|

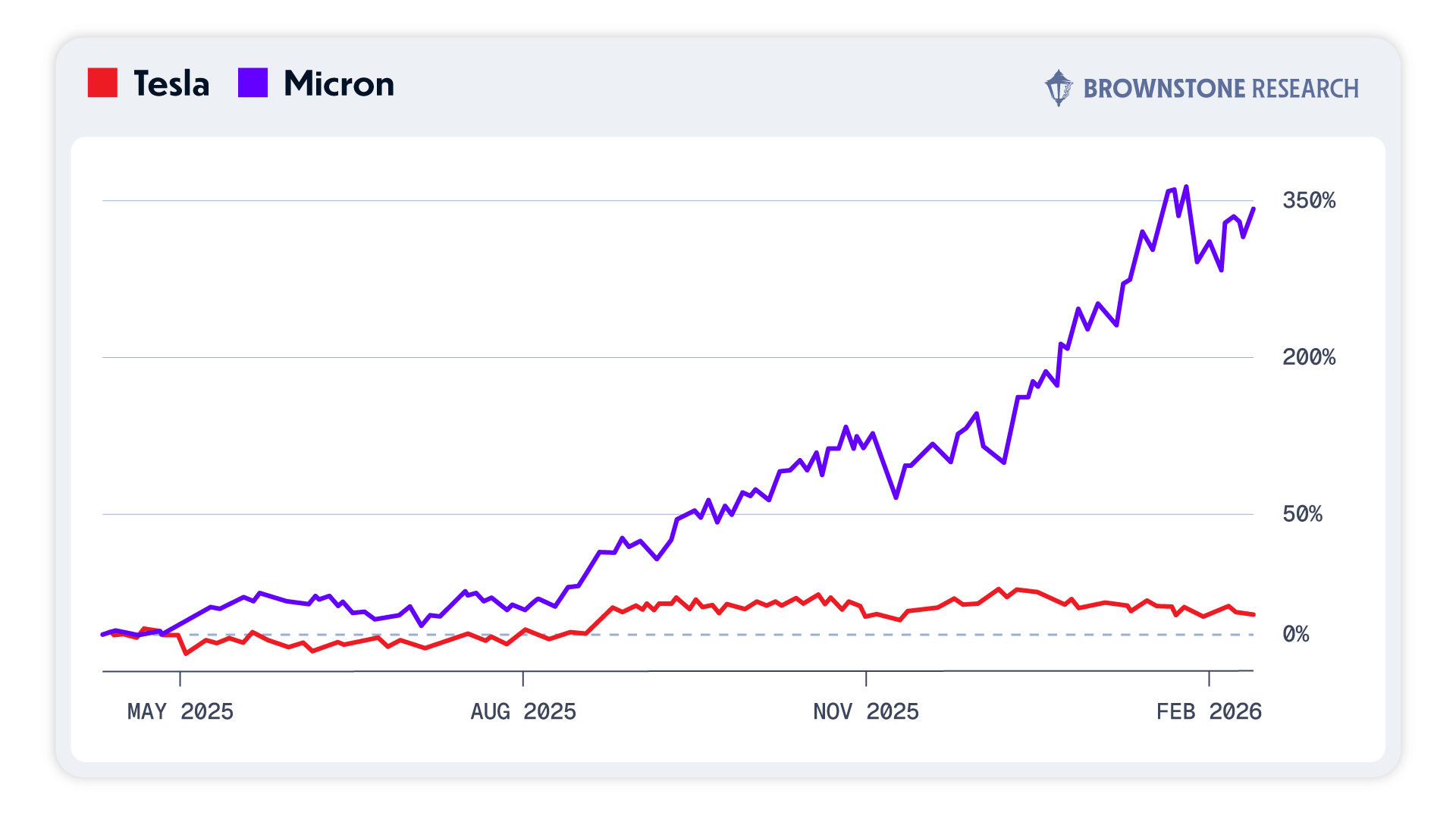

Editor’s Note: If you want to know which chipmaker could be the next NVIDIA, just ask Jeff Brown. He knows more about AI chips than practically anyone on the planet — Thanks to his senior executive roles at Qualcomm, Juniper Networks, and NXP Semiconductors… And Jeff just uncovered that one tiny chipmaker — 148 times smaller than NVIDIA — is set to provide Musk 5 billion chips in the next two years alone. Click here for the full story or read more below. Dear Reader, While everybody's talking about the SpaceX IPO… Too many investors are sleeping on the company's "hidden supplier." Just look at this chart.

The red line is Tesla… The purple line is Micron — a company that supplies Tesla with memory chips. Which stock would you rather have bought? I'm guessing Micron, if you prefer huge gains. Of course, Musk keeps his suppliers close to his chest… So most people have no idea Micron supplies Tesla. But, as a former senior executive in the semiconductor industry… When I saw Tesla's full self-driving computer, I could identify all the chips almost instantly. That's why I told my audience about Micron in October 2024. It has since outperformed Tesla by almost three times... Yes, three times one of the biggest wealth drivers on the planet. What's more, Micron crushed the wider market by a mind-blowing 15 times. Imagine bringing in 15 times more than your neighbors! And I've just identified another Musk supplier almost nobody knows about. See, there's this massive rush to get in on the SpaceX IPO… I think it's worth buying shares… But the company is already valued at $1.75 trillion. So, if we see a repeat of Micron outperforming Tesla… Isn't it better to get in on SpaceX's major supplier? Well, Musk just said a new piece of AI technology from SpaceX is "the only way to scale [AI]." And I've identified the one "hidden supplier" that could be the key provider for this new AI technology… The "hidden supplier" is set to provide Musk with 5 billion chips in the next two years… Yes, billion! That's 6.8 million chips every single day. And now is the time to react… Because I believe Musk is about to reveal this supplier to the world on July 21… And the share price could go parabolic. Click here to see the full story before it's too late. Regards, Jeff Brown Today’s editorial pick for you Pepsi Earnings Just Complicated The Story Investors Already BelievedPosted On Jul 09, 2026 by Grayson Cavern

Long before PepsiCo Inc. (NASDAQ: PEP) reported second-quarter earnings, many investors had already made up their minds. The debate had shifted away from quarterly results toward something much bigger: whether Pepsi had become another “ex-great” consumer stock. The reasoning sounded convincing. Consumers were moving toward healthier eating habits. GLP-1 weight-loss drugs threatened demand for salty snacks and sugary drinks. Years of price increases and shrinkflation had pushed shoppers toward cheaper private-label alternatives. Even loyal customers began questioning whether a bag of Doritos or a bottle of Pepsi was still worth the premium. Table of ContentsThe market reflected that pessimism. Pepsi shares entered earnings down sharply from their highs, with investors treating these headwinds less as temporary challenges and more as signs of permanent decline. Then PEP reported second-quarter revenue of $24.18 billion and core earnings per share of $2.20, both ahead of expectations, while reaffirming its full-year outlook. Those results don’t prove the bearish narrative is wrong. They do, however, force investors to confront a more uncomfortable possibility. What if Pepsi’s decline isn’t as irreversible as the market has already priced in? How Pepsi Is Challenging The Bear CaseOne strong quarter doesn’t erase the structural challenges facing Pepsi. Consumers are undeniably becoming more health-conscious. GLP-1 adoption continues expanding. Private-label brands remain aggressive competitors, particularly as shoppers search for cheaper alternatives. Pepsi itself acknowledged a difficult consumer environment and higher input costs. But the earnings also contained several data points that don’t neatly fit the market’s narrative. Organic volume returned to growth, rising 1%, while organic revenue increased 2.4%. Rather than relying entirely on higher prices, PEP generated growth through a combination of pricing, innovation and improving demand. North American Convenient Foods gained volume market share, supported by affordability initiatives and new product launches, suggesting consumers haven’t abandoned the company’s brands altogether. This means that the market has been pricing Pepsi as though consumer behavior has permanently shifted against its business. But these results now suggest consumers may be changing how they spend, but not necessarily who they spend with. Adaptation, Not Denial, Is Driving Pepsi’s ResponseWhat impressed me most wasn’t the earnings beat itself. It was management’s response to the challenges investors have been highlighting for months. Pepsi isn’t pretending GLP-1 drugs don’t exist. It isn’t dismissing changing consumer preferences or assuming shoppers will eventually accept endless price increases. Instead, the company appears focused on adapting through affordability initiatives, product innovation and disciplined execution. That strategy showed up across the financials. Core operating profit increased 4% while core operating margin reached 16.8%. Operating cash flow more than doubled to $2.37 billion during the first half of the year, allowing Pepsi to reaffirm plans to return approximately $8.9 billion to shareholders through dividends and share repurchases in 2026. Simply put, PEP is trying to stabilize demand while preserving profitability. Whether that strategy ultimately succeeds remains an open question. What this quarter demonstrates is that Pepsi still has meaningful levers to pull before investors can declare the company’s best days permanently behind Wall Street Still Isn’t Buying ItThe chart suggests investors remain unconvinced despite PEP’s better-than-expected quarter. Shares continue trading below their 20-day, 50-day and 200-day moving averages, preserving the downtrend that’s been in place for months. Even after briefly rebounding from the $135 support area late last month, the post-earnings selloff pushed shares back toward those lows, showing that sellers remain eager to fade any signs of optimism rather than chase the company’s improving fundamentals. If Wall Street believed Pepsi had already turned the corner, the stock would likely be reclaiming key technical levels instead of drifting back toward recent lows. For now, the tape says investors still view this as a company trying to stabilize, not one that’s already returned to sustainable growth. That’s exactly why these earnings deserve a closer look.

Has The Market Become Too Pessimistic?That brings us to valuation. At roughly $135 per share, PEP trades at a forward earnings multiple that sits below its historical average and at a discount to several large consumer staples peers, despite continuing to generate positive organic growth, substantial cash flow and one of the strongest dividend records in the market. If that discount reflects a business facing permanent decline, the valuation makes sense. But here’s the thing, the market has largely valued Pepsi as though changing consumer habits, GLP-1 adoption and private-label competition will erode the company’s competitive position for years to come. This quarter didn’t invalidate those concerns, but it did provide evidence that Pepsi is adapting more effectively than many investors expected. Positive organic volume growth, market share gains in North American Convenient Foods, reaffirmed guidance and stronger cash generation all point toward a business that’s proving more resilient than the prevailing narrative suggests. Now, while I don’t think one quarter is enough to declare Pepsi undervalued…I do think it’s enough to question whether Wall Street has already priced in the worst possible outcome. Because sometimes, that’s where the most interesting investment opportunities begin. This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above. Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe. StockEarnings, Inc |

Post a Comment

0Comments