| | | | | | | Presented By Fidelity | | | | Axios Markets | | By Felix Salmon · Jul 30, 2022 | | I hope you won the lottery last night. Failing that, I hope nobody won, so that you get another shot at a billion-dollar jackpot on Tuesday. - In this week's newsletter, I've decided to embrace the weird, while also taking the (rising) temperature of crypto regulation. Plus, millennial wealth, and more. All in 1,285 words, a 5-minute read.

| | | | | | 1 big thing: It's stopped making sense |  | | | Photo illustration: Annelise Capossela/Axios. Photos: FPG, Heritage Art/Heritage Images via Getty Images | | | | There's an air of unreality to the news these days — one perfectly in keeping with the "nobody knows anything" vibe that arrived with the onset of the pandemic in 2020 and never really left. Why it matters: Recent days have seen a flurry of headlines that feel as though they've been run through an impossibility drive. - My job, as a newsletter writer, is to make sense of those headlines and to deliver you a story that explains them. But the honest truth is that there is no such story, and that things are very messy and weird right now — not always in a bad way.

Driving the news: The economy has spent the past six months shrinking, per the official Q1 and Q2 GDP reports. Other data, like gross domestic income (GDI), tell a different story — as does the labor market. The strong dollar cuts both ways, depending on how you look at it. In Washington, the announcement on Wednesday that the Inflation Reduction Act would likely pass the Senate upended all manner of conventional wisdom. Among the impossible things that happened: - Senator Joe Manchin went from fickle obstructionist to master tactician overnight. Larry Summers became a hero to the left.

- America has some claim now to be a climate leader, should this bill pass and succeed in reducing U.S. carbon emissions to 40% below 2005 levels by 2030.

- The global 15% minimum corporate income tax is now back on the front burner — and there's a decent chance that the carried interest tax loophole, much beloved of private equity and venture capital executives, will finally be abolished.

The big picture: The pandemic precipitated an epistemic crisis, as well as a medical one. To this day, the amount we don't know about the SARS-CoV-2 virus is enormous, and the uncertainty around economic and financial issues is just as large. Between the lines: Inflation is creating cognitive disconnects everywhere. Second-quarter growth came in at an annual rate of $24.9 trillion, for instance, up 2% from the $24.4 trillion seen in Q1 and up more than 9% from the $22.7 trillion a year previously. - A mature business that saw revenues rise 2% in 3 months and 9% in 12 months might be thought to be doing OK. But after accounting for inflation, Q2 GDP declined by 0.2% quarter-on-quarter, which is definitely not good (although it could yet be revised upwards).

The bottom line: If you are clinging to a simple narrative that explains the current situation, where a character like Vladimir Putin or Joe Biden or Jay Powell is determining the outcome of the global economy, you are wrong. - Everything is in a messy flux right now, and no one is holding the reins.

|     | | | | | | 2. Regulator sympathy for crypto evaporates |  | | | Illustration: Aïda Amer/Axios | | | | Inflicting billions of dollars in losses is a great way to lose sympathy among politicians. - Time has run out: It's too late for the crypto industry to get the kind of regulation it's been pushing for. The crypto winter arrived before any new laws could be written, and has changed the whole tone of the debate in Washington.

Why it matters: Crypto insiders have long dreamed of a world where everything they do is carved out into their own bespoke regulatory regime: one primarily designed to encourage innovation, and that doesn't try to apply 20th century laws to a 21st century financial system. - That dream has, realistically, died.

The big picture: Regulation, by its nature, tends to concentrate on minimizing harm rather than maximizing capital formation. Right now, the harm caused by crypto is more visible than ever, while any real benefits seem small in comparison — and shrinking fast. Driving the news: Documented crypto frauds have topped $1 billion, according to the FTC. The Federal Reserve is furious at Voyager Digital for saying that it was FDIC-insured. The FBI is warning of cryptocurrency scams, and the Senate is holding hearings on them. The SEC is beefing up its Crypto Assets and Cyber Unit — and, Bloomberg reports, is investigating Coinbase for illegally trading in securities. How it works: The SEC, from its earliest days, has been charged with overseeing a level playing field, where no one has an unfair advantage. By necessity, that has to be done by reducing the ability of the rich and powerful to take advantage of the little guy — something that's been endemic to crypto for years. - Meanwhile, a tone-deaf Coinbase is proudly putting out animated videos of self-described degenerates wreaking havoc in a dystopian future. Such shenanigans fatally undercut any attempt to paint themselves as a grown-up and sober financial institution.

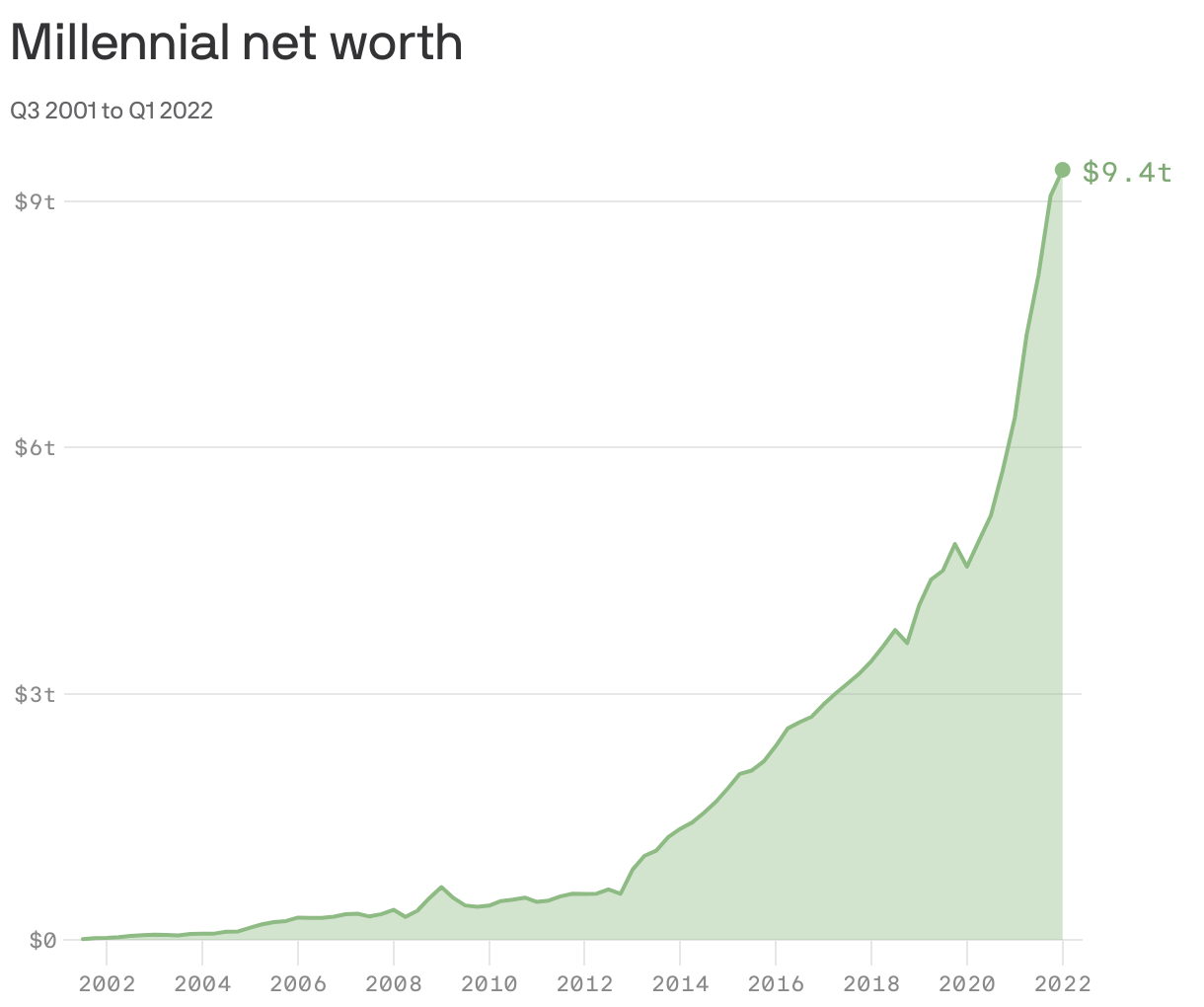

The bottom line: Crypto still has some friends left in Congress — but not nearly enough of them to pass any new laws any time soon. Meanwhile, regulators are baring their teeth, and none of them have any visible desire to cut the industry any slack. | | | | | | | | 3. The first $10 trillion is always the hardest |  Data: The Federal Reserve; Chart: Kavya Beheraj/Axios Millennials are twice as rich as they were before the pandemic. Why it matters: The recession arrived when millennials — anybody born between 1981 and 1996 — were feeling burned out and doomed. Student loans were stretching as far as the eye can see, and millennial wealth was just a fraction of what previous generations had managed to accumulate at the same age. - The pandemic changed everything. Student loans payments were paused, government stimulus checks started pouring in, the stock market soared, and house prices spiked.

Where it stands: Millennials had an average of $127,793 in net worth in the first quarter of 2022. - When Boomers were the same age, in 1989, their net worth (in 2022 dollars) was a comparable $136,786, according to Kali McFadden, a data research manager at LendingTree.

The catch: While millennials' wealth has risen very quickly in percentage terms, it's still tiny compared to other generations in absolute terms. While millennials gained $4.8 trillion of wealth in two years, Generation X gained $16.4 trillion, and now have some $42 trillion in total. The bottom line: Millennials are not yet rich, but at least they're finally on their way. | | | | | | | | A message from Fidelity | | You drive growth — Fidelity drives your equity comp to match | | |  | | | | Fidelity Stock Plan Services provides equity compensation and management solutions for your company's journey to IPO and beyond. They keep your equity comp in sync with you, all the way. Why it's important: They can help you keep your momentum going — to and through IPO. | | | | | | 4. Millennial homeownership hits 50% |  Note: Millennials were considered to be those born between 1981 and 1996. Homeownership rates are for those 18 and older. Data: U.S. Census Current Population Survey; Chart: Erin Davis/Axios Visuals One of the key reasons that millennials saw their wealth rise so quickly during the pandemic is that they started their home-buying spurt just in time. By the numbers: Between 2016 and 2022, millennial homeownership soared from 36% to more than 51%. - The Census Bureau chart above actually understates the degree to which homeownership rose. That's because it only includes "householders" — people who have a mortgage or a lease in their own name. So in the earlier years, millennials in dorm rooms or living with their parents weren't even counted in the denominator.

How it works: Recent first-time homebuyers tend to be the most leveraged, magnifying returns in up markets. - If you put down a 10% downpayment, and your house goes up in value by 50%, then the equity you have in your home goes up by six times.

The bottom line: Many millennials got onto the housing ladder just in time. | | | | |  | | | | If you like this newsletter, your friends may, too! Refer your friends and get free Axios swag when they sign up. | | | | | | | | 5. Building of the week: Balfron Tower, London |  | | | Photo: Sam Mellish / In Pictures via Getty Images | | | | Ernő Goldfinger — the Hungarian-born Brutalist architect so loathed by Ian Fleming that the novelist named a Bond villain after him — designed Balfron Tower, in London, in 1963. - The separated service tower, which includes machinery like elevators, water pumps, and garbage chutes, helps keep the 146 apartments quiet. Arrayed along "streets" in the sky, they're designed to foster neighborliness.

By the 1990s, the tower — once described as imparting "a delicate sense of terror" — had fallen on hard times, and was eventually sold off to a developer, Londonewcastle. - The formerly working-class apartments are now luxury flats, priced between $455,000 and $975,000 — with Goldfinger's own top-floor apartment likely to go for even more through a sealed-bid auction.

Go deeper: The Guardian's Olly Wainwright visits the new development. | | | | | | | | A message from Fidelity | | You move boldly — Fidelity keeps your equity comp in step | | | | | | | | Fidelity Stock Plan Services provides equity compensation and management solutions grounded in decades of experience. They can anticipate your equity comp needs along the way. Why it's important: They can help you keep your momentum going — to and through IPO. | | |  | | Why stop here? Let's go Pro. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment