| | | | | | | Presented By Fidelity | | | | Axios Markets | | By Felix Salmon · Aug 06, 2022 | | The weekday Markets team has left on vacation, but I'm still here today and next Saturday. Do reply to this email if there's anything you want me to cover next week. - This week, I'm looking at what happens when unicorns go public; a bank that isn't public but might as well be, in terms of the disclosures it needs to make; meme stocks; and the outcome of a high-profile NFT experiment. The whole thing is 1,449 words, a 5.5-minute read.

| | | | | | 1 big thing: Unprofitable unicorns' public pain |  | | | Illustration: Shoshana Gordon/Axios | | | | The current pivot to profitability in the world of venture-backed companies is far from unprecedented. What's new is the degree to which the gory details of corporate finances at former unicorns like Coinbase and Robinhood are now public. Why it matters: A private company can quietly battle on without its investors having to take any kind of write-down until the very end. When your financials are public, however, your struggles become public, too. - Last year's permissive IPO market showered listings — and the associated public scrutiny — onto hundreds of unprofitable companies.

How it works: When interest rates were low and liquidity was abundant, young companies realized that they could raise large sums of money at multi-billion-dollar valuations if they invested as much as possible in future growth — a very expensive strategy sometimes known as blitzscaling. - That strategy burns enormous amounts of cash, and it tends to end in disaster if the money stops flowing before the company achieves profitability. (Exhibit A: WeWork.)

- Now that money is more expensive and less abundant, it has stopped flowing to almost all such companies.

An IPO doesn't mean you're home free. Robinhood, which raised $2.1 billion in its 2021 IPO, is a good example. - This week, the millennial-focused broker-dealer announced losses of $295 million in the second quarter and laid off 23% of its workforce — just months after cutting 9%. So far in 2022, more than 1,000 of its employees have lost their jobs.

- Or see yesterday's WSJ and NYT stories on Coinbase.

The other side: Slightly earlier IPOs found themselves with enough time, before the music stopped, to start generating cash. - Airbnb this week announced it has become so profitable that it can afford to spend $2 billion buying back its own stock.

- Even the famously cash-burning Uber announced it was cashflow positive in the second quarter — although it still made a loss after accounting for things like stock compensation and its equity investments in other companies.

- "This marks a new phase for Uber, self-funding future growth," said Uber CFO Nelson Chai in a release.

The bottom line: All the formerly high-flying tech stocks have seen their valuations cut. Those cuts are much smaller for the likes of Airbnb and Uber, however — down 19% and 36% respectively since the date of Robinhood's IPO — than they are for companies like Robinhood, which has lost more than 70% of its value in its time as a public company. |     | | | | | | 2. The Varo Bank case study |  | | | Illustration: Sarah Grillo/Axios | | | | When Varo Bank raised $510 million last September it was flying high — and towards an IPO that could provide the privately-held unicorn an even greater sum. Then, the IPO window swung shut. State of play: Varo Bank is the only U.S. neobank — a branchless bank without overdrafts or monthly fees — to have its own bank charter. That, the bank argues, puts it in a stronger position than most of its competitors — but also means it has to file quarterly reports showing just how much capital it's burning. By the numbers: Varo lost $77 million in the second quarter, on top of a loss of $84 million in the third quarter. - That leaves the bank with $219 million of equity (assets minus liabilities), down $202 million in just three quarters from $417 million at the end of the third quarter of 2021.

What they did: Varo has laid off 75 employees and cut back sharply on marketing expenses. From here on, the focus is to save money where possible, and increase the number of customers using Varo as their primary bank. - "We're tapering back the heavy growth spending and some of the expensive customer acquisition," CEO Colin Walsh tells Axios. "We're not going to spend hundreds of millions of dollars on marketing to create an iconic brand."

Being a bank helps, at the margin. Varo says its cost of providing payment services has decreased by over 50% since it became a bank. - Varo can also lend out customer deposits to the Fed, which its competitors can't do since they don't own their deposits. It can also add Zelle, the interbank peer-to-peer payment service, which Varo is promising later this year.

Will it work? Walsh says that Varo will end the year with more than the $104 million of capital that he had when it became a bank, and that capital adequacy isn't what keeps him up at night. - But, but, but: Varo's business model is as yet unproven. Walsh has yet to demonstrate that he can persuade a critical mass of customers to use Varo as their primary bank — something that's necessary to bring the company to profitability, and reopen the possibility of an IPO.

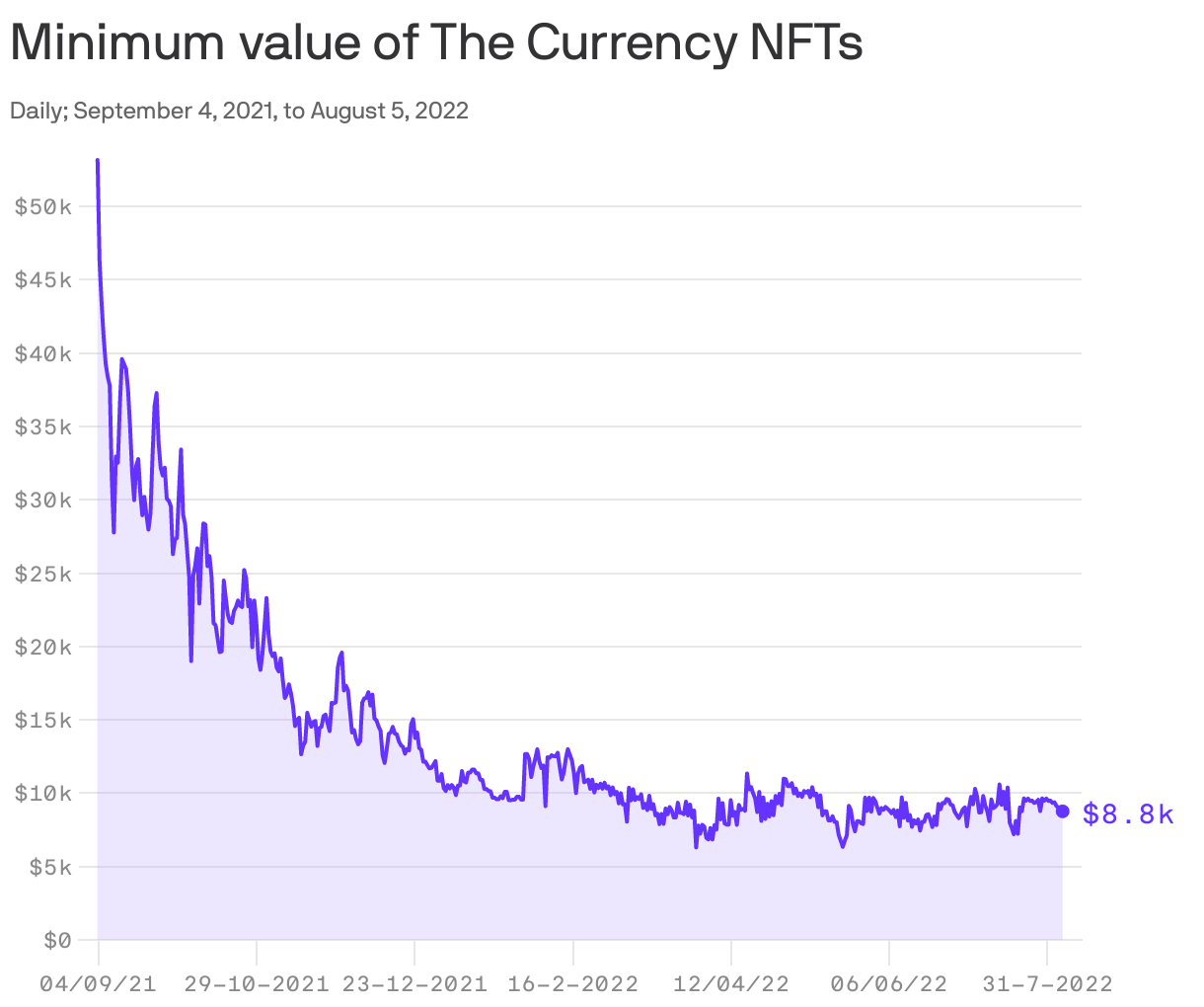

The bottom line: Varo's status as a bank makes its financial precariousness visible. Its more opaque competitors — think Chime, Aspiration, Revolut, N26, and the like — are all likely facing similar or worse economics right now. | | | | | | | | 3. Paper? Money? |  Data: NFT Price Floor; Chart: Axios Visuals When given the choice between physical and digital art, people prefer the physical. That's the verdict from one of the more interesting NFT experiments, which came to its major inflection point last week. How it works: UK artist Damien Hirst made 10,000 small (letter-sized) paintings on paper, in a series called The Currency. He then minted 10,000 NFTs, each one corresponding to one of the paintings, and sold 9,000 of them for $2,000 each. - The catch: The NFTs were freely tradable immediately, but after a year, the owners had to make a choice. Either "burn" the NFT in exchange for the physical artwork — or keep the NFT, in which case Hirst would set fire to the corresponding painting.

The verdict: Hirst decided to keep his NFTs and burn the corresponding paper works. After all, he already owns a huge amount of physical art by himself and others. - Of the other 9,000 NFTs, however, only 3,851 now remain. The rest were burned, exchanged for physical art. That's a 57% to 43% vote in favor of reality.

Why it matters: The NFTs are much easier to sell than the physical works — and, while they have fallen in value over the past year, they are still worth a lot more than the original $2,000 sale price. - Burning an NFT worth roughly $10,000 in order to get a physical painting is tantamount to buying the painting for $10,000. That's a lot of money for a small work on paper that's functionally identical to 5,148 other works, even if the piece of paper is signed by Damien Hirst.

The bottom line: The Currency seemed at first glance to be a kind of conceptual game, where participants were trying to anticipate whether the physical or digital artworks would be more valuable. In the end, however, I think people just chose whichever one they personally preferred to own. For most of them, that was something they could hang on their wall. | | | | | | | | A message from Fidelity | | You prep for your IPO — Fidelity has your back at every step | | |  | | | | Fidelity Stock Plan Services can provide equity compensation and management solutions that keep your momentum going — to and through life as a public company. Why it's important: Together, you can create equity comp solutions that work throughout your company's journey. | | | | | | 4. Don't call it a meme stock |  Data: FactSet; Chart: Axios Visuals An obscure company started trading on July 15, at $7.80 per share. By August 3 it traded, at one point, for $2,555.30 per share. It's a pattern that looks very familiar — but don't be fooled. AMTD Digital isn't a meme stock. Why it matters: Sometimes markets act in inexplicable ways; this was one of those cases. But there's no retail frenzy behind HKD, the ticker symbol of AMTD Digital, and there's no Discord server or Reddit thread full of teens investing their entire net worth in this crazy bet and trying to drive it to the moon. Between the lines: Consider Wednesday, the most frenzied day of trading. If you look at the minute-by-minute tape of that top tick, however, "frenzied" hardly describes what was happening. - There was one trade at 1:08pm at $1,800 per share, then a gap of six minutes where nothing happened, then another trade at $2,090, then a five-minute gap, one more trade at $2,200, another six-minute gap, and then the single $2,555.30 trade at 1:25pm.

- By Thursday afternoon, more than an hour passed without a single share trading hands.

Be smart: AMTD Digital is a small Hong Kong company that has a separate listing in New York. In no way should the company as a whole ever be valued by extrapolation from a single weird trade in its American depositary shares. The bottom line: Meme stocks act in weird but real ways — companies like AMC movie theaters can raise real money from their meme status, and hedge funds like Melvin Capital can lose money if they find themselves on the wrong side of a meme trade. - AMTD Digital, by contrast, is just odd. It saw a few bizarre trades, for reasons we can only guess. It's unlikely that any great fortunes were made or lost. Either way, don't blame the kids.

| | | | | | | | A message from Fidelity | | You drive growth — Fidelity drives your equity comp to match | | |  | | | | Fidelity Stock Plan Services provides equity compensation and management solutions for your company's journey to IPO and beyond. They keep your equity comp in sync with you, all the way. Why it's important: They can help you keep your momentum going — to and through IPO. | | |  | | Why stop here? Let's go Pro. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment