| | | | | | | Presented By Capital One | | | | Axios AM Deep Dive: | | Hard Truths | | By Mike Allen ·Dec 19, 2020 | | View in browser | | Good afternoon and welcome to the third edition of our Hard Truths Deep Dive series. - As we hunker down in our homes for the holidays, our focus is on race and housing, led by Aja Whitaker-Moore and Michele Salcedo.

💻 Join Axios on Tuesday at 12:30 p.m. ET for our third Hard Truths event, a discussion on housing. Register here. - 🎧 Listen to a special edition of our "Axios Today" podcast, examining three generations of Black homeownership on Chicago's South Side.

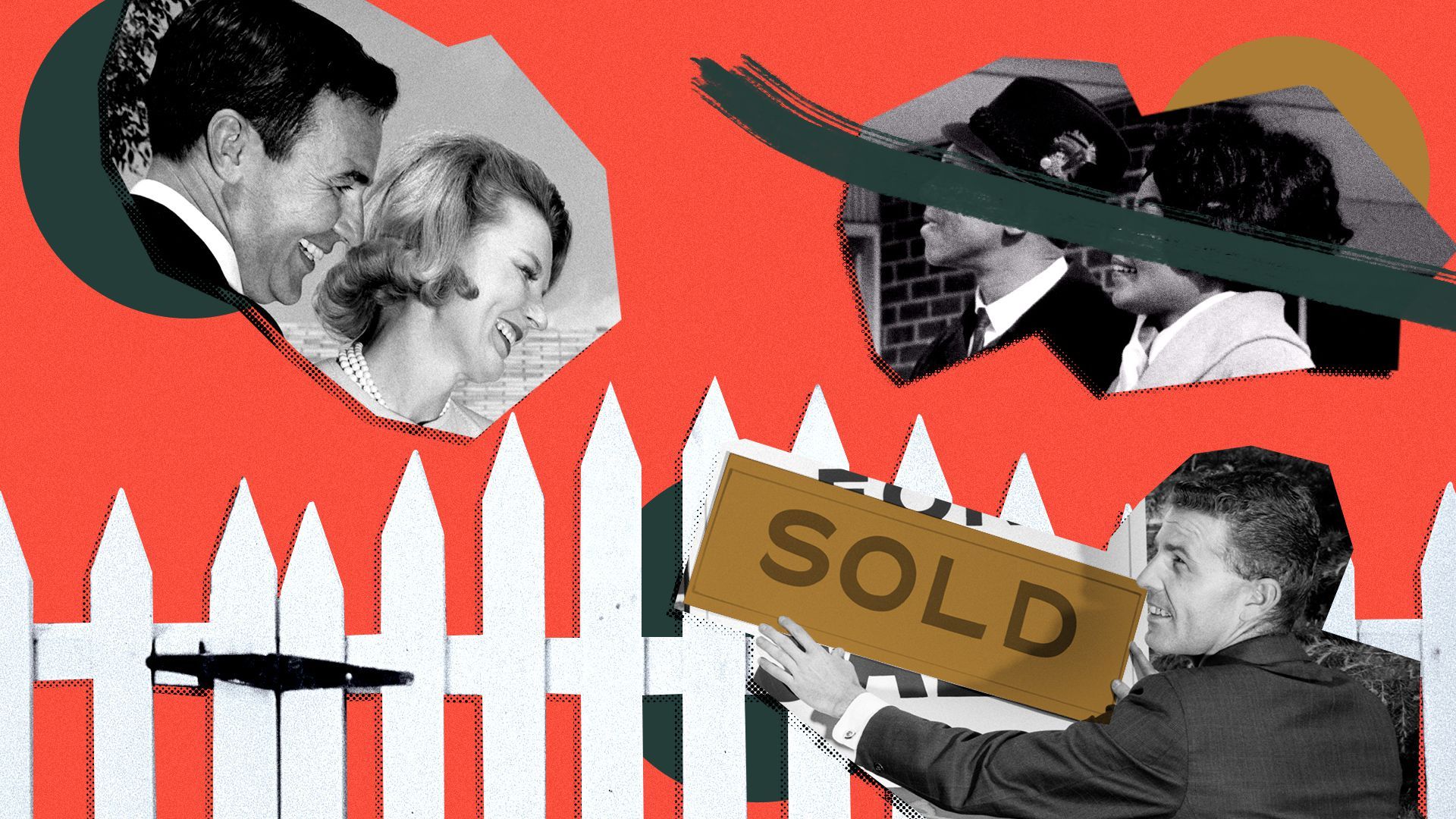

Today's Smart Brevity™ count: 1,491 words ... 5½ minutes. | | | | | | 1 big thing: American Dream deferred |  | | | Photo illustration: Aïda Amer/Axios. Photos: Lambert Studios/ARC), H. Armstrong Roberts/ClassicStock via Getty Images | | | | The U.S. government partnered with the private sector for decades to prevent Black Americans and immigrants from owning homes, Axios' managing editor for business, Aja Whitaker-Moore writes. - While explicit rules regulating where people of color live were outlawed in 1968, the legacy of racial segregation in undervalued neighborhoods still reverberates throughout the country.

Why it matters: Owning a home is an integral piece of the American dream and the single most important driver of wealth generation and financial security — especially for Black households. The catch: Federal and state governments created policies to maintain and intensify segregation. The business community supported that discrimination by using racial criteria to make decisions about lending, property valuation and rental rates. "It was the continuation of the assumption that policymakers had about white superiority, African American inferiority, and the desire to keep the two apart." — Richard Rothstein, Distinguished Fellow of the Economic Policy Institute How it worked: - Racial covenants: Starting in the 1920s, realtors and developers wrote language into deeds to prevent anyone who wasn't white from buying property.

- Redlining: The federal Home Owners' Loan Corp. created "residential security maps" in the 1930s based on evaluations from lenders, developers and appraisers. The lowest-rated, "hazardous" areas were outlined in red. The maps reinforced racial and income segregation, deterred investment in non-white communities and depressed home values.

- Real-estate agents: The profession required racial discrimination. The National Association of Realtors recently issued a public apology for its past.

"A Realtor should never be instrumental in introducing into a neighborhood a character of property or occupancy, members of any race or nationality, or any individuals whose presence will clearly be detrimental to property values in that neighborhood." The big picture: Redlined maps are gone, but the inequality they helped create has endured. Limiting the ability to build wealth through the value of a home touches future generations since houses can be passed on as inheritance, and also tapped for anything from college funds to seed money to start a business. "Redlining is still hardcoded in our cities, and that manifests itself in what home values are doing now," says Cheryl Young, senior economist at Zillow. - Non-white Americans have a harder time than white homebuyers finding homes and financing them at affordable rates using traditional mortgages.

- Being blocked from homeownership means more people of color rent and pay much more for the privilege. Higher rents equate to lower savings cushions and more exposure to eviction.

The intrigue: If you think federal policies have improved life for people of color, the reality is very different for Native Americans. - Thunder Valley Community Development Corp. executive director Tatewin Means says few Native Americans feel the federal government will solve the housing crisis soon. "We keep expecting a broken system to work," Means tells Axios' Russell Contreras.

The bottom line: "Because housing was such a driver of intergenerational wealth in the 20th century, it is hard to say that anything else measures up to driving and worsening wealth disparity between people of color and white families in the last century," says Robert Nelson, a historian focused on housing and urban history at the University of Richmond. - "It is one of the main expressions of white privilege and systemic racism."

Go deeper. |     | | | | | | 2. Timeline of housing disparities |  | | | Photo Illustration: Eniola Odetunde/Axios. Photos: Buyenlarge, Bettmann, Newsday via Getty Images | | |  Graphic: Eniola Odetunde, Danielle Alberti/Axios. Photos: Tim Graham, Travis Heying, Hearst Newspapers, Newsday, Bettmann, George Rinhart via Getty Images | | | | | | | | 3. Why racial homeownership gap persists |  | | | Photo illustration: Sarah Grillo/Axios. Photos: H. Armstrong Roberts/Classicstock, Cliff de Bear/Newsday via Getty Images | | | | The homeownership gap between Black and white Americans is worse today than when race-based housing laws and policies were in effect decades ago, Axios' Felix Salmon reports. Why it matters: Unequal access to mortgage financing has had a predictable effect: Non-white Americans have much lower homeownership rates, lower wealth and a higher degree of financial precarity, especially Black Americans.  Data: Zillow; Chart: Andrew Witherspoon/Axios Non-white Americans face a harder time finding and financing a home. They also pay higher rates once they get a loan. And they are more likely to be targets of predatory lending. - Today, Black families are denied mortgages at a much higher rate than other Americans. According to Zillow, some 24% of mortgage applications by Black Americans are denied, compared to nearly 20% for Hispanics and 14% for Asians and for whites.

- Black-owned banks have tried to fill the gap, supporting borrowers in predominantly Black communities. But their numbers have shrunk by 50% since 2001, according to the Urban Institute.

The big picture: When loan officers extended mortgages, they often withheld loans from people of color. In recent years, those decisions are increasingly made by algorithms, based on credit scores. But that's not necessarily an improvement, since Americans of color have lower credit scores, on average. - Non-white households are more likely to be renters — and timely rent payments, unlike timely mortgage payments, are not reflected in credit scores.

The bottom line: Racism can still be found at every stage of the homeownership financing process. As America approaches a new eviction crisis, the racial housing gap looks as though it's going to get even worse. Go deeper. | | | | | | | | A message from Capital One | | Our commitment to growth in underserved communities | | |  | | | | The Capital One Impact Initiative is supporting socioeconomic mobility through a $200 million, five-year commitment to closing gaps in equity and opportunity. Read about our focus on creating a world where everyone has an equal opportunity to prosper. | | | | | | 4. The rental market's "Black tax" |  | | | Photo illustration: Sarah Grillo/Axios. Photo: Underwood Archives/Getty Images | | | | Renters of color, especially Black Americans, often pay a "Black tax" — a premium for renting similar housing in the same neighborhoods as whites, Axios' Courtenay Brown, Kia Kokalitcheva and Orion Rummler write. - Why it matters: A recent study found that Black tenants paid as much as 2% more in rent — a gap that widened in areas where more white people lived.

By the numbers: Locked out of homeownership, people of color overwhelmingly rent. - More than half of Black American and Latino households are renters, according to USAFacts, while Asian and Native American renters fall just under that threshold.

- Compare that to the 27% of white households that rent.

How it's playing: People of color already put more of their income toward housing compared to white people. - They're more likely to have fallen behind on rent during the pandemic because minority renters overwhelmingly work in sectors that shed jobs because of COVID-19.

- Households of color make up just under half of all renters but are projected to account for 58% of the households that will owe back rent by the end of the year, according to the Philadelphia Federal Reserve.

- The outsized burden comes due on Dec. 31, when the CDC's halt on evictions expires.

Discrimination against vouchers, which help low-income families, the elderly and the disabled access housing in the private market, also disproportionately affects people of color. - In 2018, over 90% of D.C. voucher holders were Black, despite making up only 48% of the city's residents, according to the Equal Rights Center.

- 15% of all Black renter households in D.C. used vouchers, compared to less than 1% of white renter households.

- In New York, landlords often stood up interested tenants of color when they said they were using housing vouchers, The City reported last year. A similar phenomenon played out in Boston and in many other cities.

What to watch: Pandemic-induced evictions could exacerbate the already high levels of homelessness among Blacks and Latinos especially. - Latinos make up roughly 18% of the U.S. population, but they represent 22% of all people experiencing homelessness, per HUD's 2019 annual report to Congress.

- Among Black Americans, the figure jumps to 40%, although they comprise around 14% of the country's population.

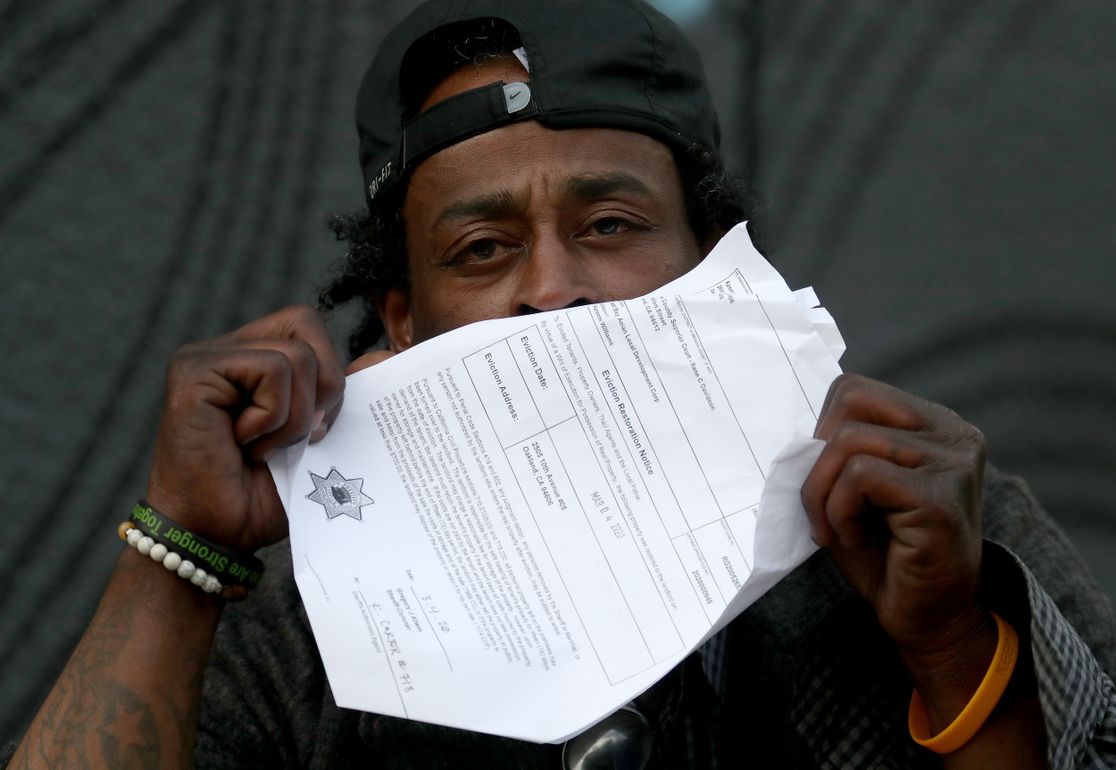

The bottom line: Higher rents, a diminished paycheck and the pandemic have renters of color on a downward spiral that affects other areas of their lives. Go deeper. | | | | | | | | 5. Bonus images: Struggling to pay the rent |  | | | Photo: Eric Baradat/AFP via Getty Images | | | | Above: COVID job cuts have left many renters of color without rent money. These banners are on a controlled-rent building in Washington. Below: An Oakland man holds the eviction notice that left his son and him homeless. Photo: Jane Tyska/East Bay Times via Getty Images | | | | | | | | 6. Reckoning on housing for Native Americans |  Data: Census Bureau. Chart: Andrew Witherspoon/Axios It's taken the coronavirus pandemic to highlight the dismal housing that many Native Americans and Alaska Natives are forced to call home: dilapidated, overcrowded structures without electricity or indoor plumbing, Axios' Russell Contreras reports. Why it matters: Native Americans on reservations have lived for decades under these dire conditions. The difficulty in building or even improving homes is traced to federal policies on reservation land and limited access to capital for Indigenous families. By the numbers: 40% of reservation housing is substandard and nearly one-third of reservation homes are overcrowded, according to the National Congress of American Indians — conditions that have turned private homes into superspreaders of COVID-19. - Some homes on the Oglala Lakota Nation, for example, have 21 people living under one roof, Thunder Valley Community Development Corp. executive director Tatewin Means told Axios.

- Less than half the homes on reservations are connected to public sewer systems, and 16% lack indoor plumbing, making frequent handwashing more difficult. Now, more than 10% of the 173,000 people of the Navajo Nation, for example, have tested positive for the virus.

- Around half the homes lack phone service.

Between the lines: Experts say there's little hope of improvement as long as Native American housing and property ownership sit in a maze of federal bureaucracies and underfunded projects. - Tribal members in need of housing on reservations face long waitlists. Off tribal lands, they face the same obstacles to getting a mortgage as Black and Latino Americans.

- The lack of housing forces some tribal members into homelessness in urban areas like Seattle, Phoenix, and Albuquerque, New Mexico.

Go deeper. | | | | | | | | A message from Capital One | | Fighting homelessness one run at a time | | |  | | | | Back on My Feet is combating homelessness through the power of running and community support. Capital One is partnering with Back on My Feet to teach its associates how to establish personal financial necessities like balancing a budget and making a plan for financial independence. Learn more. | | | | | | Axios thanks our partners for supporting our newsletters.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Suite 1300, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

Post a Comment

0Comments