Despite the recent drop we saw due to Nvidia’s dip…

The market is still very close to record highs.

But when stocks are expensive, options are expensive… especially when you’re swing trading.

I hate that, and I’m sure you do too!

It’s why I’ve been doubling down on a special trade on these 0DTE options…

Not only are they cheap and can be traded inside any regular brokerage…

But just a TINY move in the underlying asset can lead to payouts of 50% or more within 24 hours.

Now imagine having a way that points out exactly when the said asset will most likely breakout or breakdown before it happens…

Without relying on laggards like the Really Stupid Indicator (RSI).

Giving you a chance to target 50% or more in less than an hour!

That’s the kind of advantage you get with this secret here.

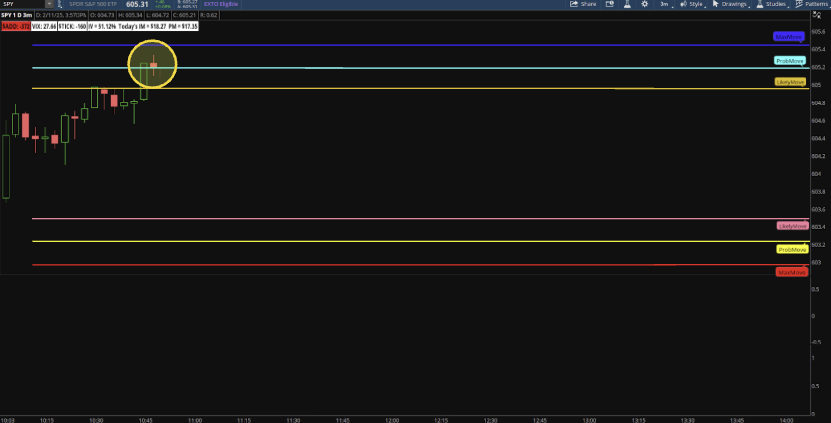

Just take a look at what happened on February 10th… this secret signaled that the SPY was about to break down.

Any regular trader with a basic trading account could have placed a simple trade at this point…

And sure enough, once the SPY reversed in less than an hour, that would have been a 67% gain.

Now, there’d have been smaller wins and those that didn’t work out…

But when you combine the power of daily options (0DTE) with this special zone…

You get the chance to turn breakouts and breakdowns into shots at 50% or more in 60 minutes or less.

That’s why I want to give you a free rundown of how I use this secret…

The one ticker to focus on, when to buy and sell… and a whole lot more!

Naturally, I won’t make reckless guarantees when it comes to trading…

But, you’ll also see how to trade the hottest 3-5 0DTE setups every market day…

Go here to get the full scoop for free.

By clicking the link above you agree to periodic updates from The TradingPub and its partners (privacy policy)

Why Walmart, Target and TJX Got Such Different Reactions After Earnings

Submitted by Leo Miller. Published: 5/25/2026.

Key Points

- Despite all three posting solid results, TJX Companies rose 5.6% after earnings, while Walmart fell 7.3% and Target dropped 3.9%.

- Walmart maintained its fiscal 2027 outlook after a roughly 25% six-month rally, giving investors little reason to push shares higher.

- TJX raised full-year sales and EPS growth guidance and increased its share buyback spending plans by $250 million, to as much as $3 billion.

- Special Report: The Biggest IPO Ever: Claim Your Stake Today

Retail earnings season delivered a clear reminder that good results are not always enough.

Walmart (NASDAQ: WMT), Target (NYSE: TGT) and TJX Companies (NYSE: TJX) all posted solid quarterly numbers recently, but investors reacted to the reports very differently.

The #1 stock to buy BEFORE the June 12th filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereFor Walmart and Target, strong sales growth was overshadowed by already elevated expectations and lingering guidance concerns. For TJX, a cleaner setup, stronger outlook and larger buyback plan gave the market a reason to reward the stock.

Walmart: After Its Big Rally, A Strong Quarter Wasn’t Enough

Arguably, the biggest disappointment from the latest round of retail earnings reports was Walmart. Overall, WMT stock dropped 7.3% after it released earnings on May 21.

But the problem wasn’t that Walmart's business wasn't performing well—it most certainly was. The company saw revenue grow by more than 7% year over year (YOY), or 5.9% on a constant-currency basis, to $177.75 billion. That marked Walmart's fastest revenue growth since calendar Q1 2023. Adjusted earnings per share (EPS) also rose solidly by 8% YOY. Both figures slightly beat Wall Street estimates.

But investors wanted more than a solid quarter. They wanted Walmart to raise its forward expectations as well.

Before its post-earnings decline, Walmart shares had delivered a total return of approximately 25% over the prior six months. That was nearly double the S&P 500’s return of about 13% over the same period.

Walmart, however, maintained its full-year fiscal 2027 outlook. After the stock’s sharp rally, that decision left investors with little incremental reason to keep bidding shares higher.

Note that the company’s fiscal reporting period is several quarters ahead of the calendar year period. The company continues to expect full-year adjusted EPS in the range of $2.75 to $2.85. Additionally, Walmart sees adjusted EPS coming in between 72 cents and 74 cents next quarter—slightly below what analysts had projected.

Target: Returns to Growth, But the Stock Still Lost Ground

Target also received no love from investors after its latest report, with shares falling 3.9% afterward.

Notably, Target has gone on an even more impressive run than Walmart, delivering a total return of over 45% in the last six months.

The company recorded net sales growth of 6.7% YOY, with total revenue rising to $25.44 billion. This ended a five-quarter streak of Target posting negative sales growth and marked the company’s highest growth rate since calendar Q4 2021. Adjusted EPS also climbed by 32% YOY.

Overall, the company’s sales growth beat estimates moderately, while EPS growth far outpaced them.

Target even increased its guidance, doubling its net sales growth expectations for the full year from 2% to 4%. It also sees adjusted EPS coming in at the high end of its $7.50 to $8.50 range. However, the firm also noted that it is facing tougher comparisons in Q2 and more challenging cost headwinds in the first half of the year. That likely tempered investor enthusiasm around Target’s otherwise strong showing.

Still, Target received analyst support, with many raising their price targets after the earnings report. The average of targets updated after the report was just under $140, considerably higher than the MarketBeat consensus price target around $125. That updated average target implied upside of around 10% in shares.

TJX: Gave Investors the Forward Momentum They Wanted

TJX stood out not only for its strong underlying performance but also for the positive reaction it received from investors.

The company posted revenues of $14.32 billion, an increase of over 9% YOY, marking TJX’s fastest growth rate in two years. Adjusted EPS rose even faster, climbing 29% YOY to $1.19. Both figures exceeded expectations, with TJX posting a large 17-cent bottom-line beat.

TJX also increased its full-year guidance. The company now expects consolidated sales to rise by 5% to 6% YOY, up from its previously forecasted growth of 4% to 5% YOY. Pre-tax profit margin guidance also got a boost, moving to a midpoint estimate of 11.95%, an increase of 20 basis points from prior estimates. Additionally, EPS growth expectations increased to a range of 7% to 9% YOY from 4% to 6% YOY.

It seems investors were likely more willing to reward TJX because the stock had not already gone on a strong run like the other two names. Before its post-earnings gain, TJX shares were up less than 5% over the past six months. In this case, a lower bar helped, and shares moved up by around 5.6% after the earnings release.

Adding to the positives, TJX announced an increase to its share buyback guidance. This is not a new authorization, but rather TJX telling investors how much it actually plans to spend on buybacks. Overall, the company increased its buyback spending plans by $250 million, to between $2.75 billion and $3 billion. After spending $604 million on buybacks during the quarter, this suggests the firm plans to spend around $2.25 billion on buybacks during the rest of the year. That would equal approximately 1.3% of its market capitalization.

TJX also received several price target increases after its results. The analyst consensus price target sits around $175, implying about 10% upside from current levels.

Amazon's Alexa for Shopping Strengthens an Already Strong Bull Case

Submitted by Sam Quirke. Published: 5/27/2026.

Key Points

- Amazon has retired its Rufus chatbot and launched Alexa for Shopping, a unified AI assistant combining product expertise with full customer history across devices.

- The move is the latest visible proof point of a broader AI transformation increasingly showing up across Amazon's business, from AWS to retail.

- Analysts are calling for as much as 40% upside from current levels, as the stock continues to go from strength to strength.

- Special Report: The Biggest IPO Ever: Claim Your Stake Today

Shares of Amazon.com Inc (NASDAQ: AMZN) are trading around $270 this week as they continue to consolidate just below the all-time high set earlier this month, following a strong earnings report. All told, the stock is up more than 30% in less than two months, a run that has rewarded investors who held on through a difficult start to the year.

Much of that momentum has been driven by growing conviction around Amazon's AI ambitions and the early signs that they are beginning to pay off. A recent announcement about its plans for the Alexa assistant may be the clearest signal yet of what that looks like in practice. It was recently reported that Amazon officially retired its generative-AI shopping assistant, better known as Rufus, and launched Alexa for Shopping. This unified AI assistant essentially merges Rufus's product knowledge and Amazon shopping history with the broader capabilities of its Alexa platform.

The #1 stock to buy BEFORE the June 12th filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereThe goal, in Amazon's own words, is to build “the world’s best, most personalized AI assistant for shopping.” For investors, though, the more important question isn't whether the product delivers on that promise in isolation. It's what this move says about the broader direction of the business.

What Alexa for Shopping Actually Does

The core logic behind the new product is simple. Until now, Rufus and Alexa operated as entirely separate consumer experiences that didn't share memory or context. An Amazon customer could research a purchase on an Alexa device and then have to start the process over with Rufus when they were ready to shop on Amazon. Alexa for Shopping fixes that by creating a continuous, highly personalized thread that follows the customer across devices, apps, and the website.

In practical terms, for the first time, a shopper can brainstorm a purchase with Alexa on their Echo, set a price alert in the app, and complete the transaction by voice when the price is right. It's a small change in theory, but in practice, it closes the loop on a shopping experience that has been surprisingly fragmented for longer than it probably needed to be.

The Competitive Pressure That Forced Amazon's Hand

This change was not made lightly, especially given that Rufus was only launched in 2024. However, the past few months have seen the likes of ChatGPT, Google's Gemini, and Perplexity roll out AI shopping features, each posing a serious threat to Amazon's position as the default starting point for shoppers' research.

That means the merger of Rufus and Alexa carries real strategic weight, as it effectively creates a quick, robust moat around its e-commerce business. As Amazon pointed out recently, these rival tools will always struggle to deliver a better shopping experience because they are forced, by default, to scrape web results rather than pull real-time product, pricing, inventory, and shopper data directly.

That's a gap that's very hard to close from the outside, and it should serve as a tailwind to Amazon’s e-commerce business in the coming quarters.

AWS Is Still the Main Engine for Growth

That said, while the Alexa for Shopping launch makes for compelling reading, the bigger driver of investor sentiment right now, and ultimately what will drive the stock in the near term, is what's happening at AWS. Amazon stopped being valued simply as an e-commerce company many years ago, and the shift toward viewing it as one of the key infrastructure providers powering the AI boom is still gathering pace.

The company's massive capital expenditure plans, which spooked investors earlier this year, are increasingly being read as strategic conviction rather than reckless spending. The payoff is beginning to emerge, as seen in AWS's growth trajectory updates and a substantial contracted backlog that bodes well for the coming years.

Recent commentary from analysts suggests AWS is still in the early stages of a reacceleration, as additional capacity comes online and long-term AI partnerships begin to deliver revenue. This is ultimately the real reason the stock is up more than 30% in just a few weeks, and why it could keep gaining over the coming months.

The Bull Case Keeps Getting Stronger

Still, the Alexa for Shopping update is a nice addition to the broader tailwinds. Put it all together, and the bull case for further gains rests firmly on a company that’s executing well across cloud, retail, and AI simultaneously. And in an ideal world, that’s exactly as it should be.

Wells Fargo and TD Cowen's recently updated price targets of $312 and $350, respectively, reflect the stock’s potential, and this strategic pivot to Alexa for Shopping is the kind of move that reinforces that upside rather than creating it. For a company that has already reshaped how the world shops once before, this latest ambition to do it again through AI should get investors excited.

This email is a paid advertisement provided by The TradingPub, a third-party advertiser of MarketBeat. Why was I sent this email?.

The majority of trades expressed are based on historical signals from Alpha Zone Pro with the benefit of 20/20 hindsight unless otherwise stated. While Roger has been using Alpha Zone Pro with great success in his premium Telegram channel, we can't guarantee future results and you may lose money. What you will see today are some of the best examples. There have been bigger winners, there have been smaller winners and there have been losers. Since Alpha Zone Pro is a tool for traders and not a trading service, profits and performance will vary among users.

If you have questions about your newsletter, please contact our U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Place, Sixth Floor, Sioux Falls, S.D. 57103. U.S.A..

Post a Comment

0Comments