| | | | | | | Presented By OurCrowd | | | | Axios Markets | | By Matt Phillips and Emily Peck · Jun 28, 2022 | | 🚨 Since Russia invaded Ukraine in February, financial markets have emerged as a major theater of the war. - So today we're taking a time out from our usual day-to-day report to offer the latest on "the economic war," which could be just as crucial to the future of Ukraine — and the world — as the tank and infantry battles now underway.

This newsletter, edited by Kate Marino, is 1,210 words, 5 minutes. | | | | | | 1 big thing: Stalemate, for now |  | | | Illustration: Sarah Grillo/Axios | | | | The sense of shock and awe surrounding heavy sanctions on Russia early in the war has been overtaken by the reality that the economic battle — like the military assault — will be a slog, Matt writes. The big picture: "Right now neither side is winning the economic war if the goal of the economic war in the short-and-medium term is to induce political concessions from your adversary," Chris Miller, a professor at Tufts University's Fletcher School of Law and Diplomacy, tells Axios. "Neither side is getting ready to offer concessions. So in that sense, it's a stalemate." Driving the news: Group of Seven leaders this weekend prepared a plan to cap the price of Russian oil, another effort to weaken the keystone of Russia's financial durability: oil money. Why it matters: The G7's continued escalation is a tacit admission that efforts to isolate Russia economically have been insufficient to cut the flow of cash helping to finance President Vladimir Putin's war. - Despite some efforts to curtail purchases of Russian energy exports, soaring oil and gas prices — themselves, a reaction to the invasion — have poured funds into Russian state coffers.

- Russia's current account surplus — the broadest measure of a country's international trade — tripled to more than $110 billion so far this year, putting it on track for a record.

- The income boom has propped up the country's currency and stabilized inflation. That, in turn, allowed the central bank to scale back the emergency interest rate hikes it implemented at the beginning of the war.

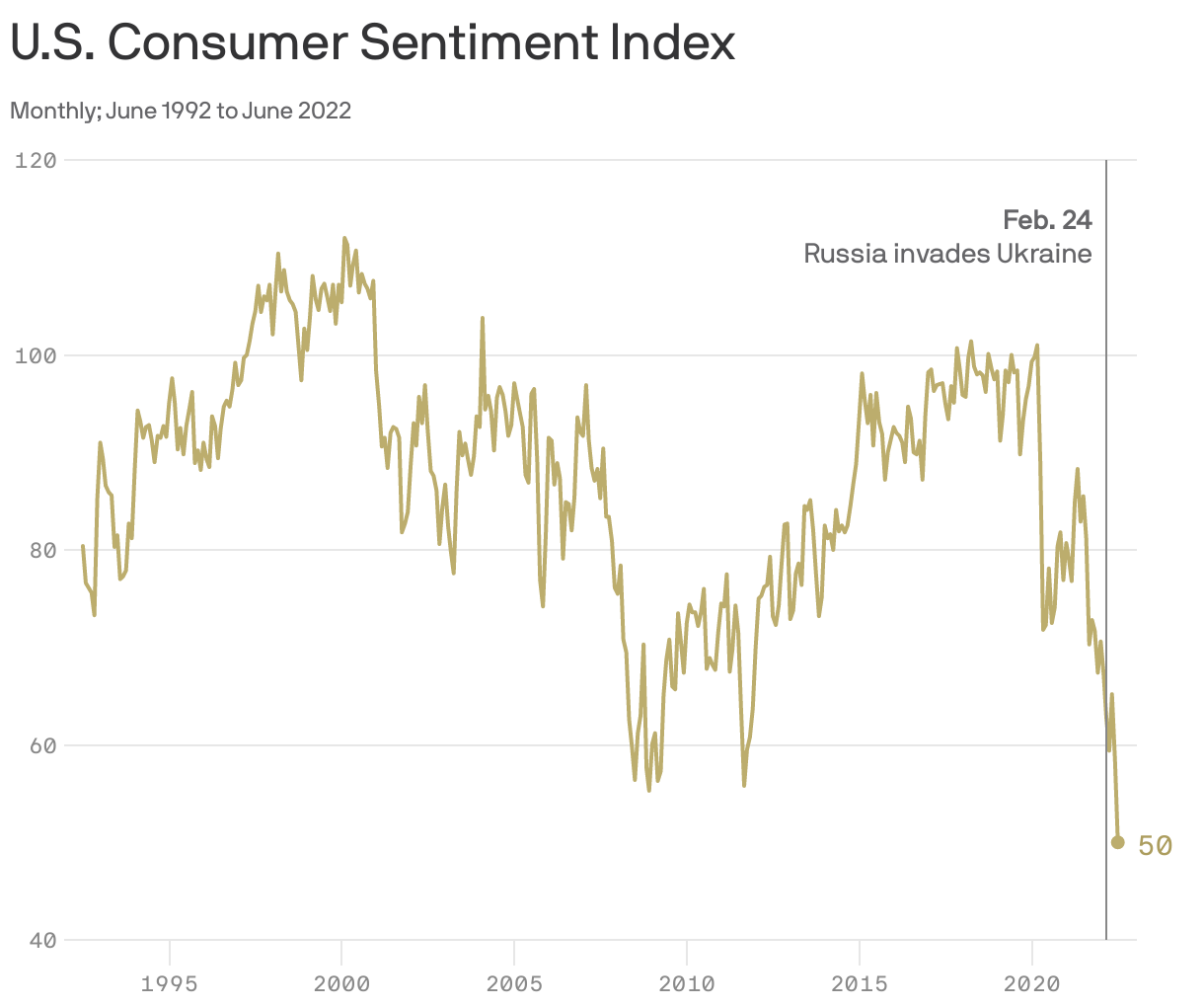

That doesn't mean the Russian economy is strong. Economists expect it to shrink by a massive 10% this year, largely driven by a collapse in consumer spending. The bottom line: Continued oil sales are helping Russia pay for the war. But the Russian people's standard of living is falling fast. |     | | | | | | 2. Blowback |  Data: University of Michigan, FactSet; Chart: Axios Visuals Russians aren't the only ones feeling the impact of the economic war. Ukraine's main backers in Europe and the U.S. now face soaring energy and food prices — linked to fallout from the war and more specifically, the West's sanctions. That's soured the public mood and eroded support for leaders, Matt writes. Why it matters: The key question is whether the big democracies of the world — already riven with internal divisions — can create a unified front to push back on Putin regardless of which party holds power. State of play: In Britain, Prime Minister Boris Johnson — a hawk on Russia — is in a perilous political position after being weakened by multiple scandals and a cost-of-living crisis. - The government of Germany's new Chancellor Olaf Scholz has begun preparing the population for rationing of natural gas — Russia is its top supplier — amid the risk supplies run out this winter. Its approval ratings are plunging.

- In the U.S., President Biden is contending with record-low consumer sentiment — the mirror image of record-high gasoline prices and a stock market meltdown — which could spell disaster for the Democrats in the coming midterm elections. Biden's approval rating is at a record low.

The bottom line: Analysts, like Gerard DiPippo at the Center for Strategic & International Studies, say that if the allies can maintain their support for Ukraine in the face of inflation, they clearly have the upper hand. - "In the long run, Russia's position is dire," DiPippo tells Axios.

- In the short-to-medium term, he adds, Putin "might have the ability to fracture the alliance, particularly if prices go higher. But in general, Russia is in a slow bleed mode."

Go deeper. | | | | | | | | Bonus chart: Ruble ricochet |  Note: Scale inverted; Source: FactSet; Chart: Axios Visuals Russia's currency cratered after it invaded Ukraine. - Since then, capital controls, interest rate hikes and oil revenues have fueled a rebound that reflects the country's financial resilience.

| | | | | | | | A message from OurCrowd | | Look beyond the stock market | | |  | | | | Explore VC investments at OurCrowd and find long-term potential outside the daily ups and downs of the stock market. OurCrowd vets hundreds of startups, then brings you a select few identified for their outsized growth potential. Go beyond the stock market. | | | | | | 3. Catch up quick | | 🍞 G7 leaders pledge $4.5 billion to address global food shortages caused by the war in Ukraine. (NYT) 🔥 Europe to resurrect old coal plants after Russia cuts gas flows. (Washington Post) 📉 Russia's economic slump will wipe out 15 years of gains. (Reuters) | | | | |  | | | | If you like this newsletter, your friends may, too! Refer your friends and get free Axios swag when they sign up. | | | | | | | | 4. How Russia skirts sanctions on energy |  Data: Kpler; Chart: Axios Visuals There's a big global sale on Russian oil right now if you're able to buy — with prices at least $30 less per barrel than European Brent crude, according to some estimates, Emily writes. Why it matters: Yes, the sanctions against Russia were swift and severe, but all this time Russia has been selling a whole lot of oil. The country has been able to offset a decline in oil sales to the West by increasing its sales to Asia. Details: India is importing 1.1 million barrels of Russian crude a day, according to data provided by Kpler, an analytics firm that tracks oil shipments. This time last year, the country was buying 173,000 barrels a day. - India effectively stopped buying crude from Nigeria, Angola, Mexico and the U.S. in favor of the cheaper Russian stuff.

- Meanwhile, China is importing more from Russia as well, but its demand is low as COVID-related lockdowns have resulted in a domestic stockpile.

- The cheap oil gives India and China a real edge at a time of soaring energy inflation — they can turn that crude into refined products and see higher profit margins than manufacturers that aren't buying the cheaper oil.

- The lower-priced oil is also tamping down inflation in the two countries, says Viktor Katona, lead crude analyst at Kpler.

What to watch: The next big shift in the market will come toward the end of the year when the EU stops importing seaborne Russian crude. Meanwhile, as the Chinese economy recovers from COVID lockdowns it could increase its imports — offsetting some of the EU's decline. Read the full story. | | | | | | | | 5. A tale of 3 bond defaults |  | | | Illustration: Aïda Amer/Axios | | | | When Russia defaults, that's generally a sign of financial carnage both inside and outside the country. That's what happened in 1918, and then again in 1998. This time, however, is different, Axios' Felix Salmon writes. Why it matters: The cost of Russia's default this week appears negligible — and in fact, there might be a benefit of defaulting, given that it could then retain possession of dollars that would otherwise go to foreign bondholders. The big picture: Countries that willfully default on their bonds can end up becoming financial pariahs. - But Russia is already cut off financially from most western governments, companies and payments systems. And it didn't willfully default on its debt obligations — in fact, it has sent all of its payments in full.

Flashback: Russia was the largest international debtor in the world when it repudiated all of its sovereign debts in 1918. It had the financial wherewithal to make bond payments; it just didn't have any desire to do so. - In 1998, Russia caused an international debt crisis when it defaulted on its domestic bonds (those denominated in rubles), which were broadly held by foreign institutions. Struggling with a weak economy, the government simply couldn't afford to keep on rolling them over.

This week's default is mostly a function of the way international financial plumbing works, with banks and clearinghouses barred from transferring Russian dollars to bondholders. The bottom line: While "default" is a scary word, Russia hasn't needed access to international capital for years, thanks to strong energy exports and relatively low domestic demand for imports. If you don't need to borrow money, then a bad credit rating does you little harm. Go deeper. | | | | | | | | A message from OurCrowd | | Market up, market down –– find alternative investments | | |  | | | | Find long-term investment growth opportunity outside the chaos of today's stock market. OurCrowd makes it easy for you to diversify your investments into a variety of expertly vetted, high-growth private companies. Invest alongside VC experts at OurCrowd. | | | | 🍸 1 thing Felix loves: an elegant corporate rebrand. Take the March 4 press release in which Stolichnaya (now Stoli), the world-famous Russian vodka, declared that it had been Latvian for decades. |  | It's called Smart Brevity®. Over 300 orgs use it — in a tool called Axios HQ — to drive productivity with clearer workplace communications. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment