Below is an important message from one of our highly valued sponsors. Please read it carefully as they have some special information to share with you.

Dear Reader, In this short 3-min. video, legendary investor James Altucher reveals the name and ticker symbol of a company he believes will skyrocket as soon as March 26th… 100% FREE of charge. No tricks. No gimmicks. Free. The company he reveals here is directly tied to the hotly anticipated IPO of Elon Musk's Starlink… Which is estimated to be worth $100 BILLION when it finally goes public. That would make it the biggest IPO in history! And right now – today… You can get a "pre-IPO" recommendation on Starlink before it goes public… From one of the most successful investors in the world – completely FREE of charge. Click here to watch the video now. It's only 3 minutes long… And it could give you an early stake in one of the biggest profit opportunities of all time. Click here to check it out before it's too late. Best, Matt Insley Publisher, Paradigm Press P.S. Starlink could go public as soon as March 26th. So for your chance at the biggest possible gains… Make sure you act on this ASAP. Click here to watch James' urgent 3 min. video now.

Today's editorial pick for you

Domino’s Pizza Stock: A Clear Winner in QSR

Posted On Feb 24, 2026 by Chris Markoch

The quick-service restaurant (QSR) sector is separating into clear winners and losers. You can put Domino’s Pizza (Nasdaq: DPZ) firmly in the winner’s column. The company’s Q4 2025 earnings report, released on Feb. 23, reinforces a compelling investment thesis: Domino’s is not simply a pizza company. It is a technology-driven, franchise-powered growth machine that has carved out a dominant position at the intersection of value, convenience, and scale.

Table of Contents

For the full fiscal year, Domino’s delivered global retail sales of over $20.1 billion, a 5.4% increase excluding foreign currency impacts. U.S. same-store sales grew 3%, while the company added 776 net new stores globally. That brings its total footprint to 22,142 locations across more than 90 markets. Income from operations rose 8.5% to $954 million, and free cash flow surged 31.2% to $671.5 million.

These numbers tell a story of a brand executing with discipline. While inflation, shifting consumer spending habits, and rising labor costs have pressured much of the restaurant industry, Domino’s is gaining ground. For investors weighing whether to initiate or add to a DPZ position, the earnings report provides a strong foundation for the bull case. However, that bullish view comes with caveats worth considering carefully.

Market Share Growth Is the Headline Story

“In our U.S. business, we gained another point of market share, pacing well ahead of the QSR Pizza category.” — Russell Weiner, CEO

In a competitive landscape where restaurant traffic has been volatile and consumer price sensitivity is elevated, gaining market share is the clearest signal of brand health. Domino’s reported U.S. same-store sales growth of 3.7% for the fourth quarter and 3.0% for the full year. Perhaps more meaningfully, CEO Russell Weiner confirmed the company captured another full percentage point of U.S. QSR pizza market share in 2025. That was a category that itself continued to grow.

Store count growth tells a similar story. Domino’s added 1,132 gross new locations globally in fiscal 2025, resulting in net growth of 776 stores after closures. Q4 alone saw 392 net new stores open.

These are not vanity metrics. Each new franchised location represents an asset-light royalty stream that flows directly to Domino’s top line with minimal incremental capital required from the parent company. Franchise stores represent 99% of the total store count, making this one of the most capital-efficient expansion models in the restaurant business. The company’s Hungry for MORE strategy, anchored in value and operational excellence, is clearly resonating with both consumers and the franchisees who bet their capital on the brand.

Institutional Confidence and a Premium Valuation

DPZ stock trades at approximately 23x forward earnings — a slight premium to the broader S&P 500 but well within the range that Domino’s has historically commanded. Investors who view this as expensive in isolation may be missing context. Domino’s generates highly predictable, recurring royalty revenue, operates with significant pricing power, and has a proven ability to grow even during periods of macroeconomic stress.

Institutional ownership of DPZ has remained steady and constructive, reflecting confidence in the company’s long-term earnings trajectory. With diluted EPS of $17.57 for fiscal 2025 — a 5.3% increase year over year — and a lower share count due to ongoing buybacks ($354.7 million in repurchases during 2025), the per-share earnings story is improving even when aggregate net income growth is moderate. The leverage ratio improved meaningfully from 4.9x to 4.4x, signaling that management is bringing the balance sheet into a more conservative position despite running a negative stockholders’ equity model common to asset-light, high-return franchisors.

A 15% Dividend Hike Signals Management Confidence

On Feb. 18, 2026, Domino’s Board of Directors approved a 15% increase to its quarterly dividend, raising it to $1.99 per share. The dividend will be payable March 30. While the absolute yield remains modest given DPZ’s share price, the rate of dividend growth is a powerful signal.

A 15% increase is not the act of a management team hedging its bets; it reflects genuine confidence in the durability of free cash flow (FCF). For income-oriented investors who may be deterred by the stock’s approximately $400 price tag, the growing dividend, combined with a robust $671.50 million in FCF in 2025, makes DPZ stock increasingly compelling as a total return holding rather than a purely growth-oriented position.

Challenges to the Bull Case

No thesis is complete without an honest look at risks. The most visible pressure point in the Q4 report is U.S. Company-owned store gross margin, which compressed 5.4 percentage points year over year, driven by higher insurance costs, rising labor rates, and food basket price inflation of 1.7%.

While franchised stores bear the brunt of these cost increases at the unit level, sustained margin pressure could dampen franchisee enthusiasm and slow new store development. International same-store sales growth, at just 0.7% for Q4, also trails the U.S. business. Currency headwinds remain a structural wildcard for a company deriving roughly half its retail sales from international markets. Investors should monitor franchisee profitability metrics closely in coming quarters.

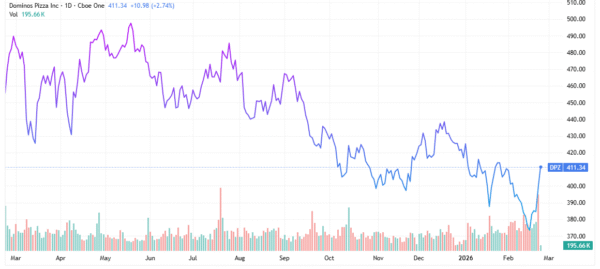

Technical Picture: Support Holds, Momentum Builds

From a technical standpoint, DPZ has traded in a constructive range in the months leading up to this earnings release. Shares have held above their 200-day moving average, a key indicator that long-term trend participants remain committed. The dividend increase and strong free cash flow number provide a fundamental backstop against significant downside.

Investors comfortable with the valuation should watch for a clean breakout above recent resistance on volume. This would be a signal that the market is re-rating the stock toward the higher end of its historical multiple range. Conversely, any macro-driven selloff toward the $360–$370 range would represent a high-quality entry point for long-term holders, given the underlying earnings and cash flow trajectory. The combination of buybacks, a rising dividend, and expanding store count creates a durable compounding mechanism for patient investors.

Bottom Line: Own the Winner

Domino’s fiscal 2025 earnings report is a reminder that in a sector defined by disruption and margin pressure, execution still wins. The company is growing stores, gaining market share, generating record free cash flow, and returning capital to shareholders at an accelerating rate.

At 23x earnings, DPZ is not cheap — but it is priced appropriately for a business with this level of consistency and competitive moat. For investors seeking a quality compounder in the consumer sector, Domino’s Pizza deserves a place on the buy list. The $400 price point is not a barrier; it is a feature that has historically rewarded those willing to pay for quality.

This is a PAID ADVERTISEMENT provided to the subscribers of Daily Options Signals Free Newsletter. Although we have sent you this email, Daily Options Signals and StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us. If you no longer wish to receive email from DailyOptionsSignals.com, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

Post a Comment

0Comments