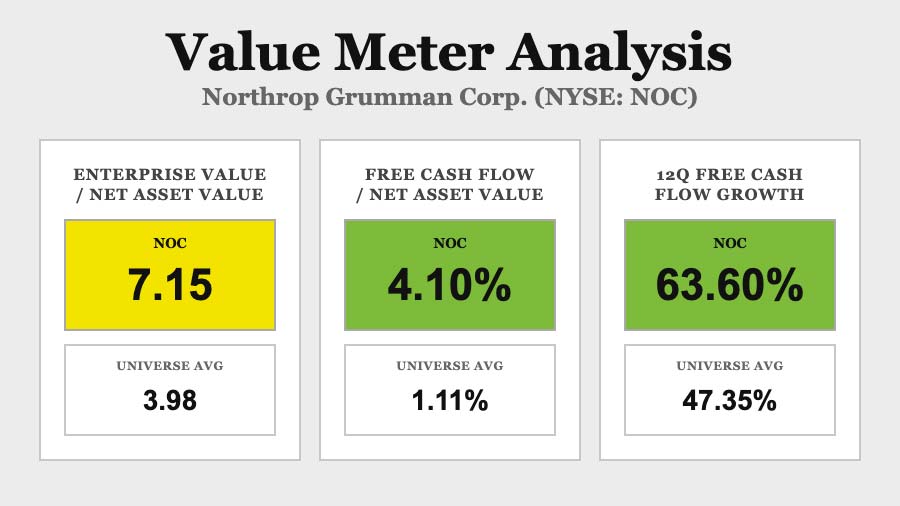

| Defense stocks rarely lack attention, but the latest surge in global tensions has pushed the sector back into the spotlight. Due to the ongoing war in Iran, investors are once again confronting the reality that modern conflicts can rapidly drain missile inventories, satellites, and advanced weapons systems. When that happens, governments don't wait long to replenish them. That renewed urgency has directed fresh investor attention toward the companies that build those systems - and few defense contractors sit closer to the center of that demand than Northrop Grumman (NYSE: NOC). Northrop Grumman is one of the United States' largest defense contractors, specializing in advanced aerospace platforms, missile defense systems, radar technology, and space capabilities. Its portfolio includes the B-21 Raider stealth bomber, missile defense networks, autonomous aircraft, and a growing array of space-based defense assets. With deep ties to the U.S. Department of Defense and allied militaries, the company occupies a strategic position in the global defense supply chain. Its most recent results reflect that high-demand environment. In the fourth quarter of 2025, Northrop Grumman generated $11.7 billion in sales, up 10% year over year. For the full year, revenue reached $42 billion, while free cash flow climbed to $3.3 billion - a 26% increase from 2024. The company also finished the year with a record backlog of $95.7 billion, giving it substantial visibility into future revenue. With those strong fundamentals in place, the key question becomes whether investors are paying too much for that strength. Northrop Grumman currently trades at an enterprise value-to-net asset value (EV/NAV) ratio of 7.15. That's significantly higher than the universe average of 3.98. The company's cash-efficiency helps explain why. Northrop Grumman generates quarterly free cash flow equal to 4.10% of its net assets, compared with just 1.11% for the broader universe. Simply put, the company is converting its assets into cash far more efficiently than most of its peers. Growth adds another layer to the story. Over the past 12 quarters, Northrop Grumman has grown its free cash flow quarter over quarter 63.6% of the time, compared with 47.35% across the broader market. That faster growth reinforces the narrative of a defense contractor benefiting from long-cycle programs and expanding global demand. At first glance, the valuation premium might appear steep. Paying nearly twice the average EV/NAV - and buying after a nearly 70% rise in just over a year - would normally raise concerns for value-focused investors. However, this may be a rare case where the company's impressive performance and the broader sentiment toward the defense sector justify the price. Let's find out The Value Meter's final verdict... |

Post a Comment

0Comments