| | | | | | | Presented By J.P. Morgan Wealth Management | | | | Axios Markets | | By Dion Rabouin ·Apr 05, 2021 | | Good morning! Was this email forwarded to you? Sign up here. (Today's Smart Brevity count: 1,386 words, 5 minutes.) | | | | | | 1 big thing: How the Fed took control of the economy |  | | | Illustration: Sarah Grillo/Axios | | | | To brace the U.S. economy and stave off another Great Depression, the Federal Reserve has taken control of it through unprecedented intervention — manipulating market prices, controlling rates and propping up companies on a previously unimaginable scale. Why it matters: The U.S. is a market-run, capitalist economy. But the market is ostensibly now governed by an unelected and largely independent group of technocrats that directs it by creating ridiculous sums of money to buy assets. - Even with this control, the Fed has by its own admission failed to fully reach its goals — stable prices and maximum employment.

How it works: The Fed steadied the economy by setting interest rates near 0%, and buying so many bonds in the open market that it now boasts a $7.7 trillion balance sheet. - The hope is that companies will hire more workers, but that's no longer how the economy works, notes Columbia University professor and Nobel Prize-winning economist Joseph Stiglitz.

- Rather than hiring, companies buy back their stock and invest in technology designed to replace workers.

"We've been through a period where low-interest rates have not stimulated the economy very much and where disproportionately [companies' increased profits] go into automation, killing jobs, not creating jobs," Stiglitz tells Axios. - "At a zero interest rate the cost you focus on is the cost of labor, because that's your only cost. Whereas if the cost of capital goes up relative to the cost of labor you get a more balanced kind of innovation and investment."

Yes, but: Many argue the Fed was forced into this position and the extraordinary economic intervention is its attempt to make up for a new world of slowing growth, growing debt, an aging population and a dysfunctional Congress. What happened: To battle the coronavirus pandemic, the Fed announced on March 23, 2020, that it would buy an unlimited amount of U.S. government bonds and mortgage-backed securities; purchase corporate bonds, including debt with a "junk" credit rating; and even provide financing directly to individual companies. Take it to the street: "Why does the Fed have outsized influence on financial prices? Because it's shown itself willing to act," Vincent Reinhart, who spent 20 years as an economist at the Fed, tells Axios. "If something really bad happens, [Fed chair Jerome] Powell is stepping in." - "The lunchtime bully doesn't enforce order on the school playground by beating everybody up, they just have to beat one or two kids up," Reinhart, now chief economist at Mellon, adds.

The intrigue: Knowing that asset prices can fall only so far before the Fed will act encourages market participants to buy at any level. - It also has essentially destroyed the ability of the market to determine companies' value, Scott Minerd, CIO of Guggenheim Partners and an adviser to the New York Fed, told me in the midst of the crisis.

- "The definition of market prices is whatever the Fed says it will be."

|     | | | | | | Bonus content: The results |  Data: Ipsos; Chart: Axios Visuals The combination of low-interest rates and inflated asset prices discourages saving and encourages risk-taking, empowering a wave of speculative investments. - The effects can be seen in the rise of Bitcoin (hailed as a savings asset that the Fed can't manipulate), the frenzy in "meme stocks" like GameStop, and the rise of the stock market to record highs even as the economy had its largest contraction since 1946.

- The Fed's policies also allowed big companies to issue record amounts of debt at record low levels, keeping many of them in business and able to run essential functions.

- But that privilege also has extended to unprofitable "zombie" companies — those without enough revenue to pay off their current monthly debt obligations — and kept new and vibrant firms from disrupting inefficient ones.

Where it stands: The benefits of this extreme action are supposed to reach everyday Americans but are largely resulting in a bonanza for the wealthy (just under 90% of stocks are held by the top 10% of U.S. households and homeownership rates skew significantly toward older, wealthier white Americans) and large corporations. | | | | | | | | 2. State of public opinion |  Data: Ipsos; Chart: Axios Visuals Disjointed results for the wealthy and working classes since the pandemic hit the U.S. have fostered an environment in which most Americans don't trust the Federal Reserve, or think that the central bank is doing a good job. Driving the news: New polling from Ipsos exclusively for Axios shows that 53% of Americans say they don't trust the central bank, and just 38% say the Fed has done a "good" or "excellent" job, while 58% say the Fed is doing a "fair" or "poor" job. - The percentage of respondents who say the Fed is doing poorly (13%) is more than triple the share who say it's doing an excellent job (4%).

- Similarly, the share who say they have no trust at all in the Fed (15%) is triple the share who say they have a great deal of trust (5%).

Why it matters: Some market participants argue that most ordinary people have no idea what the Fed does, but 60% of poll respondents said they know at least "a little" about how the Fed operates, compared to 38% who say they know "not a lot" or "nothing." - The Fed gets its charter from Congress, which is at the mercy of voters. If voters think the Fed is hurting rather than helping, they can direct their representatives accordingly.

| | | | | | | | A message from J.P. Morgan Wealth Management | | Get an investment check-up with a J.P. Morgan Advisor | | |  | | | | Your J.P. Morgan Advisor: - Develops smarter, personalized wealth-building strategies that fit you and your goals.

- Meets with you regularly to help keep your portfolio on track.

- Keeps you up to date on important market changes and how they might impact your portfolio.

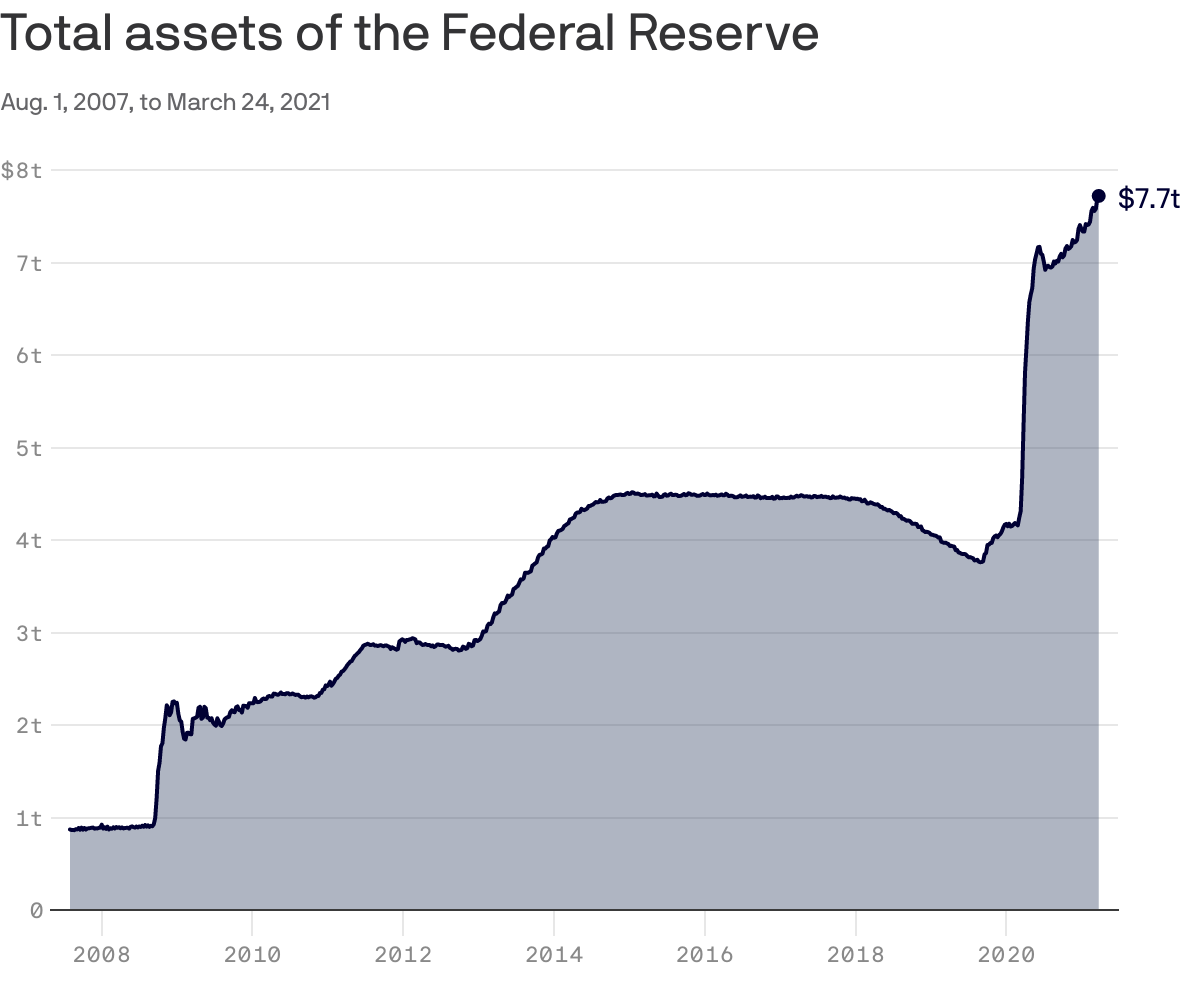

Learn more. | | | | | | 3. Why the Fed's balance sheet matters |  Data: Federal Reserve; Chart: Danielle Alberti/Axios Much has been made of the growth of the Fed's balance sheet from around $800 billion before the global financial crisis to over $7.7 trillion today. What it is: The Fed's balance sheet is the number of assets the Fed holds — akin to an investment portfolio held by the central bank. Be smart: The balance sheet has grown so large because even when the Fed brings its policy rate to 0% it can only control short-dated interest rates and it also wants to bring down long-dated interest rates like the 10-year Treasury yield that drives mortgages and other consumer borrowing costs. - Once the Fed has cut interest rates to 0%, "the balance sheet is how you push down further," says former Fed economist Claudia Sahm, a senior fellow at the Jain Family Institute.

Between the lines: The Fed uses its portfolio to influence the economy and its current $7.7 trillion total suggests it is doing a lot of influencing. - "Rigging the economy, that's what the Fed is there to do," says Julia Coronado, president of MacroPolicy Perspectives and a former Fed staffer.

- "Congress has given the Fed a job to do — it's supposed to rig the economy in a favorable way, reduce the amplitude of business cycles, reduce the severity of business cycles, and get us back to work as fast as possible."

How it works: By purchasing U.S. government bonds and mortgage-backed securities (and as of 2020 even corporate bonds from companies like Apple), the Fed increases their price and reduces their yield. - And since borrowing costs for things like mortgages and auto loans (and markets utilized by Wall Street banks and hedge funds) are based on the yield of U.S. government debt, the Fed's purchases make it cheaper to borrow money, encouraging more individuals and institutions to do so.

- The government finances its debt by issuing bonds for things it can't pay for with tax revenue, so the Fed's balance sheet makes that debt cheaper as well.

The bottom line: The Fed "is more and more active and more and more responsible for the management of not just the Treasury market, but the entire economy," says Quincy Krosby, chief market strategist at Prudential Financial. - "This is the question: Once a central bank goes down this road, at what point can they extricate themselves?"

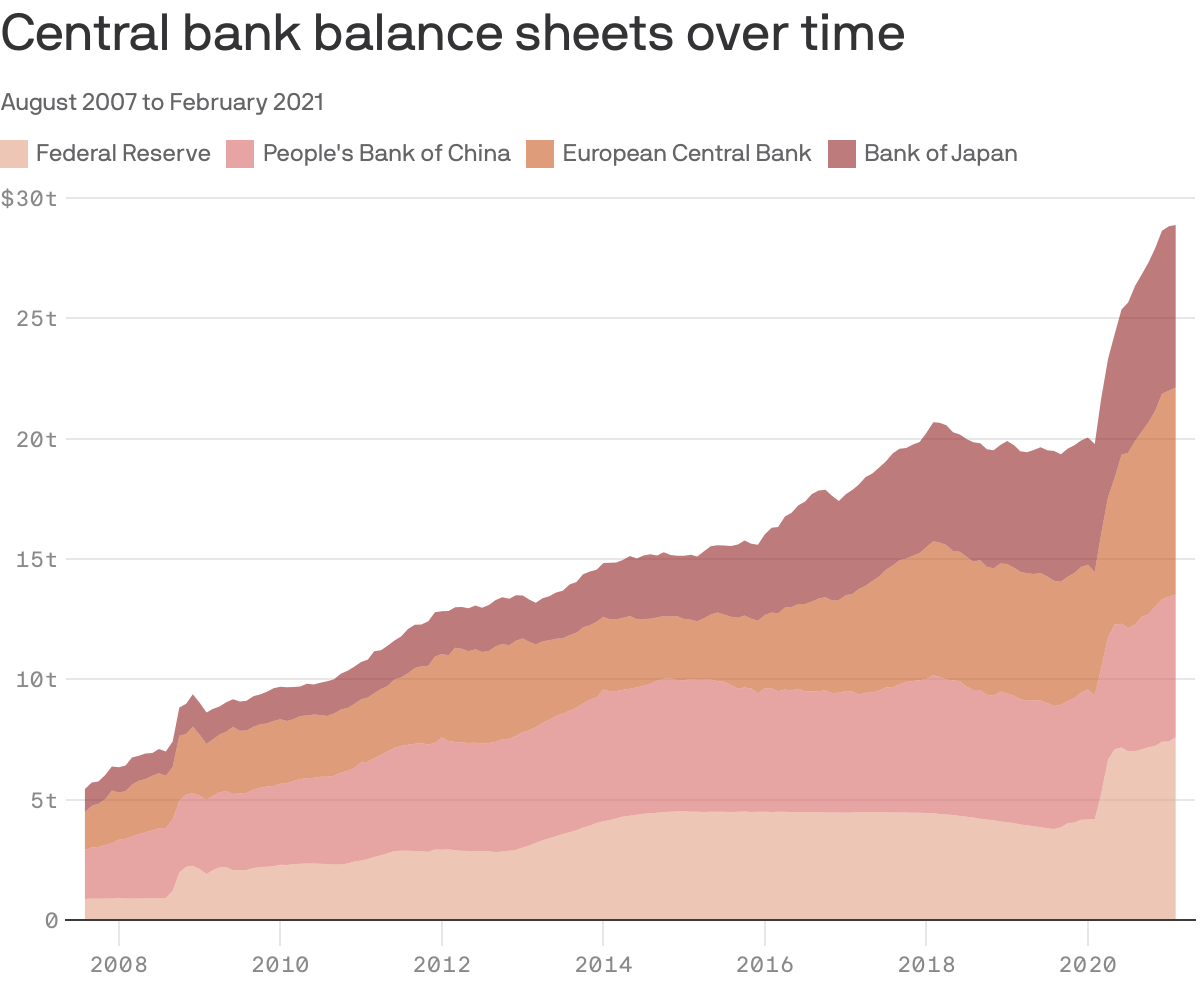

| | | | | | | | 4. The global perspective |  Data: Yardeni Research. Chart: Danielle Alberti/Axios The Fed has not been alone in its actions. Central banks around the world have been printing money out of thin air and using it to purchase assets in order to stimulate their respective economies. - Just the world's four largest central banks had accumulated $28.8 trillion of assets as of February, according to data collected by Yardeni Research.

What's next: "For central banks, I don't think there is any alternative to what they've been doing until now, namely vastly significantly support the economy," former European Central Bank president Mario Draghi told Axios in December. - "Support, in my view, will continue for quite a long time."

| | | | | | | | A message from J.P. Morgan Wealth Management | | Level up your investing strategy | | |  | | | | Tap into 200 years of expertise and make smarter investing decisions when you partner with J.P. Morgan Wealth Management. Here's how: When you trade commission-free on the Chase Mobile app, you get access to timely investment research and insights, and a support team of real people. Learn more. | | | | Thanks for reading! This newsletter is written in Smart Brevity®. Learn how your team can communicate in the same smart, clear style with Axios HQ. | | | | Axios thanks our partners for supporting our newsletters.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Suite 1300, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment