While I can't promise future performance, previous picks from this new Monday Algo have racked up gains of +149%, +190%, and +536%... in as little as one day.

1. Results are not typical. I teach methods that have made other traders money, but that does not guarantee you will make any money. Success in trading requires hard work and dedication. Past performance does not indicate future results. All trading carries risks.

Today's editorial pick for you

AutoNation (AN) Stock Faces a Critical Technical Test Ahead of Earnings

Posted On Feb 05, 2026 by Joshua Enomoto

AutoNation(NYSE: AN) could either be a catalyst or the canary in the coalmine. As an automotive retailer — one that sells both new and pre-owned vehicles — its upcoming fourth-quarter earnings results will be heavily dissected by Wall Street. For all the talk about making America great again, it has to show in the results. Therefore, AN stock stands on anxious ground.

Table of Contents

When results are released on Friday before the market opens, analysts will be looking for earnings per share of $4.89 on revenue of $7.18 billion. In the year-ago quarter, AutoNation posted EPS of $4.97 on revenue of $7.21 billion, beating the consensus target of $4.26 and $6.81 billion, respectively.

Overall, the financial performance has been mixed. As things stand, AutoNation is riding four consecutive quarters of top-and-bottom-line beats. However, in the three quarters prior to this streak, it missed on sales while only managing to beat on earnings once.

Obviously, with geopolitical tensions rising, along with artificial intelligence disrupting the labor market, a strong result is more critical than ever for the automotive retailer. Interestingly, there are several clues to suggest that the bulls may have the wind at their back.

First, what helps make AN stock intriguing at this hour is a possible bullish pennant formation that may have been forming since early April last year. If this technical thesis turns out to be accurate, AN may be in the tail end of the consolidation phase of the pattern (which may have started in August). Taken to its logical extreme, the upcoming earnings report could light the catalyst's match.

Farfetched? While technical analysis may not be the most scientific methodology, there's another piece of evidence that warrants much closer investigation.

Volatility Skew Reveals Sentiment Structure for AN Stock

When trading stocks and especially options, you're constantly in a war with uncertainty. The name of the game isn't to eliminate uncertainty altogether, as that would simply be impossible. Instead, we want to narrow the probability space as much as possible to better inform our decision-making processes.

One of the most significant tools that retail traders have ready access to is volatility skew, a screener that identifies implied volatility (IV) or a stock's potential kinetic output across the strike price spectrum of a given options chain. For the Feb. 20 expiration date — which is the next closest options chain — the underlying skew shows a prioritization of upside convexity.

For strike prices above the current spot price, call IV pricing steadily rises, which indicates that traders anticipate the possibility of a sizable move northward. True, put IV also marches steadily higher for strike prices above spot, which may indicate hedging behavior to protect long-side exposure. However, the IV for the puts is priced lower than that of calls, indicating that upside convexity is the dominant theme.

On the other end of the scale, put IV stands above calls at the lower strike price boundaries. While the magnitude of curvature is less pronounced than the call skew seen in the upper strikes, the surface-level distortion suggests that the smart money believes downside movements represent a non-trivial risk factor. Given that the market has been shaky recently, it's completely understandable that sophisticated players are hedged.

Still, the most significant takeaway here may be that investors aren't necessarily running away from AN stock. Although there's a critical earnings test coming up, AutoNation is treading water. Since the start of the year, the security is up a little over 1%. Even better, the quantitative picture could be pointing to a pleasant surprise.

Translating Sentiment to Output

Although we now have a solid idea of the sentiment bias of smart money traders, we're at a loss as to how this translates into the potential output of AutoNation stock. For that, we can turn to the Black-Scholes-derived expected move calculator. According to the financial model, AN would likely land between $199.13 and $223.08 for the Feb. 20 options chain. This calculation represents a 5.67% high-low spread relative to the current spot price.

Where did this dispersion come from? Black-Scholes assumes a world where stock market returns are lognormally distributed. Under this framework, the above range represents the perfectly symmetrical area where AN stock would fall one standard deviation away from spot (while accounting for volatility and days to expiration).

If you look at the math, the model basically asserts that in 68% of cases, AN should land between roughly $199 and $223 when Feb. 20 rolls around. While this calculation lays out the parameters of the battlefield, it's not the most instructive insight for debit-side options traders.

Let's imagine that you're a member of a search-and-rescue team and you need to look for shipwrecked survivors. Black-Scholes is important in a sense because it's like declaring a specific search area: for example, that the stricken ship went down somewhere in the Pacific Ocean (as opposed to the Atlantic or any other body of water).

However, the Black-Scholes model makes its calculations independent of market structure. In other words, it's probably accurate in setting the search parameters, but it doesn't offer a probabilistic view because it doesn't incorporate contextual factors that could influence forward probabilities.

That's a major problem. It's similar to assuming that the Pacific has no current and that environmental factors are negligible. The model is also assuming that the survivors are simply floating and not swimming or behaving in ways that could compound the distance from where they made their distress call.

As an officer charged with leading search efforts, you have difficult choices to make. Bluntly speaking, not every incident merits a full-scale search. You can't just buy a long iron condor and play both the bullish and bearish side, much like you can't send all the cutters, helicopters and drones to find one missing person. There's only so much money in the budget and there's only so much daylight available.

At some point, you have to use probabilistic math to improve the odds of finding the survivors — and that's where the Markov property comes into view.

Markov Provides a Guiding Light

Under Markov, the future state of a system depends solely on the current state. That's a fancy way of saying that forward probabilities should not be independently calculated but rather assessed under an ecosystem context. To use a simple football analogy, a 20-yard field goal is an easy chip shot. Add snow, wind and playoff pressure, and these odds may change dramatically.

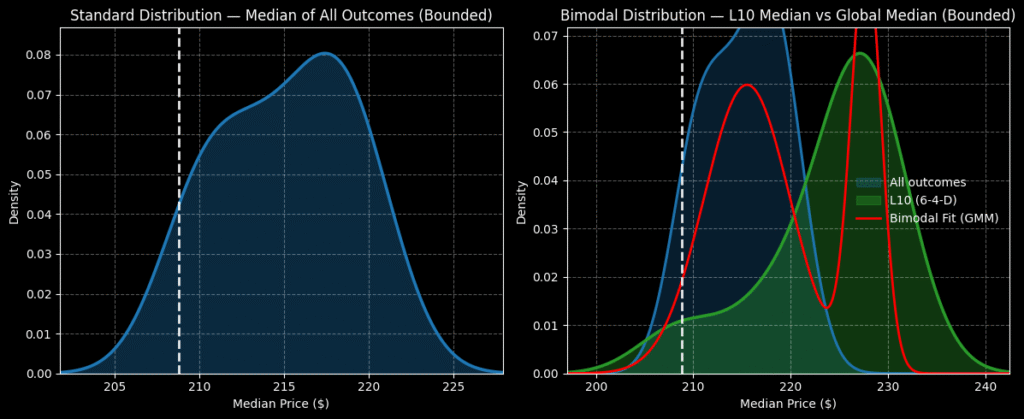

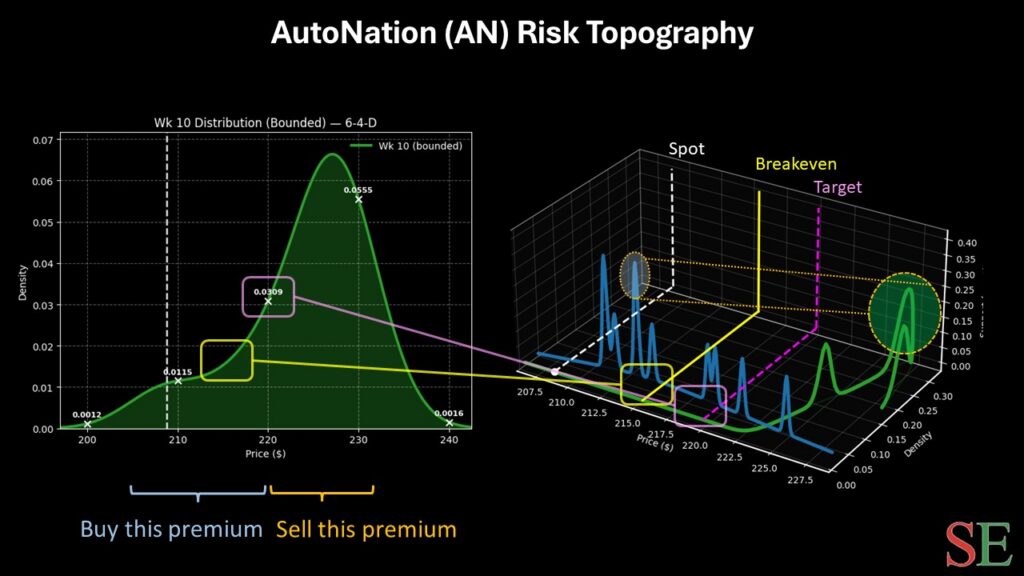

When it comes to our search-and-rescue analogy, Markov isn't just useful — it's necessary. Let's consider the current context of AN stock. In the last 10 weeks, it printed six up weeks, but with an overall downward slope. This contrarian 6-4-D sequence represents a specific type of ocean current. Put another way, survivors caught in these waters will likely drift in a certain way compared to if a different type of current were involved.

Subsequently, we can use enumerative induction to see how the market typically responds under 6-4-D conditions, as well as incorporate a Bayesian-lite inference to calculate an estimated range. Over the next 10 weeks, we would expect AN stock to land between $195 and $243, with probability density peaking near $227.

To be clear, there's no guarantee that AN stock will coalesce at or near this level. Just like the Pacific Ocean, the market is a cruel place, ready to pounce on unsuspecting visitors. Given the uncertainties, we can use math to reduce as many variables as possible. But even the greatest rescue campaign can't overcome an unforeseen shark attack.

Still, the theory is that over time, market behaviors statistically conditioned on specific quantitative structures should yield similar results. That's where inductive Bayesian inference comes into the frame. In a highly variable ecosystem, this is probably the best approach available to retail traders.

Right now, the options market is thin, with only three bull call spreads available to choose from (though more could be unlocked as price dynamics shift). Right now, the most aggressive trade is the 210/220 bull call spread expiring Feb. 20, which features a max payout of over 80% and a breakeven price of $215.55.

However, if a bull spread with a second-leg strike of $230 becomes available, that may be the trade to consider. A positive Q4 earnings print could help provide the fuel to reach this lofty but quantitatively rational target.

This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

Post a Comment

0Comments