NVIDIA: The Good, the Bad, and the Truth About the Company's Earnings

Posted On Feb 26, 2026 by Chris Markoch

NVIDIA Corp. (NASDAQ: NVDA) reported earnings after the market closed on Feb. 25, and the results were better than expected. Or were they? Despite what many investors would view as a strong report, NVDA stock was down nearly 4% in midday trading the day after the report. That was up from session lows, but it still was an unexpected jolt to investors who hoped NVIDIA would be the tide that lifted many boats.

Table of Contents

This is a time when investors need to make their own assessment. To do that, it's important to decide if the immediate response to the report has changed the fundamental outlook for NVDA stock.

The Three Sides to Every Story

In the hyperbolic world we live in, I find that there are frequently three sides to every story. The extremely positive, "everything is awesome" view. The extremely negative "software will take all our jobs" kind of view. And then there's that funny little thing called the truth. It's usually not the hot take that lives on the extremes, but if you're an investor, it should be your north star.

That's a little of what I see happening with NVIDIA stock after its report, which wasn't just good, it was very good. But when you're Josh Allen, just being as good as you were last year isn't good enough to satisfy the haters.

With that said, let's take a look at the three sides of NVIDIA's report.

NVIDIA Blew the Doors Off

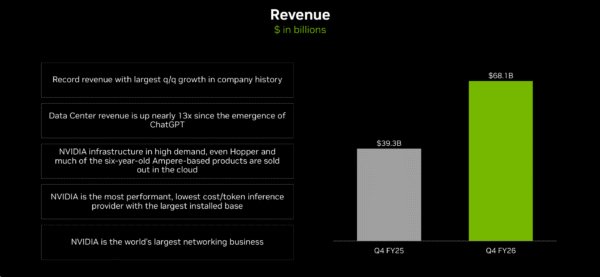

The numbers don’t lie. NVIDIA posted Q4 FY26 revenue of $68.1 billion, a staggering 73% jump year-over-year from $39.3 billion, and what the company called the largest quarter-over-quarter growth in its history. That alone should silence the skeptics, at least for now.

Data Center revenue — the engine driving this whole machine — surged to $62.3 billion combined across compute and networking. Compute alone hit $51.3 billion, up from $32.6 billion a year ago. Networking? Nearly quadrupled to $11 billion. These aren’t rounding errors. These are the kinds of numbers that rewrite expectations.

Earnings per share nearly doubled year-over-year on a GAAP basis, from $0.89 to $1.76. Gross margins expanded to 75%, and free cash flow exploded to $34.9 billion — more than double the prior year’s $15.5 billion. For context, that’s more free cash flow in a single quarter than most S&P 500 companies generate in a year.

Blackwell demand remains relentless. Even older Hopper and six-year-old Ampere-based products are sold out in the cloud. When your previous-generation hardware is still flying off the shelves, that’s not a bubble — that’s a backlog.

This was a strong report that should have removed concerns about an "AI bubble" in 2026 or 2027. But earnings reports are like progress reports that parents may receive about their students. Good or bad, they reveal what happened in the past. The future is still unknown. That takes us to the bearish case.

Oh Yeah, But What About 2028?

Let's be clear that a 4% pullback in NVDA stock is hardly a catastrophe. But it's a head scratcher, because the report was strong. And that was without NVIDIA reporting demand from China.

But the concern is about what's on the horizon. Much like Palantir (NASDAQ: PLTR), analysts are not concerned about current demand, but about NVIDIA's ability to keep that demand growing at these otherworldly levels once the AI cycle matures.

This argument isn't completely about the size of the pie. It's about how big NVIDIA's slice will be. Right now, it's still the leader by a significant margin. But as is the case with any market, competition brings down prices, and customers want to reduce what is seen as a single-supplier risk.

A third concern is about the company's capital expenditures, which many investors have heard talked about as the "circular trade." The concern is that this arrangement could create an AI spending loop. That benefits NVIDIA, until it doesn't. What would happen if partners back away from their commitments?

These arguments, plus the news that Michael Burry pointed out imperfections in NVIDIA's future numbers, landed with both retail and institutional investors.

But should it? Investor psychology is a funny thing.

The past performance doesn't guarantee future results caution applies for NVIDIA bulls. However, the caution for bears is to not let the perfect be the enemy of the good.

The Truth Coming Out of NVIDIA's Earnings

The response to NVIDIA's results isn't solely about NVIDIA. It's about the growth of AI, which is happening faster than many of us imagine, and yet it's still seen as being in its early stages. That means that enterprise customers are already using the top level of the AI stack, the application layer.

That demand is generating cash flow today, which will be reinvested in NVIDIA GPUs. It's the flywheel effect that Jensen Yuang has talked about for several quarters.

I'm old enough to remember when the internet was a "novel idea." At that time, it seemed technology was moving faster than our ability to keep up. Today, that seems more true than ever. Agentic AI is already here, but many analysts continue to look at hyperscaler investment as a quixotic bridge to nowhere.

But that bridge is getting built whether we're ready or not. And NVIDIA's products will be critical to that buildout. It's the signal, not the noise.

The size of the pie may reach a steadier state, but it's not likely to shrink. And much like many major cities have several bridges that act as thoroughfares, there will be room for other competitors to get their share of the pie. But that doesn't mean NVIDIA will get less.

This Looks Like a Solid Entry Point for NVDA Stock

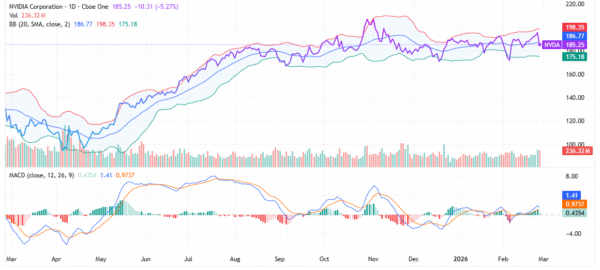

One tell I have for many earnings reports is what analysts have to say immediately after the report. In the case of NVIDIA, several analysts raised their price targets on the stock the day after the report. And many of the new targets are well above the consensus stock price of $264.53. That's already more than 40% above the NVDA stock price as of this writing.

That means, if you're looking at NVIDIA as a long-term hold, there's no reason why this wouldn't be a bullish entry point. Buyers and sellers have been bouncing the stock in a narrow range for some time without much conviction either way. But if you believe in the long-term story, NVDA stock has plenty of upside.

If you're a trade, things may be trickier. The Mar. 27 options chain shows that there's significant interest in call options at the $200 and $210 strike prices.

Headlines lift stocks in the short term. Results will eventually cause analysts to bid up a stock in spite of themselves.

This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

Post a Comment

0Comments