| | | | | | | Presented By Blackstone | | | | Axios Markets | | By Felix Salmon · Nov 05, 2022 | | I'll be going to Art Basel Miami Beach this year for the first time in many years. Let me know if you have something fun going on, just so long as it doesn't have a "VIP list." - In this week's newsletter, I look at the effect of AI and blockchain on the art world, as well as financial inclusion and optimal currency areas. The whole thing is 1,531 words, a 6-minute read.

| | | | | | 1 big thing: Art-ificial intelligence |  | | | Illustration: Sarah Grillo/Axios | | | | Artists often use cutting-edge technology to create their work, but technology tends to change the art world only slowly and infrequently. Right now could be one of those times. Why it matters: AI technology has created a serious debate in the art world around issues of authorship and ownership — a debate that feels much more consequential than, say, arguments over monkey copyright. Driving the news: In San Francisco, an art show curated by a venture capital firm — in partnership with an AI company valued at $20 billion — is making the case for AI-generated art as "legitimate work" by serious artists. - Meanwhile, in New York, the highly-respected Perrotin gallery is showing the work of MSCHF, a venture-backed for-profit limited liability Delaware company that makes money by generating a seemingly endless stream of middlebrow hipster conceptualism.

- The group's first gallery show includes AI-generated pictures of feet that don't exist, which are then painted onto canvas by "factory labor."

Between the lines: Both shows seem to be predicated on the assumption that there's something transgressive about exhibiting AI art. - On the face of it, that's odd, given that the history of market-ratified AI-generated art dates back at least as far as 2018, when not only did I buy some AI-generated art myself, but an AI-generated portrait sold at Christie's for $432,500 to what MSCHF describes as an "overly credible" buyer. (I think they mean credulous.)

- And in the world of NFTs, there's no end of AI-generated projects, with no one raising so much as an eyebrow.

The intrigue: What changed is the arrival of a new generation of AIs, like Dall-E 2, Stable Diffusion, and DreamBooth. These AIs can output images indistinguishable from those of professional illustrators — just because they have learned to copy the work of those humans. - Artists have always learned from other artists. But when a machine is trained on the corpus of a single artist, that raises gnarly questions of authorship and copyright.

- Ogbogu Kalu, for instance, a Nigerian engineer in Canada, has created AI models trained to emulate the comic-book style of Holly Mengert and James Daly III — without the permission of either illustrator.

- As Mengert points out to Andy Baio, she couldn't give Kalu permission to train his model on her work even if she wanted to, because so much of what she does involves characters owned by corporations like Disney or Penguin Random House.

The bottom line: Art is getting dumber (see: Beeple, KAWS, TikTok, etc) just as AIs are getting smarter. Right around now, we're reaching the point at which the lines are beginning to cross. |     | | | | | | 2. The dream of resale royalties |  | | | Illustration: Eniola Odetunde/Axios | | | | One longstanding dream of artists is that they might somehow be able to share in the future appreciation of their art, even after it has been sold. Once again, technologists have a solution to sell them. Why it matters: One of the great promises of NFTs was that they could incorporate resale royalties into the art itself. Recently, however, that dream has started to fall apart. - In the real-world art world, however, where resale royalties barely exist, the dream is still alive.

Driving the news: NFT marketplaces like Magic Eden, Sudoswap, x2y2, and LooksRare are competing to attract buyers by removing the requirement to pay royalties to creators; even the creators themselves are beginning to remove royalties. - Arcual, however, a new company backed by the parent company of Art Basel, this week joined Fairchain in trying to bring blockchain technology to the high-end art market — and to bring resale royalties along with it.

The big picture: There's very little evidence that collectors and galleries would like to move to a world of resale royalties, or would not seek to circumvent them in much the same way as has happened with NFTs. - That said, the Arcual smart contracts are linked to real-world sales contracts, written under Swiss law — which means, contra NFTs, that if collectors try to avoid the resale royalties, they would be in violation of a legally enforceable contract.

The bottom line: If collectors actually supported resale royalties, they would have implemented them by now. And without collectors' support, it's hard to see the idea catching on. - Proponents of royalties should remember the golden rule: She who has the gold, makes the rules.

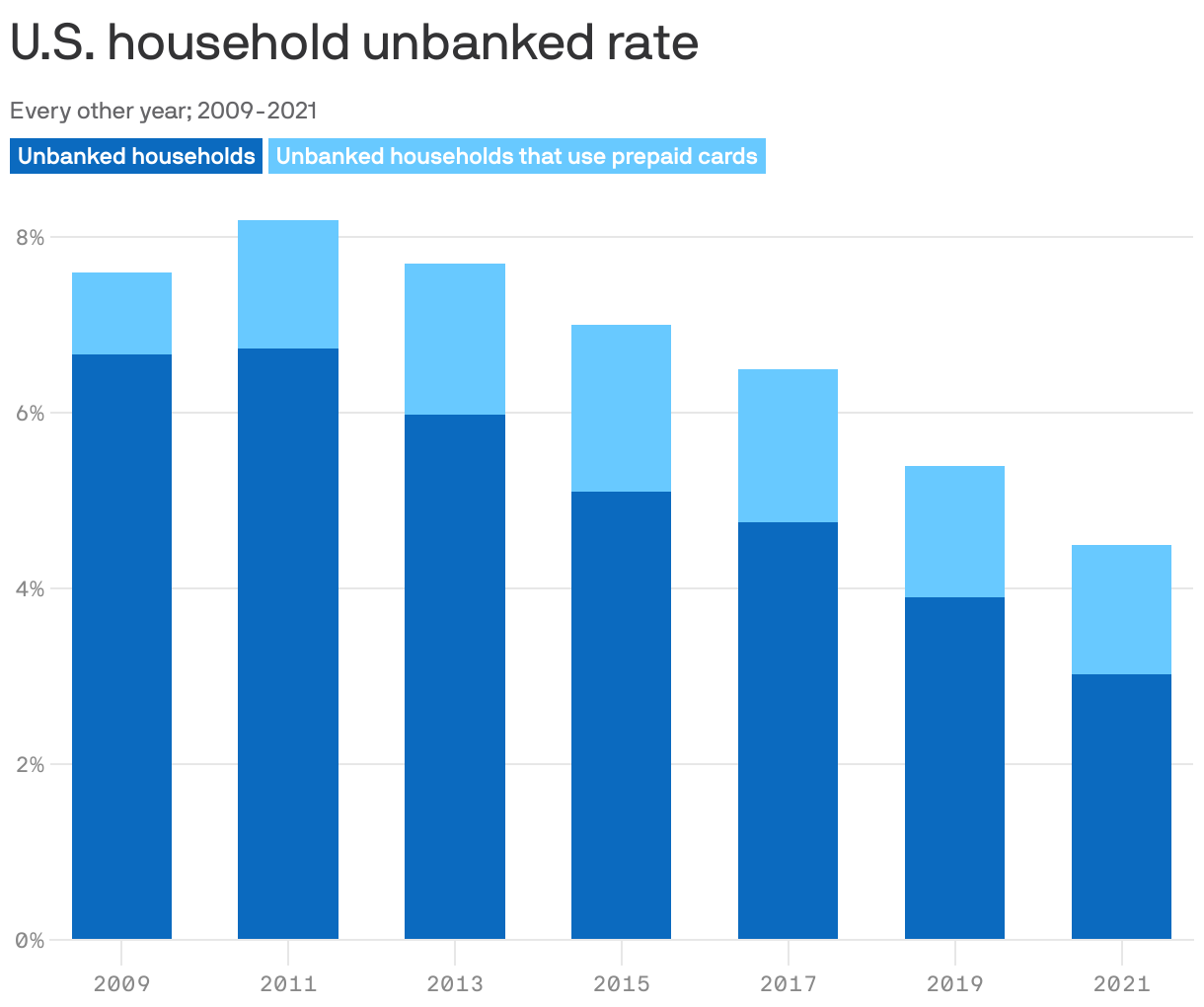

| | | | | | | | 3. A win for financial inclusion |  Data: Federal Deposit Insurance Corporation; Note: Prepaid card usage is defined by any all-time usage from 2009-2011, any usage in the past 12 months from 2013-2019 and current usage in 2021; Chart: Madison Dong/Axios Visuals The fiscal stimulus unleashed on America in the wake of the pandemic had one interesting side effect: It significantly decreased the number of U.S. households without bank accounts. Why it matters: Broadly speaking, the pandemic was good for economic inclusion. It seems to have significantly increased homeownership among Black, Asian, and Latino Americans; it also significantly decreased the number of households outside the banking system entirely. The big picture: The FDIC measures the proportion of U.S. households that are unbanked every two years — but defines unbanked as not having a checking or savings account at a bank or credit union. - Practically speaking, however, general purpose reloadable prepaid debit cards have become de facto checking accounts. Anything you can do with a basic checking account you can normally do with one of these cards — and most of the time your funds are FDIC insured.

- If you consider households with such cards to be banked, then only 3% of U.S. households are now unbanked — down 23% from 2019, and down 55% from 2011.

- That number falls even further if you subtract the people who have accounts at Venmo, Cash App, or other non-card-based digital depository institutions.

Driving the news: The biggest reason given for opening an account was the desire to easily receive stimulus checks and other government payments during the pandemic. - The second-biggest reason was getting a new job.

Between the lines: The pandemic accelerated the mobile banking revolution. In 2017, the most popular method that households used for accessing their bank accounts was going to a physical bank teller. That was the preferred channel for 25% of households, while mobile banking was popular with only 15%, per the FDIC. - In 2021, just four years later, tellers were the preferred choice of only 15% — while mobile banking was the go-to channel for 44%.

The intrigue: Klaros senior advisor and former Green Dot Bank CEO Mary Dent has a good question. If almost everybody is banked, why do check cashers still exist? - The answer: Not everybody is comfortable banking with an app. For people living paycheck-to-paycheck, mobile check deposit can take too long to clear; people with outstanding debts might also fear that their funds will be frozen by creditors.

The bottom line: Most of the remaining unbanked are unbanked by choice, says Dent. If you rationally don't trust banks, then you won't want to deposit your money with one. That helps explain why Black and Hispanic Americans have much higher unbanked rates than white Americans at every level of the income spectrum. | | | | | | | | A message from Blackstone | | Blackstone's approach in a volatile market | | |  | | | | Amid concerns about inflation and the economy, global head of private equity Joe Baratta discusses the importance of sector selection and business quality. See how Blackstone has positioned its investment portfolio for today's environment. | | | | | | 4. Where the rich pay much less |  Data: Insurify; Chart: Axios Visuals If you have a bad credit score, you will pay a lot more for car insurance, per Insurify's 2022 auto insurance trends report. - That's unless you live in one of the handful of states that ban the practice — including California, Hawaii, Maryland, and Massachusetts.

Why it matters: This is obviously and deeply unfair. But empirically speaking, insurers say that credit score is a much better predictor of future claims than any other metric. So they will continue to use it unless the practice is outlawed. | | | | |  | | | | If you like this newsletter, your friends may, too! Refer your friends and get free Axios swag when they sign up. | | | | | | | | 5. Beware bewitching single currency dreams |  | | | Illustration: Shoshana Gordon/Axios | | | | Luiz Inácio Lula da Silva, Brazil's president-elect, is resuscitating the dream of a Latin American single currency. It's an idea that plays well on the campaign trail, but it would be a disaster in practice. Why it matters: The tensions between economics and politics tend to run high in Latin America, which has a long history of disastrous monetary policy. - The current status quo, where most countries have free-floating and relatively stable national currencies, is by historical standards pretty successful. Dismantling it for political reasons would be a very bad idea.

How it works: The theory of optimal currency areas was first fleshed out in 1961, in work that eventually won a Nobel Prize for Robert Mundell. In order for a single currency to be a good idea, four facts have to obtain: - Free movement of labor

- Free movement of capital

- Fiscal policy that transfers money from rich areas to poor areas

- Broadly synchronous business cycles.

The big picture: Even a small Latin single-currency area would only satisfy one of the four criteria — there are definitely countries that could negotiate free movement of capital. - Open borders, however, where someone from, say, Paraguay would be free to live and work in Chile, are a non-starter.

- Similarly, Uruguayans are not going to want to send large annual sums of money to Bolivia.

As for business cycles, an influential 1993 paper by Barry Eichengreen looked at cross-correlations between 11 different Latin American countries. Of the 55 possible pairings, only four showed significant positive correlations. - Those findings were upheld by later analyses in 2003 and 2018.

The bottom line: It's easy for politicians to say that a single currency would help give Latin America more economic weight versus the U.S. dollar. In reality, however, it would probably just cause painful internal ruptures, just like we saw within the Eurozone in 2011. | | | | | | | | A message from Blackstone | | Identifying opportunities amid economic uncertainty | | |  | | | | Investors today face inflation, rising rates and an uncertain economic outlook. Blackstone's global head of private equity Joe Baratta talks about identifying high-quality businesses with strong secular tailwinds that have potential for long-term growth. | | | | Thanks to Kate Marino for editing and Elizabeth Black for copy-editing today's newsletter. |  | | Why stop here? Let's go Pro. | | | | | | Axios thanks our partners for supporting our newsletters. If you're interested in advertising, learn more here.

Sponsorship has no influence on editorial content. Axios, 3100 Clarendon Blvd, Arlington VA 22201 | | | You received this email because you signed up for newsletters from Axios.

Change your preferences or unsubscribe here. | | | Was this email forwarded to you?

Sign up now to get Axios in your inbox. | | | | Follow Axios on social media:    | | | | | |

No comments:

Post a Comment