| | | | | | | Presented By Fidelity | | | | Axios Markets | | By Felix Salmon · Aug 27, 2022 | | It's the last Markets Weekend of August; next week we'll have a special Labor Day edition asking where all the workers went. - This week is debt-focused. Would you borrow money to give to charity? A new company is betting that you will. I also look at the big picture of the student loan situation. The whole thing is 1,489 words, a 5.5-minute read.

| | | | | | 1 big thing: When politicians grab the purse-strings |  | | | Illustration: Brendan Lynch/Axios | | | | The decision to nationalize an entire industry is one that you'll very rarely see a U.S. politician make. But the U.S. did it in 2010, with student lending. From that year onward, rather than the federal government guaranteeing loans from private lenders, it just made the loans directly itself. Why it matters: The outcome says a lot about the pros and cons of nationalization. - The federal government rapidly discovered that it wouldn't operate like the for-profit lenders. Private lenders had a higher cost of funds than the government, and also had much less sympathy for borrowers.

- Putting politicians in charge of the government's student loan portfolio effectively flipped the normal dynamic between borrower and lender. It was a bit as if people with bank loans were able to elect their local bank manager, who could in turn forgive those loans.

The upshot: A federal lending program that was sold as generating $113 billion of income for the federal government is now likely to end up costing the government well over $500 billion. - By the numbers: A July 2022 GAO report put the costs to the government, as of April 2022, at $197 billion, with the COVID-era payment moratorium accounting for $102 billion of that.

- On top of that needs to be added a further 8 months of debt moratorium, at about $3.5 billion per month, plus at least $300 billion (and possibly much more) for the long-term costs of this week's debt forgiveness package.

The downside: That's at least $640 billion less than the amount of money the government was initially expected to make. - The upside: Thanks to the 2010 nationalization of student loans, the federal government, under Obama, Trump, and Biden, was able to implement policies it could never have imposed on private lenders. Those policies, in turn, had massive positive effects.

How it works: The federal student loan program cares more about fairness than profit. So all loans carry the same interest rate, and payments are capped as a percentage of income. - The flat rate means that high-income borrowers tend to refinance into lower-rate private loans, while lower-income borrowers find the government loans relatively attractive. As a result, the percentage of borrowers on income-driven repayment plans rose from 20% in 2013 to 47% in 2022. Expect it to rise even further after this week.

The big picture: When governments privatize industries, one of the main reasons cited is to take pricing decisions out of the hands of politicians. They feel unable to raise prices themselves, so they sell off the franchise to someone who can. - Nationalization is the same process but in reverse: It allows politicians to make pricing decisions, for better or for worse. Generally those decisions are bad for the public fisc, but that doesn't mean they're bad as a matter of public policy.

Between the lines: One look at your broadband bill should suffice to persuade you that running utilities as private-sector monopolies isn't always good public policy. - Even opponents of federal student-loan debt relief tend to stop short of waxing nostalgic about the years (roughly 2004 to 2009) when Sallie Mae was a private sector company.

The bottom line: National ownership does tend to mean cheaper prices — for better or worse. |     | | | | | | 2. Tuition inflation isn't as bad as you think |  Note: Net cost of attendance is published cost of attendance minus grant aid. Data: CollegeBoard; Chart: Erin Davis/Axios Visuals Here's something you might think you know: That the cost of going to college has been rising a lot faster than inflation for many years. You might even have a long list of reasons why it's been rising, like Baumol's cost disease, or administrative bloat, or expensive sports teams and climbing walls. - In fact, college costs haven't been rising in real terms. For private four-year colleges, they've actually been falling.

Why it matters: President Biden's decision to forgive billions of dollars in student debt has inevitably raised the specter of college cost inflation. Now that this precedent has been set, there has been a worry (or concern trolling) that colleges will feel free to hike their tuition costs, on the grounds that anybody taking out loans to pay that tuition will ultimately get a significant chunk of their debt forgiven anyway. The big picture: The amount that Americans pay for college tuition is ultimately set according to the rules of supply and demand. Right now, thanks to overbuilding, a falling birth rate, and a decline in foreign students, there's significantly more supply than there is demand — and that means flat or declining prices. - Total freshman enrollment in 2021 was 2,116,631 students, per the National Student Clearinghouse. That's down almost 20% from the 2,592,703 freshmen who enrolled in 2015.

Between the lines: Don't look at soaring official tuition costs to work out how much people are paying. Instead, look at the amount they actually pay, which is invariably lower. Colleges have worked out that a high tuition fee combined with a high "merit scholarship" is more attractive than a lower tuition fee, so now almost everybody gets some form of financial aid. By the numbers: Over the past 8 years, the published tuition fee for a four-year private college, in constant 2021 dollars, rose 9.4%, to $38,070, per the College Board. If you include room and board, the increase was the same — 9.4% — but the total was $51,690. - If you look at how much students actually pay, however, after accounting for grant aid and other discounts, the total fell slightly to $32,720, with room and board included. That's the lowest number since the 2012–13 school year.

The bottom line: Most private colleges — with a few high-profile exceptions — charge as much as they can, with or without the promise of possible future debt forgiveness. For the past decade, competition between colleges has kept prices from spiking. Even a rational expectation of future debt relief shouldn't fundamentally change that dynamic. - Go deeper: Axios' Dan Primack writes about why college costs are still objectively too high, and what might bring them down meaningfully.

| | | | | | | | 3. Borrowing to give |  | | | Illustration: Aïda Amer/Axios | | | | Donating money to charity is good and worthy. But should nonprofits encourage you to go into debt in order to do so? A new VC-funded company, BGenerous, says the answer is yes. Why it matters: Hundreds of thousands of charities around the country rely on small-dollar donations from a broad range of individuals. As those donations move from physical checks to online pledges, BGenerous has decided to apply the buy-now-pay-later playbook to them. They call it "donate now, pay later." How it works: When you use BGenerous to make a donation, you pay no money up front. Instead Drake Bank lends you the money, which gets paid directly to the charity. You then pay the bank back in installments, interest-free, over 3 to 9 months. - Drake Bank and BGenerous split a commission of between 10% and 15% of the total donated, paid by the charity (or by the donor, if they're feeling extra-generous).

The upside: BGenerous CEO Dominic Kalms tells Axios that when given the opportunity to pay over time, 82% of donors double their donation — with that number rising to 89% among donors giving $1,000 or more. - The downside: The model is "uncomfortably nearing the space of payday lending," says Stanford philanthropologist Rob Reich.

Between the lines: The BGenerous product is an iron-clad commitment device. Many people want to give more in the future; this is a way of your present self binding your future self to doing so. - The "give more tomorrow" strategy is very powerful; this just gives it teeth, and brings it in line with buy-now-pay-later products with which many modern consumers are already very comfortable.

Be smart: Inflation has cut sharply into disposable income, says Michael Gorriarán, the president of Arjuna Solutions, another company selling AI-based services that attempt to maximize the amount that donors give. - Charities need all the tools at their disposal if they're to maintain their small-dollar income stream.

The big picture: Charitable fundraising isn't cheap — it generally costs the nonprofit around 25% of the amount donated. - Paying 12% to BGenerous is "not terrible," says Caroline Fiennes, the director of charity evaluator Giving Evidence, when compared to the cost of raising money from foundations. That works out to at least 17% for smaller charities.

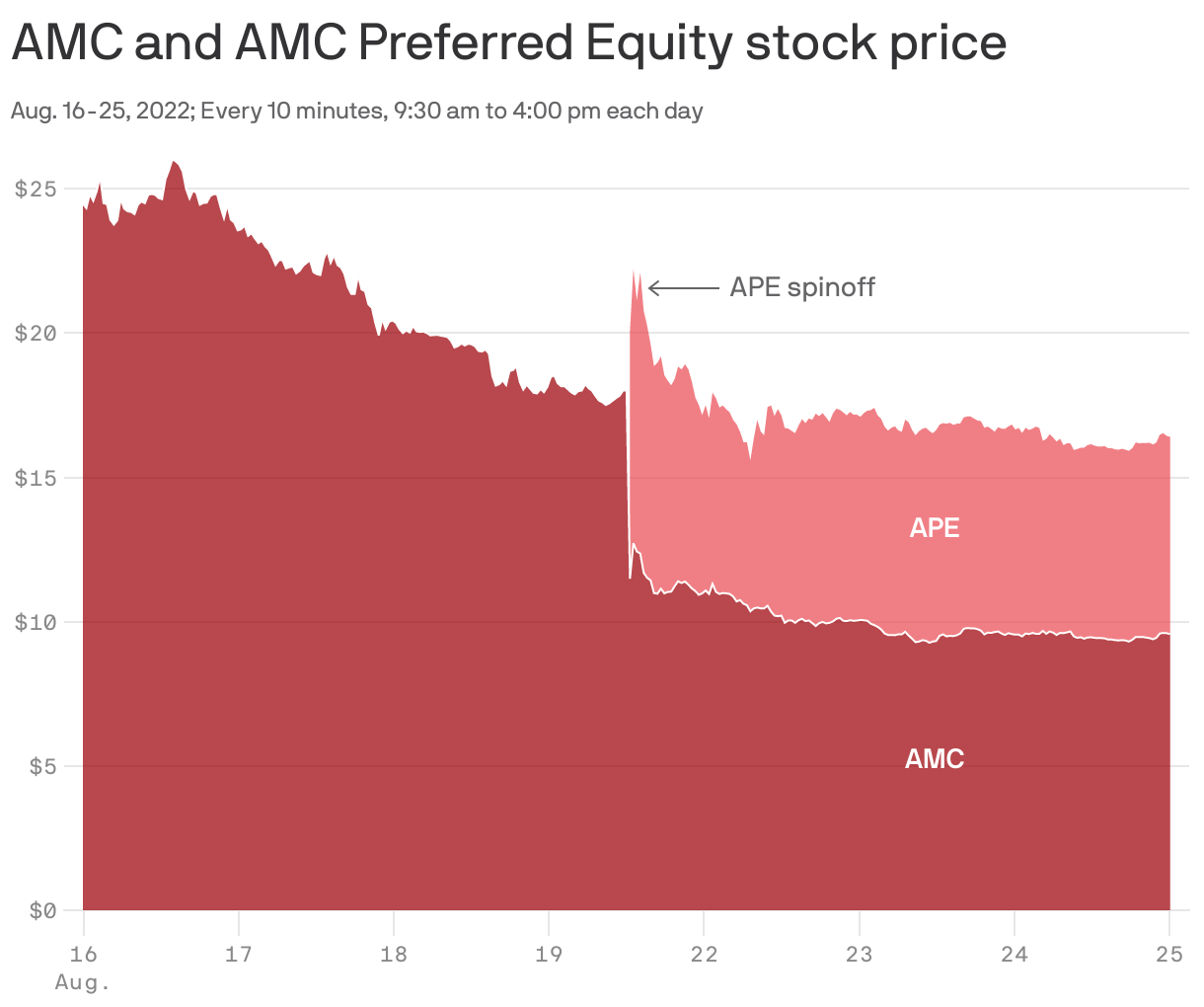

The bottom line: Charitable fundraising has never been particularly sophisticated, either technologically or financially. Maybe that's now changing. | | | | | | | | A message from Fidelity | | You want to move past IPO — Fidelity helps get you there | | |  | | | | Fidelity Stock Plan Services can provide equity compensation and management solutions that keep your momentum going — to and through life as a public company. Why it's important: Together, you can create equity comp solutions that work throughout your company's journey. | | | | | | 4. The AMC stock split |  Data: FactSet; Chart: Axios Visuals Movie-theater chain AMC, in full meme-stock mode, split its stock this week. What used to be 1 share of AMC is now 1 share of AMC plus 1 share of APE, a brand-new security, with a brand-new ticker, that is economically identical to AMC stock. - The two securities trade at weirdly different prices, for reasons that Bloomberg's Matt Levine discussed three times this week, but the combination seems to be trading at pretty much where the old AMC stock would be.

- The upside, for AMC, is that it can raise money by selling new APE shares; it's run out of AMC shares to issue and can't work out how to get permission to issue more.

| | | | | | | | A message from Fidelity | | You prep for your IPO — Fidelity has your back at every step | | |  | | | | Fidelity Stock Plan Services can provide equity compensation and management solutions that keep your momentum going — to and through life as a public company. Why it's important: Together, you can create equity comp solutions that work throughout your company's journey. | | | | Finally, if you fancy buying me a thank-you gift for writing this newsletter, Paul Allen's art collection is coming up at auction this November, and is expected to sell for more than $1 billion. Just saying. |  | | Why stop here? Let's go Pro. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment