|

A message from i2i Marketing Group, LLC

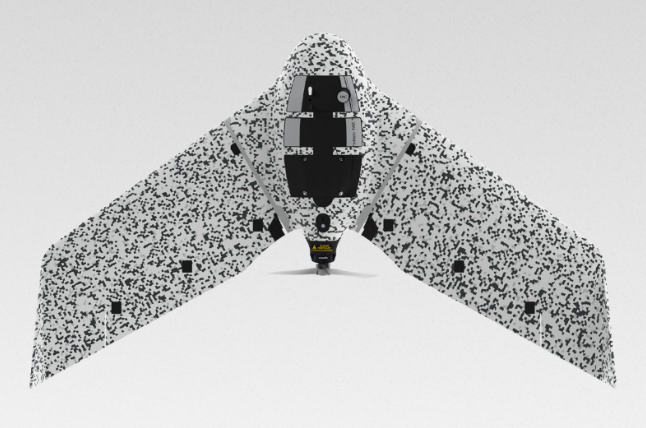

From farming fields to military airbases, drones are rapidly moving from novelty gadgets to essential tools across nearly every major industry. And the numbers being reported by domestic players in the space are starting to back that up in a big way. The global military Unmanned Aerial Systems (UAS) market is projected to grow from $14 billion in 2024 to $23.1 billion by 2033, totaling $186.8 billion in cumulative procurement over the next decade. The global commercial drone market is projected to grow from $83.97 billion in 2025 to approximately $1.75 trillion by 2035 at a 35.5% compound annual growth rate. With U.S. policy continuing to push back against Chinese-made drones and components, the door is opening for NDAA-aligned domestic manufacturers to step up. AgEagle Aerial Systems Inc., now operating as EagleNXT (NYSE: UAVS), is a NYSE American-listed company that designs and manufactures defense-grade fixed-wing drones, supplies multispectral sensors to over 150 drone platforms worldwide, holds Blue UAS Cleared List approval from the U.S. Department of Defense for its eBee TAC and eBee VISION platforms, and is now expanding into the precision loitering munition segment through its Aerodrome Group equity investment. What Does the Company Actually Do? EagleNXT operates across four core areas. The first is its eBee tactical drone fleet, which builds defense-grade fixed-wing platforms for military, government, and commercial customers across reconnaissance, mapping, and surveillance missions. The second is its MicaSense multispectral sensor business, which now powers over 150 plus drone platforms worldwide and has been featured in over 100 peer-reviewed research publications. The third is its U.S. defense procurement pipeline, which currently includes 35 high-probability-of-win UAS proposals and three active U.S. DoD orders. The fourth is its newly announced precision loitering munition program through Aerodrome Group, with a framework for a U.S.-based joint venture. The idea behind the eBee model is straightforward: deliver defense-grade reliability in a fixed-wing form factor that one soldier can deploy in three minutes. Think of it as the tactical mapping and ISR equivalent of an everyday platform that procurement officers can buy without writing a multi-year program around it. The Product Lineup EagleNXT has developed several drone platforms, each designed for a different mission profile. The eBee TAC is the company’s flagship defense platform. It weighs roughly 3 pounds, is acoustically undetectable at 300 meters AGL, and is the first and only fixed-wing drone on the U.S. Department of Defense Blue UAS Cleared List. Key applications include:

- Tactical mapping with centimeter-level RTK/PPK accuracy and no ground control points

- Reconnaissance and border surveillance with AES-256 encrypted radio link

- A 90-minute flight time, a range of up to 34 miles, and a fly-away probability of 1 in 1,750 hours

- Already logged 173,600 plus cumulative flights and over 90,490 flight hours across operational deployments

The company has also built out a broader fixed-wing fleet for more specialized tasks:

- The eBee VISION is the ISR flagship designed for real-time intelligence, surveillance, and reconnaissance, featuring HD live video with 32x digital zoom, integrated thermal imaging, NDAA compliance, and NATO STANAG 4609 compliance for GNSS-denied environments

- The eBee X is the world’s most widely deployed commercial fixed-wing drone, already cleared to fly Operations Over People in Canada and Beyond Visual Line of Sight in Brazil, with a 15-unit order recently placed by a European tier-1 defense integrator

- The MicaSense RedEdge-P Triple is the flagship multispectral sensor delivering 15 spectral bands at 2 cm resolution, a 2 terabyte removable storage that enables up to three captures per second

- The Aerodrome loitering munition program is a newly announced precision-strike initiative through a strategic equity investment, with a framework for a U.S.-based joint venture supporting localized production for the loitering munition segment

Record Revenue Growth and Recent Results On November 17, 2025, EagleNXT reported third quarter fiscal year 2025 results showing the strategy converting into reported numbers. Drone revenue grew 35% year over year in FY2025, revenue came in at $12.8 million, and net income for fiscal 2024 was $7.06 million, up 211%. The product and customer mix shows the strategy reading through to the income statement:

- eBee defense platforms contributed the largest growth segment, with active deployments to the U.S. Air Force, U.S. Marine Corps, U.S. Border Patrol, French Army (a $3.4 million order, the largest single order in company history), and NATO/KFOR forces

- MicaSense sensors have shipped to customers across 10 countries on six continents since the August 2025 launch of the RedEdge-P Green, with a January 2026 U.S. Army purchase including S.O.D.A. 3D and Duet M sensors

- Gross profit rose to $6.3 million for fiscal 2024, up 14.5% year over year

- Operating expenses decreased 27.9% in Q1 2025 versus the prior year period, showing simultaneous revenue growth and cost discipline

- Capital structure was strengthened in November 2025 with a Series G Preferred Stock financing structure providing the capacity to raise up to $100 million in gross proceeds, subject to conditions, and NYSE American compliance was fully restored in January 2026

On the order front, EagleNXT added multiple new customers in the past 90 days, including a January 2026 U.S. Army order for six eBee TAC drones, a February 2026 15-unit eBee X deal with a European tier-1 defense integrator, the first eBee VISION deployment to a Canadian operator, a Malaysian government procurement through reseller Surmap Sdn Bhd, and six eBee TAC drones to Poland through Dilectro. Pipeline activity now includes 35 high-probability-of-win UAS proposals actively in motion and three current U.S. DoD orders being competed.

The Defense Angle EagleNXT is actively pursuing government and military contracts, and the past 90 days have brought meaningful progress. The company has completed deliveries to the U.S. Army, secured a Defense Logistics Agency quote pathway through four prime defense contractors, and announced a strategic equity investment in Aerodrome Group Ltd. on March 6, 2026, an Israel-based developer of precision loitering munitions. More recently, on April 14, 2026, the company announced a $10 million strategic investment in ThirdEye Systems Ltd., an Israeli developer of AI-powered counter-drone systems, and the launch of ThirdEye USA, LLC, a 51%-owned U.S. joint venture that will produce counter-drone systems out of the Allen, Texas headquarters beginning May 2026. Its defense go-to-market strategy includes several key elements:

- Blue UAS Cleared List approval for both eBee TAC and eBee VISION, the Pentagon’s vetted roster of secure, NDAA-compliant drones approved for government and military procurement, with eBee TAC the first and only fixed-wing drone on the list

- U.S.-based manufacturing coming online in May 2026 at the new Allen, Texas facility in the northeast Dallas-Fort Worth metroplex, supporting Made-in-America procurement for the eBee VISION drone and MicaSense sensor line

- A defense-experienced leadership team anchored by Chairman Capt. Grant Begley (Ret.), a U.S. Naval Academy graduate and Top Gun designated pilot, and CEO Bill Irby, a U.S. Naval Academy graduate, former Marine Corps officer, and 30-year defense industry veteran

- A pipeline of 35 high-probability proposals submitted through four prime defense contractors, leveraging the Simplified Acquisition Threshold to compress procurement timelines from months to days, with DLA quotes valid through January 2027

- Regulatory firsts that include the first FAA approval for Operations Over People and Beyond Visual Line of Sight in the United States, the first EASA C2 Certificate for BVLOS in Europe, plus NATO STANAG 4609 compliance

- A growing precision-strike portfolio through the new Aerodrome Group equity stake plus the framework for a U.S.-based joint venture, expanding the company from tactical mapping and ISR into the loitering munition segment that has reshaped the modern battlefield

The company has also received active sensor orders from Oak Ridge National Laboratory and the U.S. Naval Research Laboratory, alongside U.S. Border Patrol deployments for surveillance and monitoring operations.

Manufacturing and Global Footprint EagleNXT has built out a notable global manufacturing and operational presence. Its Switzerland production facility has been the historical anchor for eBee fixed-wing drone manufacturing and assembly. The company is now adding a U.S. production facility in Allen, Texas, with operational startup expected in May 2026, supporting eBee VISION drone and MicaSense sensor production for the U.S. government, parapublic, and research markets. The company maintains active customer relationships across North America, Europe, the Middle East, and Asia, with the eBee fleet logging over one million flights globally. The Allen, Texas headquarters, relocated from Wichita, Kansas in January 2026, serves as both the U.S. headquarters and a strategic gateway to the Dallas-Fort Worth aerospace ecosystem and major U.S. defense customers.

Top 5 Reasons To Keep An Eye On (UAVS)

- Drone Revenue Growth: 35% year-over-year drone revenue growth in FY2025, FY2025 revenue of $12.8 million, and net income of $7.06 million up 211%.

- Pentagon Validation: Both eBee TAC and eBee VISION on the U.S. Department of Defense Blue UAS Cleared List, with eBee TAC the first and only fixed-wing drone on the list.

- NDAA-Aligned Manufacturing: U.S. production at the new Allen, Texas facility coming online in May 2026, supporting Made-in-America procurement for the eBee VISION drone and MicaSense sensors.

- Defense Portfolio Expansion: Two strategic equity investments, Aerodrome Group for precision loitering munitions and a $10M stake in ThirdEye Systems for AI-powered counter-drone systems, with two U.S.-based joint venture frameworks anchored at the Allen, Texas facility, placing EagleNXT on both the offense and counter-drone sides of the modern battlefield.

- Procurement Pipeline: 35 high-probability-of-win UAS proposals in motion, three active U.S. DoD orders being completed, and DLA quotes valid through January 2027 via four prime defense contractors.

Worth Keeping an Eye On? EagleNXT presents an interesting combination of defense-grade drone hardware, a Pentagon-vetted product line, a multispectral sensor business that compounds with every new platform integrated, and an emerging precision-strike program under one umbrella. The company’s product strategy has now translated into reported numbers, with FY2025 drone revenue up 35% year over year and FY2025 revenue of $12.8 million. Defense ambitions have also progressed, with both eBee TAC and eBee VISION on the Blue UAS Cleared List, a new U.S. manufacturing facility coming online in May 2026, and a precision loitering munition program now in motion. For those interested in the commercial and defense drone space, UAVS may be a name worth watching as the company works toward its U.S. manufacturing launch, defense procurement conversions, and continued international expansion. Know The Risks… EagleNXT is a small-cap technology company with a limited revenue history relative to its larger defense peers and a business model that depends heavily on winning new government and military contracts. The company’s pipeline of 35 high-probability proposals carries execution risk, and there is no guarantee that those opportunities will convert into purchase orders, deliveries, or recurring revenue. Defense procurement timelines remain unpredictable, as DLA quotes, prime contractor relationships, and Simplified Acquisition Threshold processes can be delayed, modified, or canceled. International expansion across Canada, Malaysia, Poland, and the UAE adds regulatory and geopolitical exposure. This is a high-risk investment in an emerging-defense company, always review SEC filings carefully and do your own due diligence. Anyways… That’s all for now!

Additional Reading from MarketBeat Media

Monolithic Power Systems: AI Stock Beat, Raised and Upgraded Post-EarningsReported by Leo Miller. Posted: 5/5/2026.

Key Points

- Monolithic Power Systems has been a top-performing chip stock in 2026, and its latest financials show why.

- The company exceeded estimates across the board and greatly increased its AI growth expectations.

- Wall Street analysts issued large price target increases despite shares falling slightly.

- Special Report: Warning: Your AI Portfolio Could Be Obsolete by Year's End

Stocks like NVIDIA (NASDAQ: NVDA) and Broadcom (NASDAQ: AVGO) often dominate semiconductor headlines, but one lesser-known chip stock has outpaced them in recent returns. That stock is Monolithic Power Systems (NASDAQ: MPWR), which has surged more than 70% so far in 2026. By comparison, NVIDIA is up less than 10% this year, while Broadcom’s return is around 20%.

Most investors are reacting to the Iran strikes without understanding the underlying motive driving the decision.

Addison Wiggin, Founder of Grey Swan Investment Fraternity, says there is a hidden reason behind the bombing - and knowing it could change how you position your money right now. Discover the real reason behind the Iran strikes before markets react

Part of Monolithic’s strong performance reflects the growing importance of energy efficiency in data centers. GE Vernova (NYSE: GEV) is another stock benefiting from this trend, with shares up more than 60% in 2026. Monolithic makes power chips and modules that regulate energy use across systems, including AI equipment. Monolithic reported its latest financial results on April 30, and its share price fell roughly 2% the following trading day. Still, Wall Street analysts sharply raised price targets after the release, suggesting investors see additional opportunity. Monolithic’s Q1: 2 Beats and Stellar GuidanceIn Q1 2026, Monolithic posted revenue of $804 million, up 26% year over year (YOY). That beat expectations near $782 million (about 23% growth). Adjusted earnings per share (EPS) came in at $5.10, also up 26%, topping estimates of $4.90 (roughly 21% growth). But the guidance grabbed the most attention. For Q2 2026, Monolithic forecasts revenue of $900 million at the midpoint, implying 35%–36% growth — the firm's highest growth rate since Q1 2025. That far exceeded estimates near $817 million (about 23% growth). Monolithic did not provide explicit EPS guidance for the quarter. AI Drives Big Growth Across Two End MarketsResults were strong across most of Monolithic’s key end markets. Communications revenue increased 55.5% YOY, accounting for 13.9% of total sales. Enterprise Data — which includes power-management solutions for AI and server applications — jumped 97.7% YOY and has become the company’s largest end market, at 32.7% of total sales. Automotive rose 5.1% YOY, and Industrial grew 14.2% YOY, making up 18.9% and 6% of revenue, respectively. Storage and Computing declined 7.5% YOY, and Consumer fell 4.2% YOY, representing 21.7% and 6.8% of revenue. Overall, gains in the company’s strongest end markets more than offset declines elsewhere. No single end market accounted for more than one-third of sales, underscoring Monolithic’s diversification. AI demand appears to be the primary driver. For 2026, Monolithic now projects Enterprise Data sales will rise by at least 85% YOY — a substantial increase from its prior floor of 50%, which itself had been raised from earlier expectations of 30%–40%. Communications is also tied to AI. Revenue in that segment rose 33% compared with Q4 2025, driven by power solutions for optical modules and switches. Monolithic supplies modules for optical transceivers, a part of the AI networking ecosystem experiencing surging demand. When an analyst asked whether Communications revenue could grow as fast as, or faster than, Enterprise Data, CEO Michael R. Hsing replied, "Yes," though he provided no specific figures. The prospect of multiple end markets growing 85% or more in 2026 is encouraging. Analysts Boost Targets Big-Time After Monolithic’s ReportThe MarketBeat consensus price target on Monolithic sits near $1,600, implying limited upside from current levels. But price targets shifted materially after the earnings release. Among analysts that updated targets (and for which MarketBeat had prior data), the average target rose by 29% — a very significant move that contrasts with the modest sell-off in the stock. Looking at all price targets issued after the results, the average was roughly $1,793, a notable increase over the consensus and implying about 15% upside from recent prices. The company’s financial performance is impressive, but the stock is not cheap. Continued strong execution could leave room for further gains, yet a slowdown in demand or a lapse in execution could trigger a significant decline after such a rapid rally. |

Post a Comment

0Comments