| | | | | | | Presented By Ripple | | | | Axios Markets | | By Matt Phillips and Emily Peck · Apr 18, 2022 | | 🤌 Welp, it's Monday and tax day. Emily's got the lowdown on filing this year. We're also mulling the impact of rising rates on companies and homeowners, and the future of high inflation. Let's go! Today's newsletter is 1,177 words, 4.5 minutes. | | | | | | 1 big thing: Corporate credit is still very loose |  Data: Moody's; Chart: Axios Visuals Corporate credit is defying the Fed's push for tighter money, Axios' Neil Irwin writes. - Recently, corporate bond yields have fallen relative to Treasuries, meaning businesses lending conditions are still highly stimulative. It is one of many signs that markets have not tightened nearly as much as might be expected, given the Fed's policy U-turn.

Why it matters: The Fed's strategy to rein in inflation is premised on tightening the screws on credit — but based on the results so far, it may need to get even more aggressive. By the numbers: Since the Fed's shift began in early November, the 10-year Treasury yield has surged (from 1.55% to 2.83%), as has the average rate for a 30-year fixed-rate mortgage (3.09% to 5.00%). - Initially, corporate borrowing costs rose faster, as typically happens when the Fed tightens, which is partly how monetary policy slows the economy. But in the last month, the usual pattern hasn't applied: The spread between risk-free rates and corporate bond yields has narrowed.

- Last week, Aaa-rated bond yields were 1.07 percentage points higher than Treasury yields, according to Moody's data, about the same spread as early November and down from 1.55 percentage points on March 8. It averaged 1.62% in the decade of the 2010s.

One likely factor: The Fed's decisive moves toward "quantitative tightening" will mean shrinking its $9 trillion bond portfolio by up to $95 billion a month. The policy has more direct effects on Treasuries and mortgages (via runoff of mortgage-backed securities) than on corporate bonds. Still, narrowing corporate debt spreads are evidence that — for all the talk of recession risk — conditions remain highly accommodative for corporate America. Also, the S&P 500 is down only 4.8% since the start of November, hardly the kind of drop that signals tightening. As of last week, Goldman's Financial Conditions Index, which incorporates rates, stock valuations and credit spreads, showed financial conditions were looser than nearly all of the 2010s. Yes, but: There is also the risk of overdoing it, and causing a freeze-up of business credit that causes a recession, or a crisis. What they're saying: "It's tough to pinpoint a yield level where this would 'break' the market or the economy," Mike Larson of Weiss Ratings tells Axios. - But given high inflation, rising rates and volatility, "it's the kind of thing that could definitely cause problems for corporate America the more the Federal Reserve decides to tighten the screws."

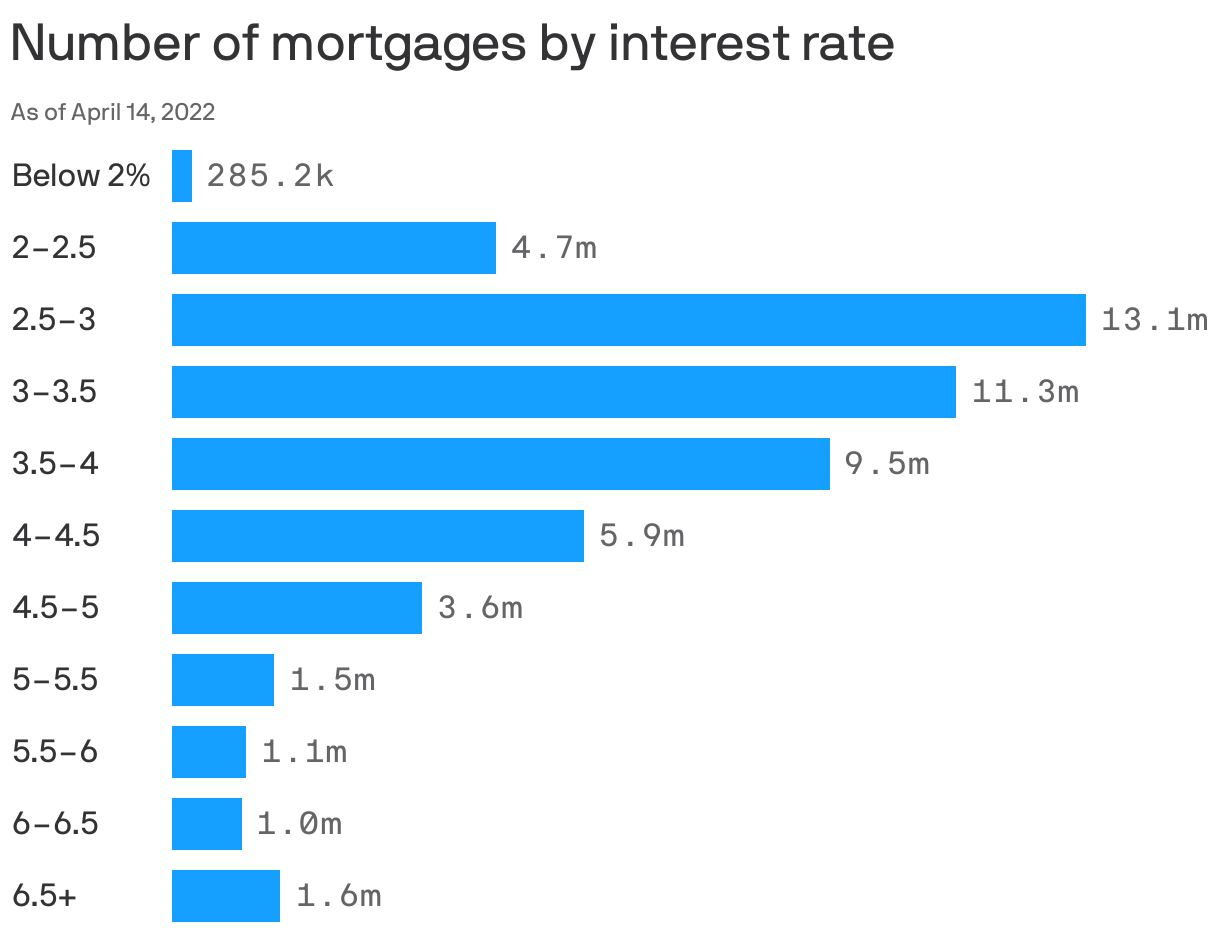

The bottom line: Corporate credit is still very flush. If the Fed really wants to slow down the party, it appears to have lots of work to do. |     | | | | | | 2. Catch up quick | | 📈 China's economy grew 4.8%, but challenges lie ahead. (WSJ) 🍎 Apple's workers at NYC store move toward union. (Axios) 🚢 Massive ship freed from the Chesapeake Bay. (Axios) 📈 Bond rout promises more pain for investors. (WSJ) | | | | | | | | 3. Why homeowners aren't selling |  Data: Black Knight; Chart: Axios Visuals Nine out of ten American mortgages carry an interest rate of less than 5%, the official level at which most new 30-year fixed-rate mortgages are now being written, Axios' Felix Salmon writes. Why it matters: Houses are affordable — if you already own one. According to Fannie Mae's most recent survey, 92% of homeowners say their current home is affordable. More impressively, 91% of lower-income homeowners say the same thing, up from 79% at the end of 2017. Yes, but: Were those homeowners to move, they would need to pay substantially more in interest. The big picture: If you hold a mortgage that's cheaper than what you'd need to pay if you moved, that's a significant incentive to stay put. The result is that thanks to supply-and-demand dynamics, increased mortgage rates are less likely to mean lower home prices. - Between the lines: When mortgage rates rise, that lowers the supply of homes hitting the market. Lower supply means higher prices, especially in areas where many buyers are bidding in cash.

The bottom line: Americans are holding onto their cars for much longer than they normally would because replacing them is so expensive. Something similar is beginning to happen in real estate, too. | | | | | | | | A message from Ripple | | Our commitment: carbon-neutral by 2030 | | |  | | | | Ripple, a company providing crypto solutions for business, is on track to be carbon net-zero by 2030. We're reducing emissions, increasing clean energy use, investing in high quality carbon removal projects and using a carbon-neutral blockchain. Learn more about a U.S.-based crypto innovator. | | | | | | 4. Get used to paying more |  | | | Illustration: Sarah Grillo/Axios | | | | Consumers need to brace for a new era of paying more across the board, Axios' Javier E. David writes. The big picture: This inflationary moment won't last forever. But the old days of cheap goods and services may be gone. What's next: Eventually, the energy spike will end. And some added costs, like Amazon's newly unveiled "surcharge" for online sellers, can be rolled back. - However, other prices can be notoriously "sticky" — which suggests economic activity is setting a new base at higher price levels.

Go deeper. | | | | |  | | | | If you like this newsletter, your friends may, too! Refer your friends and get free Axios swag when they sign up. | | | | | | | | 5. Tax frustrations |  | | | Illustration: Megan Robinson/Axios | | | | Not to get all technical here, but doing your taxes is a headache. This year, more than half of tax filers turned to a professional for help, Emily writes. Why it matters: Even low-wage earners shell out for tax prep, cutting into the refund money they rely on to make ends meet, a new survey finds. Even more galling — most of these folks qualify for free filing services. Driving the news: Today is the deadline to file your federal return, but if you cannot, you can file an extension. - There is a pot of gold waiting at the end of the anxiety rainbow. This year's average refund is $3,226.

By the numbers: Still, only one in five workers who qualify for free filing help use the service, according to a new survey of nearly 7,000 service sector workers conducted by the Shift Project. The ongoing survey is conducted by sociologists at Harvard and the University of California, San Francisco. - The median worker pays $100, equivalent to about six hours of work, to file their taxes each year. Some workers pay as much as $600 to file — a week's wages for someone earning $15 an hour.

- Many of these workers qualify for the Earned Income Tax Credit, a refund offered by the federal government responsible for keeping millions out of poverty.

That means folks are using money meant to raise their standard of living and paying it back to tax prep companies. - "Refunds are really important to this group of workers and filing for taxes, an important part of the process of being able to receive those refunds just really cuts into the benefit that the refund is giving," said Evelyn Bellew, a resident fellow at Shift.

Zoom out: Taxes don't need to be this complicated. Other countries have figured out systems that are relatively painless, as Axios' Neil Irwin explained nearly a decade ago. - If you're a wage earner who gets a weekly or biweekly check, the IRS already knows how much you made and how much was taken out of your check. They could just.. send you a refund if you overpaid, or a bill if you owe money. You could deal with it quickly. Imagine!

- Standing in the way — lobbying by companies that provide tax prep services, and some conservatives who believe making tax filing a headache helps fuel general anti-tax sentiment.

The bottom line: Don't expect any of this to change. But if you earn less than $73,000, check out your options. Good luck! | | | | | | | | A message from Ripple | | Carbon-neutral crypto is a reality right now | | |  | | | | Ripple uses the energy-efficient XRP Ledger — the first major global carbon-neutral blockchain — and its native cryptocurrency, XRP, to keep environmental impact low, with transactions that are much less energy-intensive than cash transactions. Learn more about a U.S.-based crypto innovator. | | |  | It's called Smart Brevity®. Over 200 orgs use it — in a tool called Axios HQ — to drive productivity with clearer workplace communications. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Suite 1300, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment