| | | | | | | Presented By The Northern Trust Institute | | | | Axios Markets | | By Felix Salmon · Dec 03, 2022 | | I'm back from the Thanksgiving break but, after two days of Art Basel Miami Beach, not particularly rested. - In this week's newsletter: A new uncompromising attitude toward business; what's going on with Ghanaian bonds; Chinese wine (non-)consumption; and a missive from Miami. All in 1,410 words, a 5.5-minute read.

| | | | | | 1 big thing: The end of benefit of the doubt |  | | | Photo illustration: Shoshana Gordon/Axios. Photos: Jim Watson/AFP, Jeenah Moon/Bloomberg via Getty Images | | | | "Can you give the guy a break?" — Netflix CEO Reed Hastings, after being asked about Elon Musk at the NYT's Dealbook Summit on Wednesday No. We're in no mood to give Elon Musk a break. Nor ByteDance. Nor Sam Bankman-Fried. Nor, for that matter, the entire crypto industry. There's a new vibe in town, and it's unforgiving. Why it matters: The past 40 years or so have been characterized by a laissez-faire "let a thousand flowers bloom" attitude toward business ventures. Now that attitude's downside is apparent, and the backlash has begun. The big picture: The old theory was that of a typical VC fund. If you seed hundreds of ventures and most go to zero but a few show outsize returns of 100x or more, then both you and the broader ecosystem will prove very healthy. - The catch: Such logic ignores the possibility of negative returns much larger than -100%.

- When failure involves massive negative externalities — depositors losing their money, say, or Russia finding itself capable of influencing the 2016 U.S. presidential election — large upsides must be weighed against potentially devastating downsides.

Between the lines: Die-hard crypto acolytes are furious at Sam Bankman-Fried, at anybody who'd give him a platform, and at anybody who believes him. - They understand that the only way for crypto to survive the FTX implosion is to underbus Bankman-Fried individually, with extreme prejudice.

- After all, a world where Bankman-Fried might be telling the truth is a world where the entire asset class is inherently capable of spinning so far out of control as to endanger almost everybody exposed to it.

Be smart: That's more or less the view of the European Central Bank, which on Wednesday published an important blog post that pulls no punches when it comes to the crypto industry's massive hiring spree of former regulators. - Regulation, notes the ECB, is tantamount to an official seal of approval — which means that the only truly effective way to regulate crypto is to refuse to regulate it at all.

- The "let it burn" philosophy certainly has the advantage of simplicity: The more that authorities place crypto beyond the regulatory pale, and refuse to let regulated financial institutions touch it, the less danger it poses.

Where it stands: Musk this week created and then destroyed the idea that Apple had threatened to remove Twitter from its App Store — an idea born of Apple's longstanding zero-tolerance policy when it comes to any shenanigans on its platform. - App developers hate that policy, and the capricious way it's enforced, but they tend to grudgingly agree that it works well for Apple.

- Attempts to ban TikTok in the U.S. come from a similar place — no matter how much pleasure the app can bring to consumers, it could also pose an enormous geopolitical threat.

The bottom line: Banning a dangerous technology can be easier and more effective than fixing or regulating it. Expect that impulse to be indulged with increasing frequency. |     | | | | | | 2. The end of World Bank bond guarantees |  Data: Datastream; Chart: Axios Visuals When a country can't access bond markets on its own, the World Bank has twice stepped in with a partial guarantee — which in both cases turned out to be worth less than the original bond buyers had bargained for. Why it matters: That form of financial engineering tempted bond investors into thinking private-sector bonds might have the same seniority (so-called "preferred creditor status") afforded to World Bank debts. - In the first case, investors' hopes were dashed. The same thing looks possible in the second case, too.

How it works: If a country with such a bond misses a debt payment, then the guarantee kicks in; the World Bank makes the coupon payment to the bondholders, and the country owes the Bank instead. - Because the Bank is a preferred creditor, the country won't default on that obligation. And as soon as the Bank is repaid, the guarantee is reinstated, meaning that the next payment is covered, too.

The catch: The first time the Bank attempted this structure, with an Argentina bond issued in 1999, the cleverness evaporated on its first exposure to reality. Once Argentina inevitably defaulted in 2001, instead of demanding immediate repayment as bondholders had hoped, the Bank decreed Argentina could repay the money slowly between 2005 and 2009. - Something similar is happening now in Ghana. The nation is on the brink of default — which would manifest as a debt exchange where old bonds would be swapped for less attractive new ones.

- The World Bank, seeking to help Ghana as much as possible, has no particular reason to increase that nation's total debt burden by maximizing the amount it has to pay out on the 2030 bonds.

- As sovereign debt nerds Mark Weidemaier, Ugo Panizza and Mitu Gulati explain in the FT, holders of Ghana's 2030 bond — the one partially guaranteed by the Bank — could easily be caught up in the restructuring before the Bank makes even a single guarantee payment.

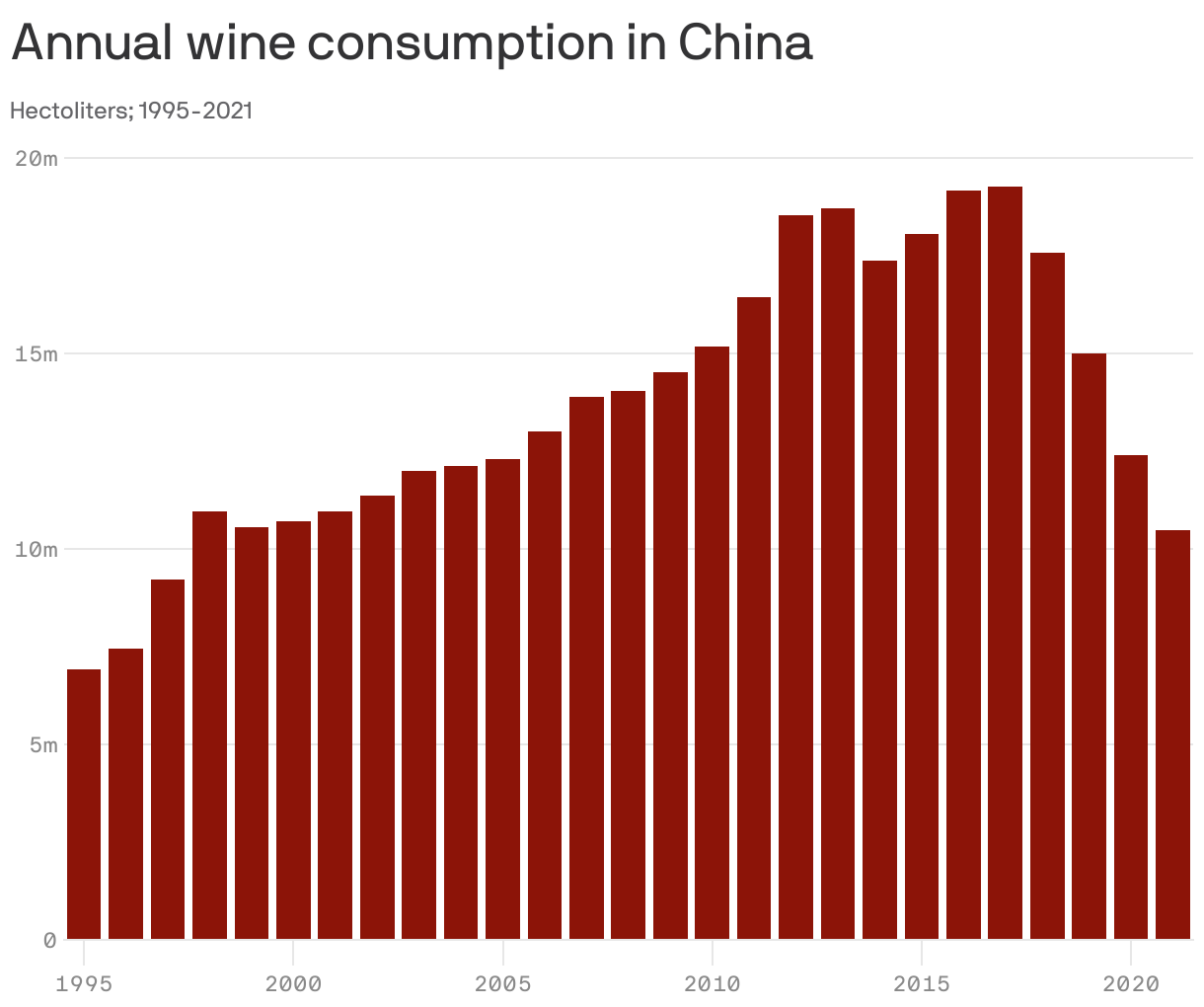

The bottom line: The partially guaranteed bond is still trading at a substantial premium to Ghana's other bonds. As FT's Robin Wigglesworth writes, if bondholders get minimal benefit from a World Bank guarantee for the second consecutive time, that structure seems to belong solidly in the "tried and failed" category. Go deeper: If you want to explore the details of what happened to the Argentina bond, and if you can get past the Euromoney paywall, I covered it in detail back in 2002. | | | | | | | | 3. The end of the future of wine |  Data: OIV Database; Chart: Axios Visuals Chinese wine consumption last year totaled just 10.5m hectoliters. That's the lowest number since 1997, when China's population was 200 million smaller and its GDP was a mere 5% of its 2021 size. Why it matters: Until 2013, China was considered the inevitable home of the future wine market. That now looks much less likely. The big picture: In most of the world, wine sales are overwhelmingly to people who want to drink the stuff. That's not the case in China, where only about 2.5% of adults drink wine at least once a month. - Instead, most wine is bought by people who don't intend to drink it. Instead, they give it away as gifts, during festivals like Chinese New Year, the Mid-Autumn Festival, or Singles Day.

- The pandemic caused massive disruption to Chinese gift-giving, as wine fell out of favor. Perhaps people realized the recipients weren't drinking their gifts.

The bottom line: Just as in the rest of the world, people who drink wine at home ended up drinking more of it during the pandemic. But so far there's no indication that China's population is going to become a global force in the wine world. | | | | | | | | A message from The Northern Trust Institute | | The Entrepreneur's Guide to Building Wealth | | |  | | | | Whether you are focused on growing your business or preparing for an exit, a solid wealth plan is critical for entrepreneurs at every stage. Next steps: Read Northern Trust's guide to explore insights for building and sustaining your wealth. Learn more. | | | | | | 4. The most Miami artwork in Miami |  | | | Photo: MSCHF | | | | The ATM is the new banana. Why it matters: Art Basel Miami Beach is the art fair that best exemplifies the triumph of buzz over connoisseurship. Three years ago, the buzz surrounded a banana; this year, it's a machine that displays your checking account balance for all to see. The big picture: The work, by MSCHF, is a critique of the vulgar exhibitionism that Miami is famous for year-round, but especially during art week; it's also the prime example of it. How it works: Anybody (or at least anybody who has gained access to the art fair) can participate in the work by inserting their ATM card, entering their PIN, and checking their balance. The artwork then displays their balance on a leaderboard, highest balance first, accompanied by a photograph of the person who inserted the card. - When Axios last checked, the top score was held by a man in a pink T-shirt boasting a $2.9 million balance.

Between the lines: The hypebeast culture that MSCHF emerged from is driven by self-loathing consumers who buy brands' output despite knowing it has no intrinsic quality, just because they also know that it is worth more on the secondary market than they are paying for it. - All parallels to the primary art market are entirely intentional.

The bottom line: Miami is the spiritual home of people who really want other folks to know how rich they are. MSCHF has now given them a way of doing exactly that, protected only by the thinnest veneer of irony. | | | | |  | | | | If you like this newsletter, your friends may, too! Refer your friends and get free Axios swag when they sign up. | | | | | | | | 5. Building of the week: Wrigley Building, Chicago |  | | | Photo: Raymond Boyd/Getty Images | | | | The Wrigley Building, on Chicago's Magnificent Mile, opened in 1921 to a Beaux-Arts design by local architect Charles Beersman, modeled on the 12th-century Giralda Tower in Seville. The bottom line: Axios Chicago readers really don't like modernism. | | | | | | | | A message from The Northern Trust Institute | | Market Currents podcast: Listen now | | |  | | | | Market Currents, a new podcast from The Northern Trust Institute, explores today's most hotly debated investment topics. Join host Katie Nixon as she interviews industry experts to investigate the evidence on both sides. Listen today. | | | | Thanks to Kate Marino for editing this newsletter, and Rob Reinalda for copy-editing it. |  | | Why stop here? Let's go Pro. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment