I'm issuing a new buy recommendation on one specific stock I call "Silicon Valley's Toll Collector."

Practically ALL of the biggest AI players, with their billion-dollar budgets, are essentially sending "toll money" to one single company. With 771 patents on its books, it has a competitive edge others can't compete with.

And it's now at the center of a cash stream which is growing higher and higher with no end in sight. And anyone, with an internet connection and a brokerage account, can gain exposure to it.

I'm expecting a major press release to drop from Silicon Valley's Toll Collector that day.

I believe this press release will include an update on how much this billion-dollar cash stream has grown over the past year. When Wall Street gets a glimpse of this number, it could send shockwaves through the entire financial world.

Once the news is out, there's no stuffing that 'genie' back into the bottle.

Results are not typical and will vary from person to person. Making money trading stocks takes time, timing, proper execution, dedication, and hard work. There are inherent risks involved with investing in the stock market, including the loss of your investment. Past performance in the market is not indicative of future results. Any investment is at your own risk.

Today's editorial pick for you

McDonald’s: Boring is Beautiful, But Only if You Own MCD Stock

It's not that surprising. McDonald's continues to caution about the low-income consumers who are not, as of yet, participating in the economic growth being reported. And McDonald's has the misfortune of being both iconic and polarizing. The company has its critics for everything from its menu to, recently, its pricing.

But a stock and a company are two different things. If you're an MCD stock shareholder, you know what that means. There are several companies that simply do what they do. That describes McDonald's.

Let's take a brief look at McDonald's earnings report and then explain why many investors know that, over time, a report is a moment in time, but the trend is always their friend.

Boring is Beautiful

McDonald's quietly delivered exactly what long-term holders want to see in the fourth quarter: steady growth, a clean beat on both the top and bottom line, and more evidence that its scale and value positioning still travel well globally. Revenue came in at about $7 billion, up high single digits year-over-year and 2.5% ahead of Wall Street expectations.

Adjusted earnings per share of $3.12 also topped consensus and marked solid double-digit growth versus last year. Under the hood, global comparable sales rose 5.7 percent, with positive guest counts and all three major segments contributing: the United States was the standout at 6.8 percent comp growth, International Operated Markets grew 5.2 percent, and International Developmental Licensed Markets added 4.5 percent.

Systemwide sales increased by double digits for the quarter and 7 percent for the full year, pushing total system sales above $139 billion and underscoring how much cash this "boring" brand actually moves through the system in any given year.

Double Beat, But a Cautious Tone

The market got the headline it wanted – a double beat – but the stock's muted reaction reflects the more cautious narrative around the consumer. Management is still leaning hard into value messaging because traffic growth is increasingly skewed toward higher-income guests, while lower-income diners remain under pressure from inflation in necessities, higher interest costs, and shrinking excess savings.

That's showing up in the mix. McDonald's is seeing healthy check growth, helped by premium and limited-time offers. But it has to be careful not to push too far on price at the risk of alienating the very customers who view McDonald's as an everyday affordable option.

On the margin side, the quarter benefited from operating leverage on higher sales and continued efficiency work under the company's "Accelerating the Arches" and "Accelerating the Organization" initiatives, although restructuring charges did create some noise in reported operating income.

Excluding those items, underlying operating income grew in the mid-single digits, which is respectable given wage and commodity pressures across the global restaurant industry. For income investors, the story remains intact: strong free cash flow supports a reliable dividend and buybacks, and the latest results don't challenge that capital-return thesis in any meaningful way.

A Global Brand That Just Keeps Grinding

Strategically, the quarter reinforces why McDonald's belongs in the "own it, don't trade it" bucket. All three geographic segments are growing comps, and the company continues to add restaurants, nudging total systemwide locations into the mid-40,000s and extending its reach into both developed and emerging markets.

Digital, delivery and loyalty remain important growth pillars: the app makes it easier to price-segment customers and offer targeted deals, while delivery expands occasions without needing to add dining room capacity. Those are exactly the kinds of incremental, execution-driven growth levers that may not excite traders on any single earnings day, but they compound nicely when you zoom out over three to five years.

Management's commentary also emphasized the brand's ability to flex across macro environments: when times are good, McDonald's participates with premium innovation and marketing; when times get tougher, it pivots to sharper value and traffic-driving offers.

Today, it is clearly leaning toward the latter, using bundles, national value platforms, and selective price rollbacks to defend visitation among more stretched households without giving away the store to customers who are still willing – and able – to trade up. The result is a quarter that may not have been spectacular enough to keep the stock bid up in the immediate aftermath, but it does extend the longer-term pattern this name is known for. That is modestly better-than-expected growth, resilient margins, and a business model that proves, once again, that "boring" can be a very attractive place to compound capital.

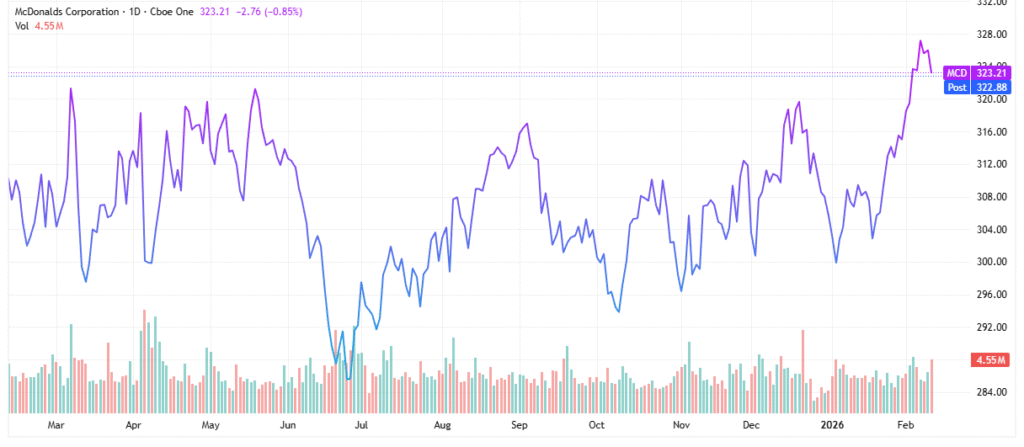

Look At This Chart, Not That Chart

McDonald's is a stock that you own, and not trade. Still, it's easy to be a buy-and-hold investor if you don't have to do the whole waiting thing. That's because part of owning a stock like MCD is that it's going to be boring at times.

Take for example, what's happened in the last 12 months. The stock's moved up and down and all around, and investors would have had a 4.24% stock price gain to show for it. Even factoring in the company's rock-solid dividend, you would only have had a total return of around 6.6%.

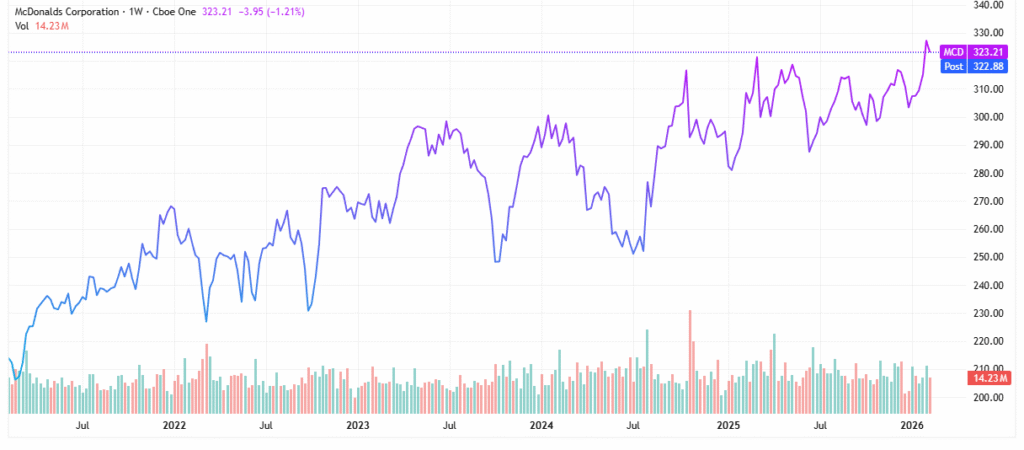

But that's not the chart you should look at. Here's the five-year chart for MCD stock:

Now we're talking. This is the type of chart that a buy-and-hold investor loves to see. The stock has been gently grinding higher. How high? Try a 50.9% gain in the stock price and a total return of over 69%. That means a $5,000 investment would be worth $8,450.

And that assumes you don't add any more to your account other than reinvested dividends. If you do, the return in terms of dollars would be even greater. That's the beauty of compounding. But you only get it if you buy the stock and hold it.

MCD Stock Could Be Due for a Pull Back

So if you don't currently own MCD stock, but think it has a place in your portfolio, it might be better to keep it on a watch list, for now. Looking back at the one-year stock chart shows the stock is a little extended.

If the choppy movement in after-hours trading extends into the market open, it could be a down day for MCD stock. That wouldn't be unusual for companies that give reports that are good, but not great.

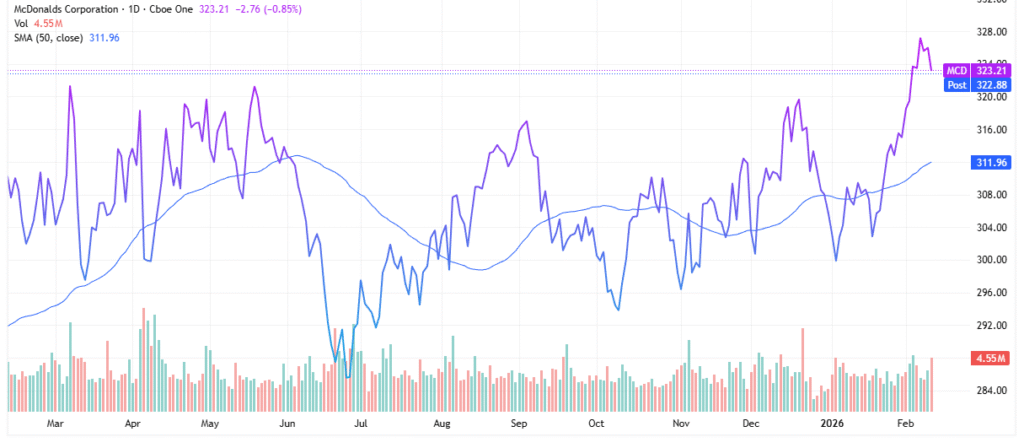

In that case, having the stock fall back to the 50-day simple moving average (SMA) at around $312 would be a good opportunity to start a position. And if the stock price were to drift down around the 200-day SMA, it would be all the better.

This is a PAID ADVERTISEMENT provided to the subscribers of Daily Options Signals Free Newsletter. Although we have sent you this email, Daily Options Signals and StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us. If you no longer wish to receive email from DailyOptionsSignals.com, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

Post a Comment

0Comments