| | | | | | | | | | | Axios Pro Rata | | By Kia Kokalitcheva · Jul 30, 2022 | | Welcome to another special edition of our weekend newsletter! - This time we're talking climate change (again), with contributions from my colleagues from the Generate and Pro Climate tech teams, edited by Axios Pro's George Moriarty.

- 📪 Try out Axios Pro and get $200 off any Axios Pro subscription by using code PRO200 at checkout.

Today's newsletter is 1,172 words ... 4½ minutes. | | | | | | 1 big thing: Climate insurance is risky business |  | | | Illustration: Shoshana Gordon/Axios | | | | Insurance startups are eyeing the climate space as historical models struggle to keep up, but experimental underwriting models may not be a silver bullet, writes Axios Pro's Megan Hernbroth. Why it matters: Insurance models have struggled to keep up with the pace of climate-related claims, but there's no clear sailing for new insurance concepts. Context: Traditional insurance coverage for businesses and individuals relies on historical data to predict the likelihood of a qualifying event and adjust the policy accordingly. - Insurance companies themselves are insured through reinsurance, which helps distribute the underlying risk to preserve solvency during large qualifying events.

State of play: Those historical models are less reliable in a world with increasingly severe weather events due to climate change, so some insurance startups have opted to explore alternative models. - Sensible, for example, provides something akin to a guarantee product for consumers via a refund should a severe weather event damage an asset.

- This is what Aon Securities CEO Paul Schultz calls a parametric approach to risk diversification, where either the qualifying event happens or doesn't.

- It's a common model in less-mature markets as well, Schultz explained, due to the unreliable nature of historical data.

Yes, but: Inflation is taking its toll on the insurance industry broadly, and young startups with lines of credit may not be able to keep up with the more established groups. - Asset prices are increasing faster than insurance policies are revised, meaning a company could end up paying out more than it collects should a qualifying event hit a rapidly appreciating asset.

- Credit markets are tight on the heels of yet another interest rate hike, and early-stage insurance startups may not be able to convince investors to overlook the underlying business costs for an unproven model.

- And those that can get credit face increasing costs, pushing margins even lower.

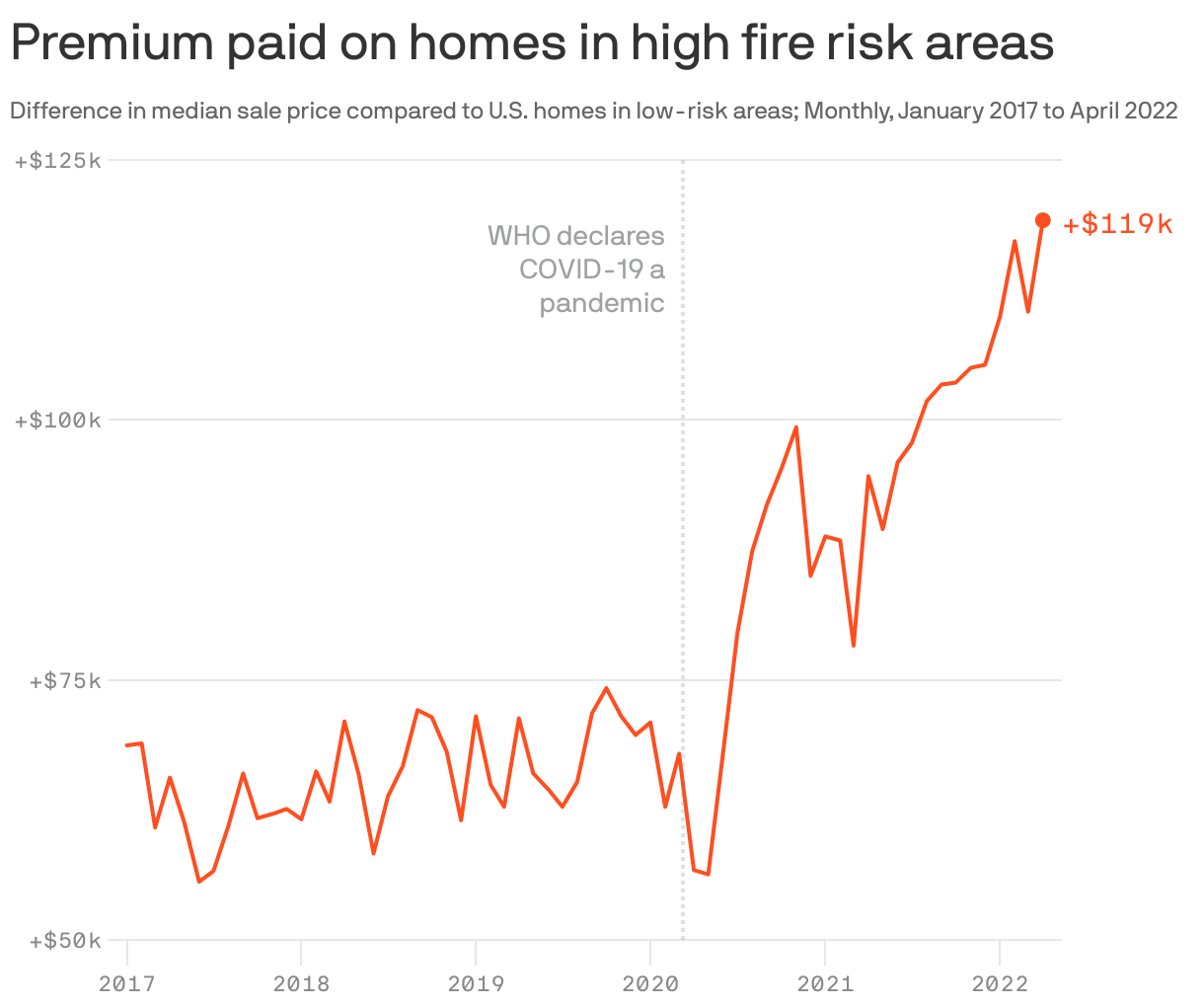

The bottom line: Experimental models do not insulate startups, and investors by extension, from the risky future ahead. |     | | | | | | 2. Homebuyers add climate risk to checklist |  Reproduced from Redfin; Chart: Axios Visuals Home shoppers have more information than ever to see how a potential new home will be threatened by wildfires, floods, heat and other climate risks. But research shows that large swaths of homebuyers and renters can't (or don't) act on that data, writes Axios Pro's Alan Neuhauser. Why it matters: Climate-risk data can empower decision-makers, but it can also exacerbate inequality. What's happening: Each listing on Redfin and Realtor.com now includes "Climate Risk" scores: a 0-100 gauge of how likely a flood, fire, severe storm, drought or extreme heat will strike the home. - The data is supplied by First Street Foundation, a nonprofit working to map climate risk.

What they found: Communities of color face a disproportionate risk of flooding and extreme heat. - Redlined neighborhoods are 5 degrees hotter than non-redlined areas, per a 2020 study that attributed the trend to the urban heat-island effect.

- And when it comes to flooding, 8.4% of homes in redlined areas face high flood risk, compared with 6.9% of homes in non-redlined areas, per Redfin.

Yes, and: Research is underway, but one hypothesis is that climate intelligence could entrench these inequities by further depressing home values in areas that are still marked by the impacts of segregation. - "People ... can't get equity to compensate them to move," Redfin chief economist Daryl Fairweather tells Axios.

- A greater number of families who live in formerly redlined areas are renters rather than owners — and renters, at least in theory, have more flexibility to move.

Yes, but: There are also plenty of high-net-worth areas that have seen huge investment despite the climate risks. Miami has boomed despite hurricane and sea level threats, and ski towns like Tahoe, Park City and Aspen have grown in the face of severe fire risk. - "There may be a 1% risk each year," First Street Foundation CEO Matthew Eby tells Axios. "But when you have cumulative risk of 1% every year over 30 years, you have a 1 in 4 chance of being impacted by that event."

Meanwhile: Then there's the middle-band: Homebuyers forced out by astronomical home prices in certain sections have to accept a suburb in central or northern California that will likely experience a wildfire. - "People sacrifice on climate risk because it's abstract, it's in the future, versus looking at your monthly mortgage payment, which is a lot more tangible," Redfin's Fairweather says.

| | | | | | | | 3. Hurricane season to allow some companies to showcase their tech |  | | | Illustration: Brendan Lynch/Axios | | | | The 2022 Atlantic hurricane season is likely to be unusually active, with worrisome signs in parts of the Atlantic, Caribbean and Gulf of Mexico, writes Axios' Andrew Freedman. The big picture: While hurricane forecasters' main tools are provided by the federal government — such as the National Oceanic and Atmospheric Administration (NOAA) and Air Force hurricane hunters, satellites and computer models — startups are playing a growing role in forecasting. Zoom in: As it did last year, San Francisco-based Saildrone will be fielding a handful of its remotely operated, heavily instrumented drones, which resemble surfboards with sails, near and even into tropical storms and hurricanes. - Its research program conducted with NOAA scored a big payoff last year, when one drone in its fleet sailed into the heart of then-Category 4 Hurricane Sam.

- The video it relayed back was widely shared, showing tumultuous, white-cap dominated seas.

- The drones are being used to study an area of the storm that hurricane hunter aircraft cannot safely evaluate — the border between the turbulent ocean water and the air.

- Knowing more about the exchange of heat between the sea and air could allow for improved hurricane intensity predictions.

Between the lines: In addition to NOAA and NASA's imagery, venture-backed satellite firms, such as ICEEYE and Planet, can provide detailed imagery of a storm's impact on land to help disaster assistance providers analyze the damage, even far from the coasts. - Providers of synthetic aperture radar images, such as ICEEYE, can pinpoint flooding on the land surface through cloud cover, which can give them an advantage over purely visible imagery platforms.

- In addition, private-sector weather and climate intelligence firms, such as tomorrow.io, work to provide clients with information they need to anticipate and mitigate storm-related risks.

- There are also an increasing number of private-sector satellite networks deployed or planned from operators like Spire and Capella Space, which could be used to enhance the data that flows into NOAA's computer models used for predicting a storm's path and intensity.

The bottom line: What was long a solely federal function, gathering data and predicting tropical storms and hurricanes, is now becoming more diverse, and hopefully, more accurate as well. | | | | | | | | A message from Axios | | The news you need in 10 minutes. | | |  | | | | Catch up on the biggest stories of the day and why they matter with the Axios Today podcast. Host Niala Boodhoo is joined by journalists from Axios' newsroom to unpack the stories shaping your city and the trends shaping our world. Listen for free. | | | | | | 📚 Due Diligence | - A $369 billion gold rush (Axios)

- Turning to drones and other instruments to hunt hurricanes (Marketplace)

- Why big financial firms are scooping up climate modeling companies (Axios)

| | | | | | | | 🧩 Trivia | | Climate disasters have triggered some of the biggest insurance payouts in history. - Question: Which disaster led to the biggest one in the U.S.? (Answer at the bottom.)

| | | | | | | | 🧮 Final Numbers |  Data: PitchBook; Chart: Nicki Camberg/Axios | | | | | | | | A message from Axios | | The news you need in 10 minutes. | | | | | | | | Catch up on the biggest stories of the day and why they matter with the Axios Today podcast. Host Niala Boodhoo is joined by journalists from Axios' newsroom to unpack the stories shaping your city and the trends shaping our world. Listen for free. | | | | 🙏 Thanks for reading! See you Monday for Axios Pro Rata's weekday programming, and please ask your friends, colleagues and climate tech investors to sign up. Trivia answer: Hurricanes Katrina, Rita and Wilma in 2005 led to payouts totaling $130 billion. |  | | Why stop here? Let's go Pro. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment