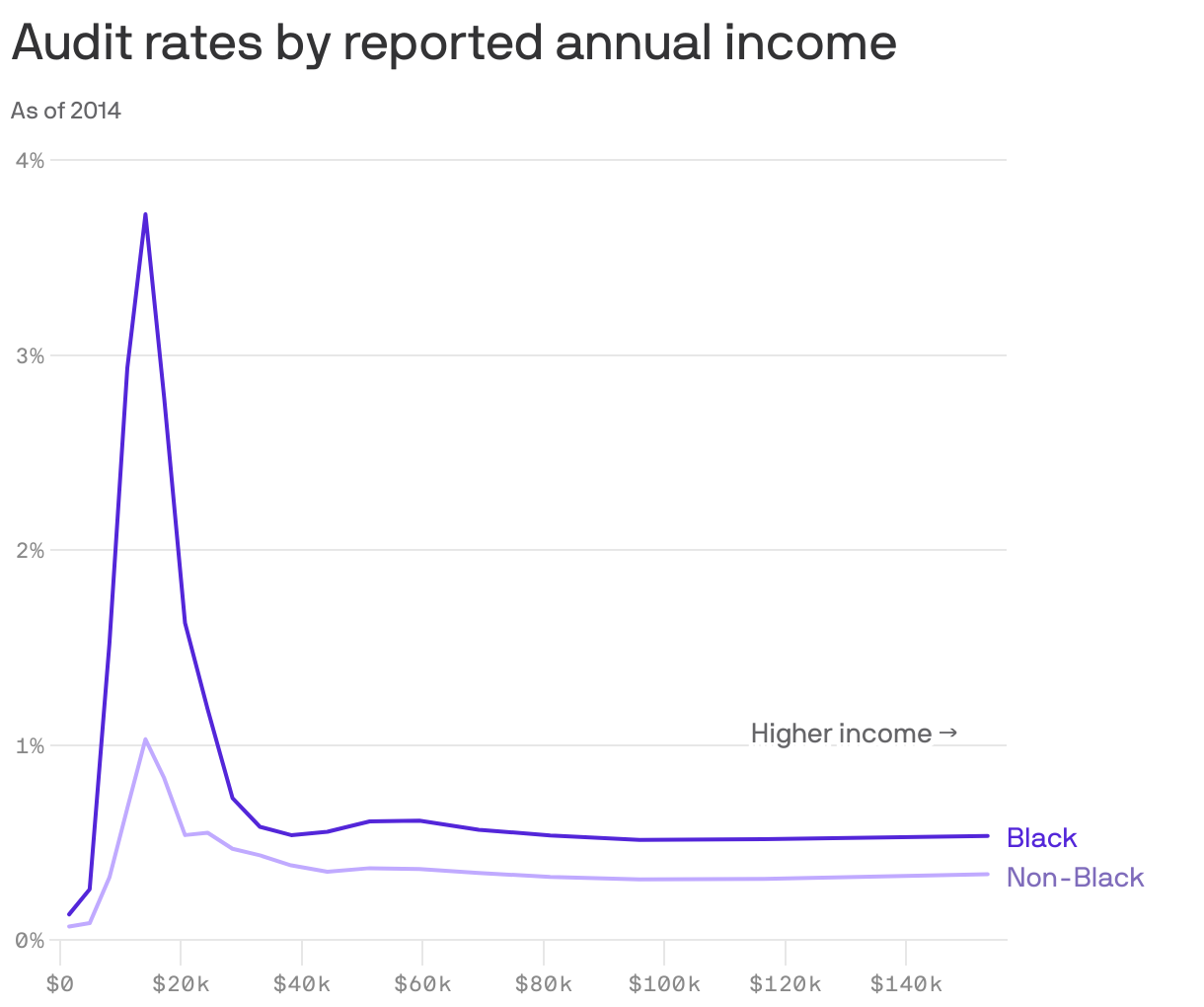

The bottom line: TikTok may not be a Chinese superweapon that is going to entertain an entire continent into submission. More realistically, its uncannily good algorithm is already being subsumed to capitalist imperatives. It might not be as fun as it used to be, but there's no sign anyone is leaving. | | | | | | | | 3. Who gets audited the most |  Data: Stanford Institute for Economic Policy Research; Chart: Axios Visuals If you're a single Black man with dependents who claims the Earned Income Tax Credit (EITC), you have a 7.73% chance of being audited by the IRS in any given year. For Americans as a whole, the equivalent figure is just 0.54%. - Single men with dependents claiming the EITC are also audited at a very high rate if they're not Black — 3.46% of them get the dreaded letter in the mail — but that number is still small when compared to their Black counterparts.

Why it matters: Black Americans at all levels of the income spectrum get audited at significantly higher rates, according to an extremely important new study conducted by Stanford researchers with the cooperation of the IRS. - The study used comprehensive data from 2014 — "the most recent year for which the vast majority of audits were complete and available to us," the researchers write.

The big picture: The biggest disparity, by far, comes among Americans claiming the EITC. When looking at EITC claimants, Black filers are much more likely than their non-Black counterparts to get audited. - "The racial audit disparity within EITC returns contributes 78% of the overall disparity," conclude the researchers.

Between the lines: As Axios' Emily Peck reported last year, EITC audits are much easier to conduct than audits of high earners, even though the rich tend to evade much more in the way of taxes. - Even within EITC audits, it's easier for the IRS to deal with filers who have no business income. Black filers constitute 21% of non-business EITC returns, but only 11% of business EITC returns.

- The IRS seems to be effectively ignoring the business returns: Non-business audits constitute 93% of EITC audits, despite the fact that business EITC returns have much more underreporting, in dollar terms.

How it works: The IRS does not observe race directly, and EITC audit selection is done by algorithm. But the algorithm design seems to be having a disparate impact on Black Americans. - Specifically, the algorithm seems much more likely to select tax returns where the chance of some kind of underpayment, even if small, is extremely high, rather than returns where the underpayment is likely to be largest.

- The latter returns tend to be filed by high-income taxpayers, and require much more work — and more experienced auditors — than the relatively automated audits of non-business EITC claimants.

The bottom line: It looks very much as though the problem of disparate algorithmic impact could be solved pretty easily — by changing the IRS auditing algorithm from being based on a binary "is this tax return likely to be false" question, to being based on the expected dollar amount of underpayment. - That, however, would mean an increase in the number of expensive auditors needed at the IRS. And Congress hates to increase the IRS budget, even when doing so pays for itself many times over.

My thought bubble: The even better solution would be to stop making everybody file a tax return in the first place. | | | | | | | | A message from SiriusXM | | Stream SiriusXM now and get 3 months for free | | |  | | | | Stream more than 425 channels on your devices for free on the SXM App, including expertly curated ad-free music, live sports, personalized stations and more. Next steps: Sign up now to get 3 months free. Cancel anytime. Learn more about the offer and start streaming. See offer details. | | | | | | 4. Building of the week: Cathedral of Learning, Pittsburgh |  | | | Photo: UPitt | | | | At 535 feet tall, the 42-story late Gothic revival Cathedral of Learning, in Pittsburgh, is the tallest educational building in the western hemisphere. - Designed by local architect Charles Klauder, the building, complete with cross-shaped floor plans, was built between 1926 and 1934. Ever since, it has served as the centerpiece of the main campus of the University of Pittsburgh.

| | | | | | | | A message from SiriusXM | | Get free access to music, sports, news and more | | |  | | | | Subscribe to SiriusXM Streaming and get access to 3 months of free: - Expertly curated ad-free music.

- Pandora artist stations.

- Live sports.

- Celebrity hosts, comedians and newscasters.

- Howard Stern and more.

More info: Listen on your phone, at home and more with the SXM App. See offer details. | | | | Thanks to Kate Marino for editing this newsletter, and to Elizabeth Black for copy-editing it. |  | | Why stop here? Let's go Pro. | | | | | | Axios thanks our partners for supporting our newsletters.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

To stop receiving this newsletter, unsubscribe or manage your email preferences. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment