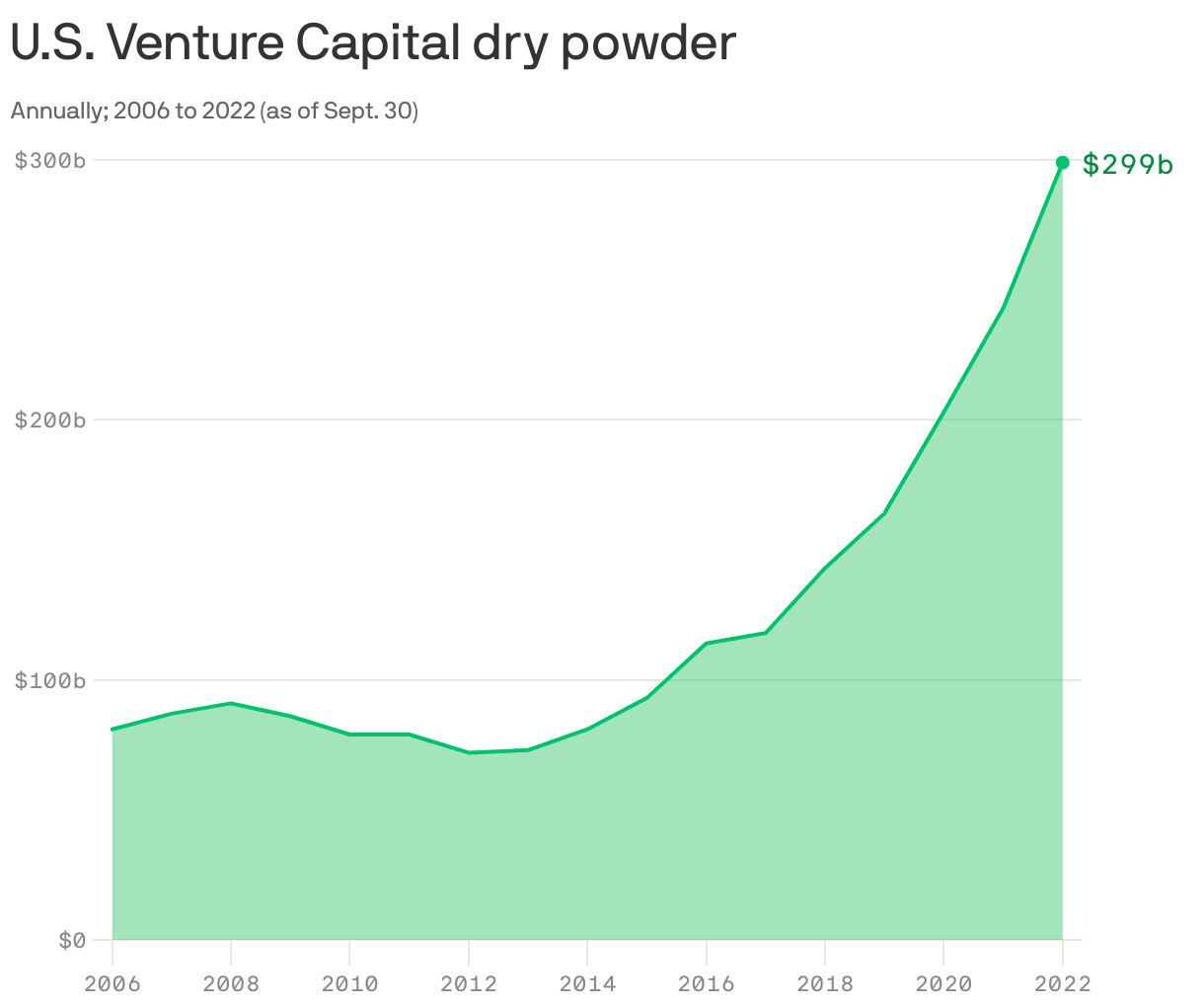

| Last year was a record year for venture capital fundraising, but some investors are warning that big "dry powder" figures are an illusion, and won't translate into much startup investment in a year that's already off to a rocky start. Why it matters: Whether VCs are willing to back companies in 2023 could spell life or death for certain cash-hungry startups. The big picture: In 2022, VCs raised a grand total of $162.6 billion across 769 funds in fresh capital, per PitchBook's latest data. That followed 2021's own venture fundraising record of $154.1 billion. - As of Sept. 30, 2022, there was about $298.5 billion of dry powder, per PitchBook.

What they're saying: "Everyone keeps talking about how VCs have so much 'Dry Powder' to invest. It's all B.S.," Octane AI co-founder Ben Parr recently said on Twitter. Yes, but: There's nuance. For one, not all limited partners (LPs) are created equal. While some high-net-worth individuals' might be strapped for cash right now, things are different for large institutions. - They model their portfolios and assets for a number of possible scenarios and are usually prepared to have the necessary liquidity to honor commitments.

- But the cash crunch does show up in one area — whether they make commitments to new funds. While some LPs are doubling down on venture and increasing their allocations to the asset class, many now feel overextended after the pandemic era saw VCs raise new funds faster than before.

Moreover: VCs do have to deploy the capital they raised — it is their job to do so. - But it won't be at the speed and volume seen during the heady days of 2021, which may make it feel like the market isn't moving. And as many point out, downturns also usually drive out the tourists, adding to the feeling that all the investors have packed their checkbooks away.

- In fact, even amid last year's pullback from VCs and some startups delaying fundraising, investors poured $238.3 billion across nearly 16,000 deals in the U.S. That's more venture investing than any over a decade at least, with the exception of 2021.

Vibe check: "I haven't heard anywhere near the LP bellyaching that I heard during the financial crisis," Ahoy Capital's Chris Douvos, whose firm invests in early-stage venture funds, tells Axios. - "There aren't mass calls for people to shrink fund size like there was in 2008," he adds. "I think what people want is for pacing to return down to normal down from the hyperactive of 2020 and 2021."

- He also points out that for VCs, "the deployment of capital is a gating to the raising their next fund."

The bottom line: 2021 remains an outlier in nearly every possible way. |

No comments:

Post a Comment