Editor's Note: Marc Chaikin, the 60-year Wall Street legend who called Nvidia before it soared 45,000%, just came forward with another huge opportunity he’s spotted in the AI space. While the media is caught up in "SpaceX IPO fever" right now, the under-the-radar event Marc reveals below could give you access to three brand-new AI IPOs in a rare deal known as a "starburst." You may never get a chance to take part in one of these again in your life... and while it's speculative – this is your chance to get in very early while everyone's attention is elsewhere...

Dear Reader,

A tech firm that’s been called "the unseen winner of the AI race" could soon break itself up into three separate companies.

The next Netflix... The next Tesla... And the next Amazon are all poised to spin off just from this one stock.

That would create a once-in-a-lifetime opportunity for investors who buy shares in the company before it happens.

Buy shares of this stock today, and you could get the same amount of free shares automatically deposited in your account for each spinoff.

Meaning, 10 shares could turn into 30 shares overnight.

And you could wake up with the world's newest, hottest tech disruptors all sitting in your account – with no extra work on your part.

Believe me, when it happens, it feels like magic, but it's actually something called a "starburst."

This brilliant type of spinoff is especially rare in the tech industry.

And if the starburst announcement goes public (and it hasn't yet), it's going to be all the media talks about for a while afterward.

This potential "starburst" is my No. 1 recommendation for how average folks can set themselves up to benefit from what I'm calling AI's "jump to lightspeed" moment.

Get the early scoop on this huge opportunity right here.

Sincerely,

Marc Chaikin

Founder, Chaikin Analytics

P.S. In 2021, GE announced a starburst when the stock traded at just $67 per share.

They rolled out the deal in stages, and when it was done, shareholders owned three companies instead of just one. The share prices on those once they were individually valued? $75... $300... $614... That means that one starburst unlocked $184 billion for investors. I predict this AI starburst will be orders of magnitude larger. See why when you click here...

Applied Digital Is Building a $36 Billion AI Real Estate Empire

By Jeffrey Neal Johnson. Originally Published: 6/12/2026.

Key Points

- Applied Digital finalized a 15-year, 210-megawatt lease at Delta Forge 2, locking in approximately $36 billion in total contracted base-term lease revenue.

- A $1.59 billion senior secured notes offering will fund construction of a new 150-megawatt building and retire a high-interest Goldman Sachs bridge loan.

- Analysts at Northland Capital Markets project execution risk will decline between 2026 and 2027, with a consensus price target of $67.67 representing over 70% upside.

- Special Report: Forget SpaceX. Buy the company Musk can't replace.

Applied Digital (NASDAQ: APLD) recently finalized a 15-year, 210-megawatt lease at its Delta Forge 2 campus, signaling a clear transition from a high-beta crypto miner to a tier-one digital infrastructure landlord.

While retail investors temporarily dumped shares over macroeconomic inflation jitters and near-term debt mechanics, institutional capital recognizes a business holding approximately $36 billion in total contracted base-term lease revenue, with roughly 70% backed by U.S.-based investment-grade hyperscalers.

Where to Put $100 Before Trump's New Tech Law Rolls Out (Ad)

The Financial Times says a new tech law puts America 'on the verge of a financial revolution.' Yahoo Finance estimates it could unlock $400 trillion - but analyst Jeff Brown, who was consulted by Congressional offices on the legislation, believes the real figure could reach $2.6 quadrillion.

Brown says this shift will pour onto a new type of investment exchange - and he's showing investors how to position themselves starting with just $100.

Click here to see how Jeff Brown says to claim your stakeThe artificial intelligence (AI) land grab is accelerating, and hyperscalers require dedicated power and cooling at a scale previously unseen in commercial real estate. By securing a $5.2 billion baseline revenue commitment, expandable to $12.7 billion if all 30-year renewal options are exercised, Applied Digital locks in the long-term cash flow profile required to dominate the next decade of infrastructure deployment.

With an $11.1 billion market capitalization and 139% year-over-year top-line revenue growth, Applied Digital commands a premium valuation largely because of its ability to build high-density campuses faster than legacy data center operators. Operations for Delta Forge 2 are targeted to commence in the first quarter of 2028, effectively setting a hard date for when these multibillion-dollar contracts begin generating actual yield.

This Isn't Debt, It's Rocket Fuel

Markets often struggle to distinguish between short-term capital expenditure requirements and long-term value creation. Applied Digital recently suffered an intraday decline of 5.7%, sending its share price down to the $39 zone.

Retail sentiment quickly soured on the news that subsidiary Applied Digital ComputeCo 3 priced a $1.59 billion offering of 7.000% senior secured notes due 2031. This isolated price action, heavily influenced by a broader tech sector retreat ahead of May consumer price index data, masks the fundamental strength of Applied Digital's underlying asset base.

The $1.59 billion debt issuance is not reckless corporate borrowing to fund operational deficits. Applied Digital specified that the proceeds will be used primarily to construct a 150-megawatt fourth building, designated ELN-04, at the Polaris Forge 1 campus in North Dakota.

A portion of the proceeds will also be used to retire a high-interest bridge loan previously secured from Goldman Sachs. When you match these near-term leverage requirements against the massive 1.4-gigawatt contracted critical IT load across the five-campus portfolio, the debt mechanics reflect highly sophisticated capital alignment.

Applied Digital is leveraging predictable, contracted cash flows to bridge immediate development phases. A recently closed revolving credit facility with up to $350 million of committed capacity and an additional $200 million accordion option provides the necessary liquidity runway to maintain construction timelines. The subsequent 9.5% after-hours volume surge illustrates institutional investors stepping in to capitalize on retail misunderstanding of this secured debt structure.

Applied Digital's Waterless Moat Is Its Secret Weapon

Comparing Applied Digital to hardware-centric peers will help investors understand the company's strategic operational pivot. Companies like IREN (NASDAQ: IREN) and CoreWeave (NASDAQ: CRWV) assume more direct hardware depreciation risk by constantly purchasing and leasing the latest generation of graphics processing units.

Applied Digital operates more like an infrastructure landlord. The client supplies the highly volatile compute hardware; Applied Digital supplies the facility, the power, and the cooling. This facility-first real estate model may help insulate operating margins from rapid silicon obsolescence. Legacy miners like Core Scientific (NASDAQ: CORZ) are attempting similar pivots, but few possess the capital backing to execute at the gigawatt scale.

The unnamed counterparty at Delta Forge 2 is the same U.S.-based, investment-grade hyperscaler responsible for the two previous major leases across Applied Digital’s portfolio. This level of vendor stickiness is a strong validation of the underlying technology stack.

Delta Forge 2, located in an undisclosed southern state, will exclusively use proprietary waterless cooling technology alongside high-power-density infrastructure. As grid access tightens and nationwide environmental regulations on water use become more stringent, waterless cooling shifts from a luxury feature to a potential competitive advantage for massive training and inference workloads.

Today, 70% of Applied Digital's $36 billion base-term revenue backlog is supported by U.S.-based investment-grade hyperscalers, demonstrating that the market demands exactly what Applied Digital is building.

From High-Beta Bet to Blue-Chip Blueprint

Applied Digital's valuation multiples currently skew toward extreme growth expectations rather than present-day profitability. A price-to-sales ratio of 35 and a trailing 12-month earnings per share loss of 74 cents reflect an organization operating at the peak of its capital expenditure cycle. The current balance sheet debt-to-equity ratio sits at 1.65, a necessary byproduct of scaling multibillion-dollar facilities.

Despite the significant capital outlays, the execution risk narrative is shifting rapidly.

Northland Capital Markets analysts recently validated this infrastructure transition, projecting that execution risk will sharply decline between 2026 and 2027 as project deliverables come online. The analyst also stated that significant multiple expansion was possible, pushing the valuation toward 15x as tangible cash flows materialize.

The broader analyst community agrees, maintaining a consensus price target of $67.67, which represents over 70% upside from current levels.

Institutional investors reinforce this bullish outlook, as the $7.02 million in shares sold in the last quarter is vastly overshadowed by the $94 million spent on purchases. While some corporate insiders recently executed structured selling programs, these distributions reflect standard equity compensation realization rather than a broader executive exodus.

Short interest remains at healthy levels, suggesting the recent price action is driven purely by fundamental repositioning.

The elevated beta of 5.69 for Applied Digital remains a lagging indicator, permanently tethered to its past life managing volatile cryptocurrency operations.

As the market digests the bond-like cash flow profile created by 15-year take-or-pay utility contracts, the equity will naturally rerate. Institutional capital values the predictability of digital real estate multiples over the cyclicality of legacy bitcoin mining revenue.

Capturing Value Before the Walls Go Up

Shifting a multibillion-dollar business model from digital asset speculation to institutional real estate requires heavy capital deployment, and pricing volatility remains the admission price for early allocators. Applied Digital already holds the binding hyperscaler commitments necessary to support its corporate transition, shielding the balance sheet from some of the inherent cyclicality of the broader semiconductor and computing markets.

While current profitability metrics appear heavily depressed due to massive infrastructure investments, the forward-looking cash flows are supported by contracted hyperscaler leases rather than guaranteed by completed operations. The transition from construction to operation over the next 24 months will serve as the primary catalyst for sustained valuation expansion.

Investors may want to add Applied Digital to their watchlist, as the company is rapidly bringing its Delta Forge 2 and Polaris Forge 1 campuses online. Those with a higher risk tolerance might consider using the current debt-driven price volatility as an entry point before the broader market fully prices in the $36 billion contracted revenue backlog.

Okta’s AI Moment May Be Bigger Than Investors Realize

By Thomas Hughes. Originally Published: 6/16/2026.

Key Points

- Okta's fiscal Q1 2027 results showed revenue of $765 million, growing 11.2% year-over-year, driven largely by rising agentic AI demand.

- OKTA shares surged more than 30% following the earnings release, reaching a four-year high, with analyst consensus price targets rising 18%.

- Institutions own more than 85% of Okta shares and shifted from distribution to accumulation in Q2, while the company's debt-free balance sheet supports ongoing share buybacks.

- Special Report: Forget SpaceX. Buy the company Musk can't replace.

Okta’s (NASDAQ: OKTA) fiscal Q1 2027 earnings report changed the narrative by showing that the company’s strength and cash flow are being driven by AI-focused demand. While AI is disrupting SaaS stocks, that disruption is proving favorable, contrary to expectations, with cybersecurity at the forefront. The need is simple: AI must be secure at every level. Without security, AI is untrustworthy at best and dangerous at worst, and Okta is central to securing the global tech ecosystem.

Okta’s cloud-native, vendor-neutral approach to identity security means no vendor lock-in and the largest, broadest addressable market among its peers. The platform also integrates seamlessly, has nearly 100% uptime, and offers easy-to-use features that enable single sign-on for employees and streamlined on- and off-boarding for HR teams.

Where to Put $100 Before Trump's New Tech Law Rolls Out (Ad)

The Financial Times says a new tech law puts America 'on the verge of a financial revolution.' Yahoo Finance estimates it could unlock $400 trillion - but analyst Jeff Brown, who was consulted by Congressional offices on the legislation, believes the real figure could reach $2.6 quadrillion.

Brown says this shift will pour onto a new type of investment exchange - and he's showing investors how to position themselves starting with just $100.

Click here to see how Jeff Brown says to claim your stakeThe takeaway is that organizations and enterprises that need to secure identities and access, including agentic AI, can do so with Okta regardless of which vendor provides the technology being secured.

Regarding agentic AI, it drives an exponential increase in access requests, which in turn drives demand for Okta’s services.

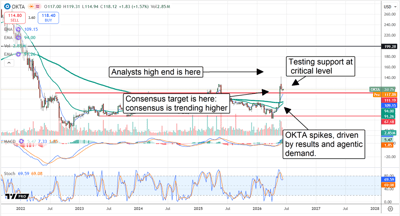

Okta’s AI-Driven Price Spike Supported by Analysts

Okta’s price spike itself is telling. The market surged by more than 30% in the week of the release, indicating robust support at a cluster of moving averages. That cluster is significant, suggesting a market with aligned forces and a firm floor in price action.

OKTA’s price has broken to a 12-month high and is now at a four-year high, indicating shifting market dynamics and a high probability of a continued move higher. As of mid-June, profit-taking has capped gains, but support remains at the high end of the previous range, setting the stage for another rally this summer.

Analyst trends are also central to the stock’s outlook and strengthened following the Q1 release. MarketBeat tracked 25 revisions in the first week, and all but four were price target increases. Three of the four outliers were reaffirmed targets, aligning with a forecast for consensus-or-better pricing, while the single downgrade was offset by a price target increase to an above-consensus level.

The critical takeaway from the analyst data is that the consensus of fresh targets is just over $118, an 18% increase from the pre-release level, including the new high target of $150. The $118 consensus implies modest upside relative to the critical support target, while the $150 high suggests that another multiyear high could be set. In this scenario, the consensus trend provides support for price action, while the high end leads the market. Assuming upcoming releases extend the trends revealed in Q1, analysts’ price target forecasts will continue strengthening and leading this market higher.

Institutional data suggest downside risk is limited this summer. Institutions own more than 85% of the stock, providing a solid support base, and they shifted from distribution in Q1 to accumulation in Q2. That shift aligns with the April stock price bottom, strengthening it as a support target and helping explain the May/June advance. The likely outcome is that this group retains its bullish posture in 2026, potentially accelerating accumulation as subsequent reports are released.

Okta Builds Momentum in Q1: Raises Guidance, Though Outlook Remains Cautious

Okta had a solid quarter in Q1, with revenue of $765 million, up 11.2% year-over-year and slightly ahead of MarketBeat’s reported consensus. Strength was driven by agentic demand and reinforced by forward-looking metrics that suggest acceleration in upcoming quarters. Remaining performance obligation, a measure of contracted business, grew 16%, suggesting the Q2 and full-year guidance updates were cautious. Management expects growth to continue and exceed consensus, but only 9% in the current quarter and 9.5% for the year.

Margins and earnings were also strong. The company managed costs and spending well, resulting in adjusted earnings growth that exceeded forecasts by more than 600 basis points. More importantly, strong earnings and cash flow bolster the capital return outlook through aggressive share buybacks. Q1 activity reduced the share count by more than 2.2% on average, giving investors significant leverage; the Q1 results and cash flow suggest that pace will continue in upcoming quarters and may even accelerate.

Okta’s balance sheet shows no red flags in 2026. The company carries no debt, has ample cash, and offers value for investors. Q1 highlights include increased cash and equivalents, reduced liabilities, and steady equity despite reinvestment and buybacks. Looking ahead, the likely outcome is that cash flow and free cash flow will continue to support growth and capital returns while maintaining fortress-like balance sheet metrics.

This email is a paid sponsorship sent on behalf of Chaikin Analytics, a third-party advertiser of MarketBeat. Why did I get this email?.

This ad is sent on behalf of Chaikin Analytics, 201 King Of Prussia Rd., Suite 650, Radnor, PA 19087. If you would like to optout from receiving offers from Chaikin Analytics please click here.

If you have questions or concerns about your newsletter, please contact MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Pl. #620, Sioux Falls, SD 57103. USA..

Post a Comment

0Comments