| | | | | | | Presented By Northern Trust | | | | Axios Markets | | By Sam Ro ·Jul 30, 2021 | | Today's newsletter is 1,325 words, 5 minutes. 🎒of the day: 600,000, the number of backpacks Amazon sold on Prime Day. | | | | | | 1 big thing: Now's a great time to plan for a sell-off |  | | | Illustration: Shoshana Gordon/Axios | | | | The stock market is near all-time highs, which makes for a great time to plan for a big sell-off, even if you don't expect one to come. Why it matters: A sell-off that sends the stock market down 10% from current levels would be very average by historical standards. - Regardless of whether you expect the market to go lower, most would agree that it's better to formulate an investment strategy during times of calm than times of stress.

What they're saying: "I think we make the best decisions when they are in a vacuum," Invesco chief global market strategist Kristina Hooper tells Axios. - "It's very, very hard," she says of sell-offs. "You get caught up in the moment, and you just assume that whatever direction the market is this moment is the way it is going to be heading."

State of play: Hooper identified a handful of market headwinds that are on the radar of many investors. - There's the spread of COVID-19, which threatens to disrupt economic activity as infection rates rise in many regions of the world.

- The timing of tighter monetary policy is of high interest, as a premature move by the Federal Reserve could do more harm than good for long-run economic growth.

- And then there's the statutory debt ceiling, which the U.S. is expected to hit on Aug. 1. While there are short-term workarounds for this issue, congressional brinkmanship threatens to disrupt the Treasury's ability to finance the government's debts.

Threat level: "No bull market is completely devoid of setbacks," Edward Jones investment strategist Angelo Kourkafas says. - "Even the second-longest bull market on record (2009–2020) had its share of blemishes. During that period, there were six 10% corrections driven by a variety of factors, including growth scares, trade wars, oil prices and shifts in Fed policy," he says.

Yes, but: "What we have seen thus far is a market that rebounds rather quickly," Hooper says. "I wouldn't be surprised if we saw that again." The bottom line: There's no way to know for sure ahead of time if a sell-off will prove to be a buying opportunity or something far worse. But formulating a sell-off strategy before it happens seems like sound advice. |     | | | | | | 2. Catch up quick | | The SEC has stopped processing IPO registrations by Chinese companies as it updates guidance on disclosures, people familiar with the matter say. (Reuters) Amazon said its net sales jumped 27% to $113 billion in Q2, though its quarterly performance and expectations for the near future fell short of expectations. (Yahoo Finance) Tech investor Cathie Wood accumulated shares of Robinhood on the company's first day of trading. (Bloomberg) | | | | | | | | 3. Silver lining in the "disappointing" GDP report |  Date: Bureau of Economic Analysis; Chart: Axios Visuals U.S. GDP grew at a 6.5% annualized rate during the second quarter, a pace that fell short of some economists' expectations. But a closer look at the numbers suggests the report was far from disappointing. Why it matters: If the shortfall in GDP growth were due to a shortfall in demand, then there would be concerns the economy could be peaking. - However, shrinking inventories weighed heavily on the metric, suggesting lack of goods prevented higher levels of growth.

By the numbers: Real business inventories fell at a $166 billion annual rate in Q2, shaving 1.1 percentage points off of GDP growth during the quarter. What they're saying: "Supply chain constraints and shortages are a substantial part of the drawdown in inventories," High Frequency Economics' chief U.S. economist Rubeela Farooqi tells Axios. Yes, but: "The drag from inventories means that businesses have to rebuild stock, which will be a positive for growth," Farooqi says. The bottom line: The word "disappointment" has been thrown around a lot lately with little context. More often than not, shortfalls have been due to lack of supply available for a very healthy customer. - Also, 6.5% GDP growth is a blistering pace for a $19.4 trillion economy, which by the way is bigger now than it was before the pandemic.

- "Businesses cannot get the parts and products they need to meet this tremendous moment of demand," Wells Fargo senior economist Sarah House tells Axios. "But what hurts GDP today will be a help in coming quarters, as a much-needed rebuilding of inventories will mitigate the inevitable slowdown in spending."

| | | | | | | | A message from Northern Trust | | How investors can navigate a changing tax environment | | |  | | | | The prospect of higher tax rates has investors rightfully concerned about their bottom line. A new report from The Northern Trust Institute explores how to address unrealized gains in your portfolio and implement other tax-efficient investing strategies. Learn more. | | | | | | 4. How Credit Suisse failed at basic risk management |  | | | Illustration: Aïda Amer/Axios | | | | When Tidjane Thiam was fired as CEO of Credit Suisse in early 2020, the stated reason was his involvement in a spying scandal. Now that an incendiary report has been released by Credit Suisse about the bank's internal risk controls under Thiam's leadership, it looks like he was fired for the wrong reason, Axios chief financial correspondent Felix Salmon writes. Why it matters: The 165-year-old Credit Suisse, with its trillion-dollar balance sheet and 50,000 employees, is one of the most systemically important financial institutions in the world. The weakness of its internal controls, exposed by the collapse of the Archegos hedge fund, amounts to a major international scandal. The big picture: Credit Suisse lost $5.5 billion as a result of effectively lending Archegos money that the fund couldn't repay. What they're saying: The losses were "the result of a fundamental failure of management," concludes the 172-page report, written by a team of lawyers from Paul, Weiss. - "The Archegos risks were identified and were conspicuous," it says, but "business and risk personnel ... failed at multiple junctures to take decisive and urgent action to address them."

- One example: In August 2020, Credit Suisse calculated its "potential exposure" to Archegos at $530 million, vastly higher than the hedge fund's $20 million limit. The bank's "scenario exposure" — a different measure — was higher still. It also knew that the data underlying those calculations could be as much as six weeks out of date. Yet it did nothing.

Between the lines: Credit Suisse is making this report public because "Archegos is a stain on Credit Suisse's name," StoneTurn risk and compliance adviser Julie Copeland tells Axios. "Short of doing this, they would not be able to satisfy their customers, shareholders and regulators that they get it." - Thought bubble: The problem did not just lie with individuals. It was systemic and cultural, and it's not at all clear that the lumbering beast that is Credit Suisse is even capable of changing its ways to ensure that this cannot happen again.

The bottom line: The fear of all macroprudential regulators is that the world's largest banks are all too big to manage. This report will only reinforce their worst fears. Go deeper | | | | |  | | | | If you like this newsletter, your friends may, too! Refer your friends and get free Axios swag when they sign up. | | | | | | | | 5. Inflation goes online |  Data: Adobe Digital Economy Index; Chart: Connor Rothschild/Axios The deals you're getting online may not be as good as what you were getting a year ago. Why it matters: Shoppers have long understood that it's cheaper to buy goods online than in brick-and-mortar stores. - Up until 2019, the prices for goods online had actually been falling for years.

By the numbers: Adobe Analytics analyzed the online purchasing data of more than 1 trillion visits to U.S. retail websites. - Online prices declined steadily from 2015 to 2019, falling 3.9% per year on average.

- However, online prices in June increased by 2.3% from a year ago.

- While the number is up, it's still lower than the historic 5.4% jump in the U.S. Consumer Price Index during the same period.

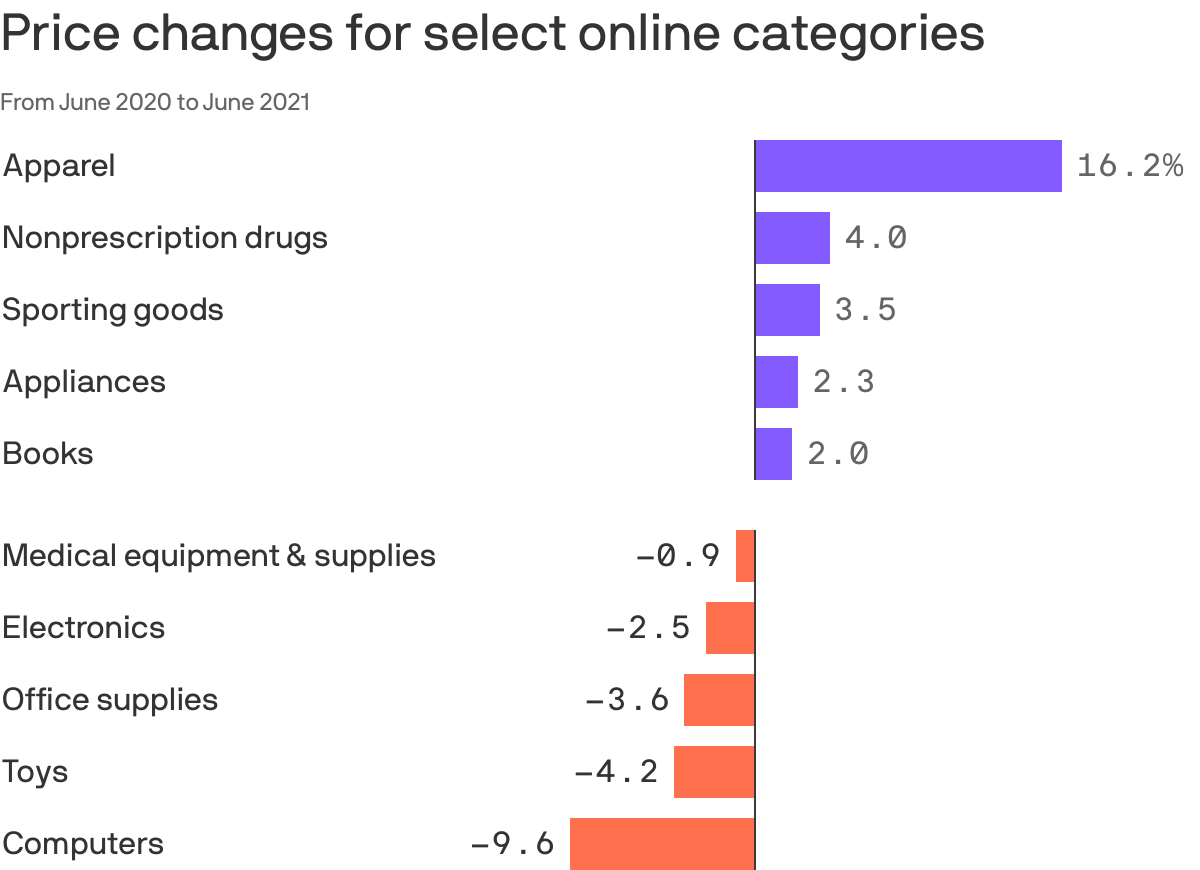

- Leading the online price gains were apparel, which was up 16.2%, and nonprescription drugs, which were up 4%.

- Though, online computer prices fell 9.6%, and online toy prices declined by 4.2%.

State of play: Shorter-term measures suggest prices remain on an upward trajectory. Online prices were up 1.2% month-over-month. This compares to CPI, which was up 0.9% during the period. The big picture: Behind all of the inflation figures — both online and offline — are shortages that are plaguing almost every industry as the reopened economy has come with demand far outstripping supply. The bottom line: Companies will continue to try to steal customers from each other by offering lower prices, and they'll aim to do it profitably by cutting costs and making their operations more streamlined. But there's not much they can do with pricing when margins are already thin and costs are rising. | | | | | | | | A message from Northern Trust | | How to prepare your portfolio for tax reform | | |  | | | | Prepare your portfolio and wealth plan for change with research-based insights on the likelihood of proposed tax policy changes and cutting-edge wealth planning strategies for managing complex wealth from The Northern Trust Institute. Ready for reform? | | |  | | It'll help you deliver employee communications more effectively. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Suite 1300, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment